Since June, the Reserve Bank of Australia (RBA) has kept the official cash rate (OCR) at 4.10%. Official interest rates have hopefully also peaked; although that will depend on whether there is a major upside surprise in the economic data.

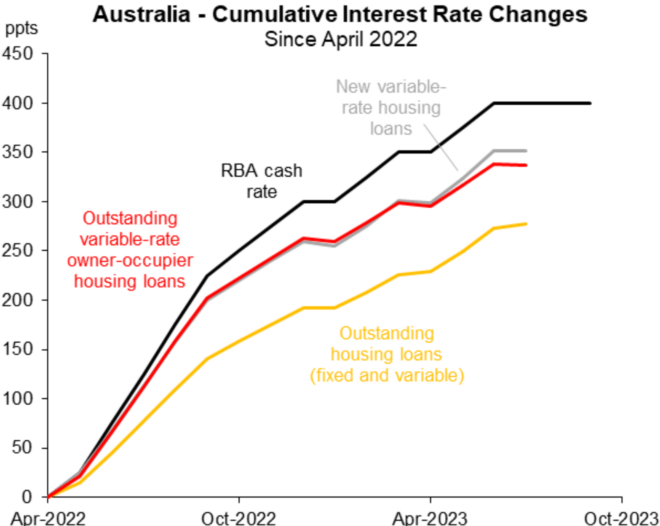

However, given there is still a large number of cheap pandemic fixed-rate mortgages that have yet to convert to variable rates, the RBA can rest assured that average mortgage rates will continue to rise, meaning there is still a significant amount of monetary tightening ‘baked in’ to the system:

Source: Justin Fabo (Macquarie Group)

According to CBA, by mid-2024, when almost all of the current fixed-rate mortgages have expired, Australian consumers will spend about 10% of their disposable income on debt maintenance costs, easily the largest share on record.

Accordingly, as these fixed-rate mortgages mature, the average interest rate paid by Australian mortgage holders will rise.

This reduces the RBA’s need to boost interest rates even further in order to slow the economy.

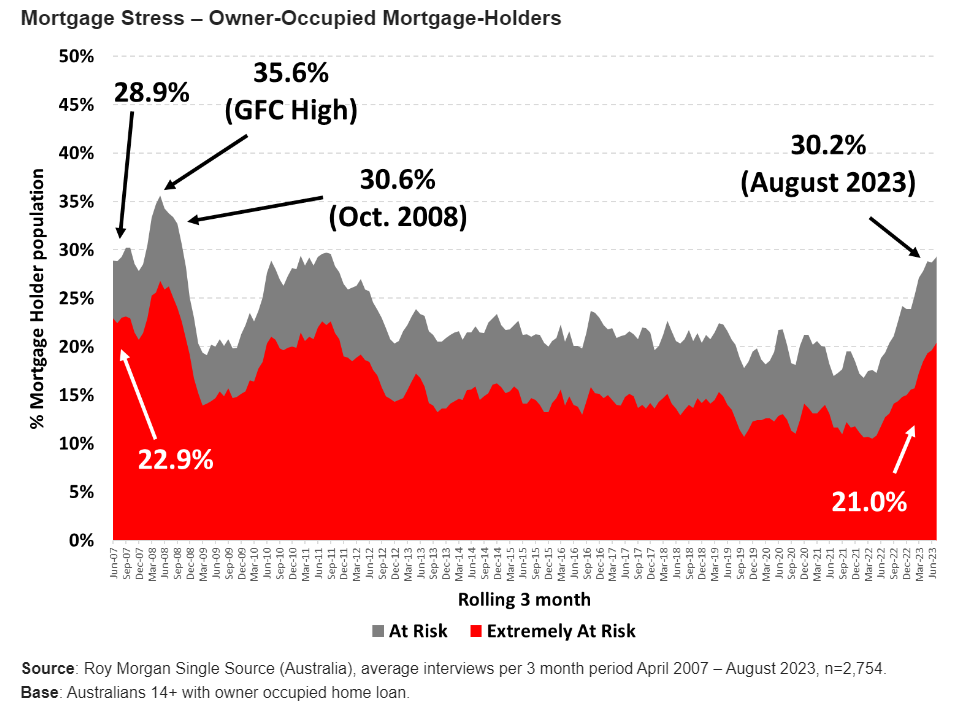

Mortgage stress continues to rise:

