Credit Agricole with the note.

Thanks to an impressive resurgence this month, the USD is set to come in on top of all its G10 FX peers in Q323. The USD has been unfazed by the lingering threats of a US government shutdown that historically tends to act as a drag, and instead focus on the widening chasm between a resilient US economy and a stagnant Europe, as evidenced by the most acute relative appeal in long rates in years.

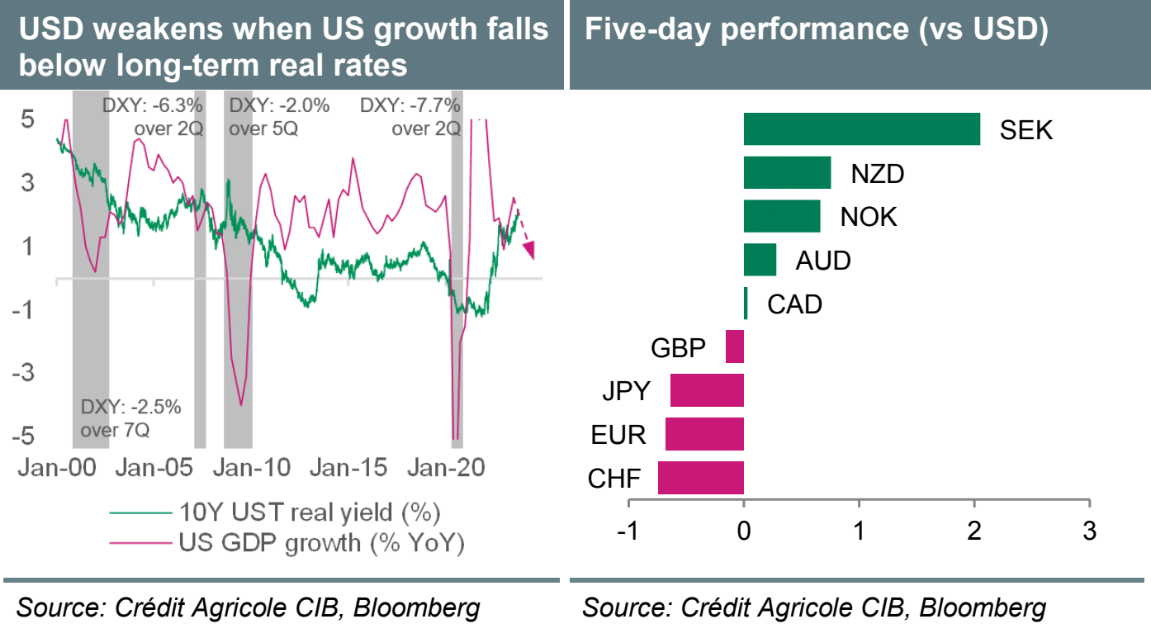

With the price of oil having just extended its rally to fresh YTD highs just shy of the USD100/bl threshold, one may think that inflation expectations have been the main driver in the latest leap higher in interest rates. And yet, it is the real rate component that has experienced the steepest rise, as of special note the real 10Y UST yield has just risen to its highest level since 2008 above 2.25%.

This measure arguably corresponds to the market pricing of long-term US growth prospects, and a direct comparison to actual US growth rates could prove interesting. For most of the past 23 years, the latter tends to exceed the former, as an outperformance of the US economy vs its longterm potential possibly brings stability. Nevertheless, over that period, there have been four episodes when this relationship inverts for a long enough time, which in every case translated into USD losses vs other FX majors.

The latest leading surveys such as next week’s ISMs suggest that US GDP could beat this mark again in Q323, though the tide may turn around the turn of the year. While not necessarily bringing a steep recession, our US economist still expects the US annual growth rate to cool to 1.5% and 0.7% YoY in the next couple of quarters. It would most likely imply either a drop below the long-term US real rate mark, or a reduced appeal from long nominal rates, as both tend to spur some USD weakening.

Elsewhere next week, the final Eurozone PMIs for September could confirm a tentative turnaround in activity momentum, as most bad news already seems to be in the price. The RBA and RBNZ look set to leave their policy rates unchanged as they continue to observe the impact of existing rate hikes, while risks of FX interventions loom high in Japan as USD/JPY threatens a break of 150.

We could get his correction courtesy of a US shutdown that eases yields.