By Stephen Halmarick, Chief Economist at CBA:

Key Points:

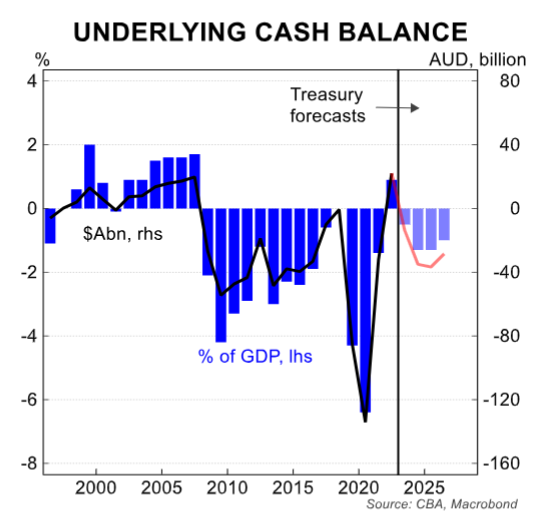

- The 2022/23 budget position has come in much stronger than previously estimated, as widely expected. For 2022/23 the budget was in surplus by $A22.1bn (+0.9% of GDP), a substantial improvement on the October 2022 estimate of a deficit of $A36.9bn (-1.5% of GDP) and the more recent May 2023 estimate of a $A4.2bn (+0.2% of GDP) surplus.

- The improvement in 2022/23 came mostly from the revenue side. Total revenue is up $A13.9bn relative to the May 2023 estimate, jumping to 25.7% of GDP from an previous estimate of 25.0% -thanks largely to higher company tax receipts. In contrast, spending for the 2022/23 year was $A4bn lower than the May estimate.

- While the benefits to the budget from the stronger-than-expected economy are likely to fade as we progress through 2023/24, the chances are high that the budget will remain in surplus this year and outperform the most recent estimate of a $A13.9bn (-0.5% of GDP) deficit.

- The stronger budget position has lowered Australia’s net debt position and has positive implications for the AOFM’s borrowing task.At 19.4% of GDP as at June 2023, Australia’s net debt is at its lowest level since 2018/19.

- Thetightening of fiscal policy that has been occurring through 2022/23 and pushing into 2023/24 will assist the RBA in getting inflation back into the 2%-3% target range,which we expect to see in H2 2024.

Bigger surplus in 2022/23

As widely expected, the final outcome for the 2022/23 Budget position showed a significant improvement on the estimates contained in the May 2023 Budget as well as the government’s October 2022 re-do on the budget for the last year.

Advertisement