Roy Morgan has released its mortgage stress survey for August, which shows that 30.2% of owner-occupied households with mortgages are “stressed”, the highest share since October 2008 when the OCR was 7.25%:

The number of Australians ‘At Risk’ of mortgage stress (1,566,000) is at a record high.

The number of mortgage holders considered ‘Extremely At Risk’, has now increased to 1,066,000 (21.0%) which is now significantly above the long-term average over the last 15 years of 15.3%.

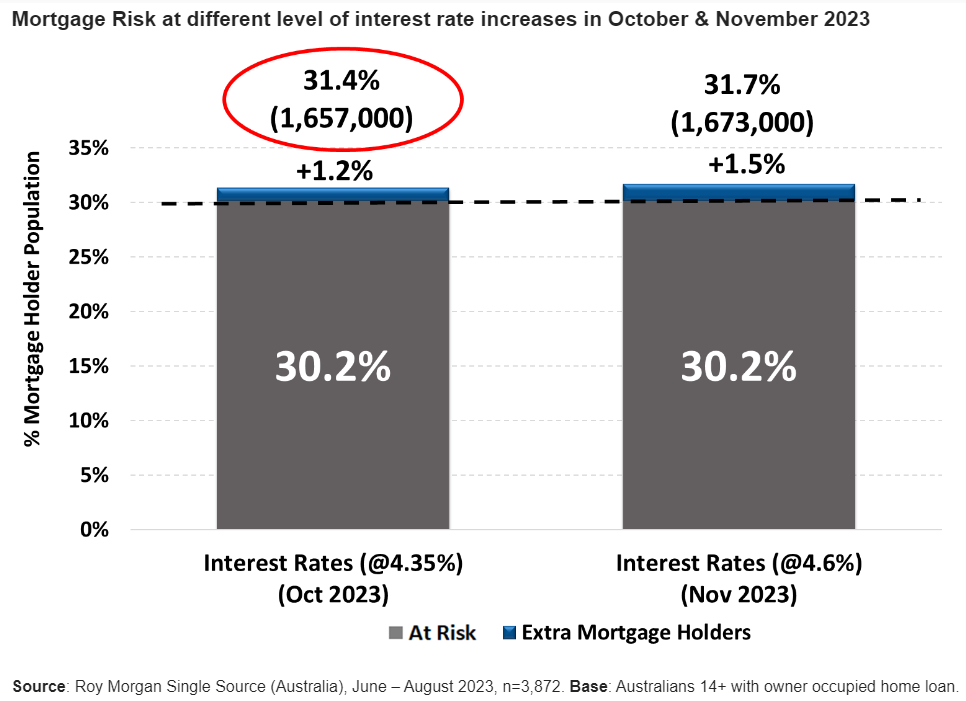

The impact of two unlikely RBA interest rate increases of +0.25% in October (+0.25% to 4.35%) and November (+0.25% to 4.6%) has been modelled by Roy Morgan.

If the RBA hikes interest rates by +0.25% in October to 4.35%, 31.4% (up 1.2% points) of mortgage holders, or 1,657,000, will be labelled ‘At Risk’ in October 2023, a 91,000 rise.

If the RBA hikes interest rates by another +0.25% in November to 4.6%, 31.7% of mortgage holders, or 1,673,000, will be labelled ‘At Risk’ in November 2023, an increase of 107,000.

Roy Morgan employs “a conservative model, essentially assuming that all other factors remain constant”.

Therefore, as more borrowers switch from fixed to variable rates, mortgage stress will rise.

Moreover, if Australia’s unemployment rate rises in line with the RBA’s projection, from 3.7% to about 4.5% late next year, mortgage stress will worsen.