Westpac with the note.

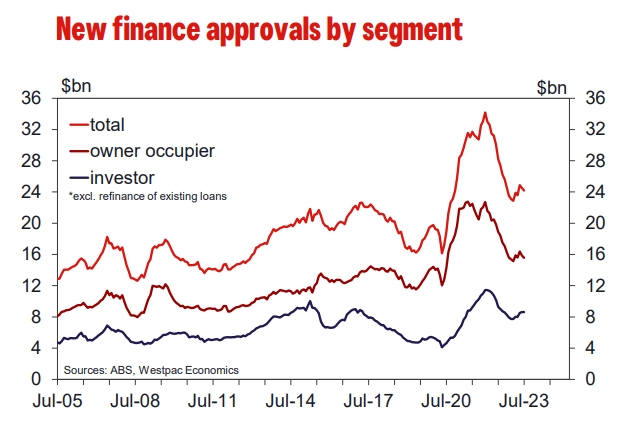

The total value of new housing finance approvals declined 1.2% in July following a 1.6% decline in June.

The result was a touch below the consensus forecast of a 0.5% decline, but within the margin of error for what can be a choppy series month to month.

The detail showed weakness centred on construction-related owner-occupier lending, with much milder declines for other segments.

As such the picture is still consistent with the wider narrative of a gradual, price-led recovery in established markets but suggests there may be more weakness coming through around new building.

The total value of loans to owner occupiers excl. refi declined 1.9%mth, the number of loans down 2.3%mth. That followed a slightly larger decline in June (–3.1%mth in value terms, –3.8%mth in numbers).

Despite the back to back declines, loans are still showing a steady rise on a 3mth avg basis, up 2.5%qtr in value terms and 4.3%qtr in number terms.

The detail shows a particularly big 6.2% drop in owner-occupier construction loans (–12.4% in number terms) which had posted a robust gain in June (+6.7% in number terms).

The state breakdown shows large falls in all major states with particularly big month to month swings in Vic, SA, WA and Tas.

While the July fall may prove to be ‘noise’ it could be a sign that new dwelling construction is moving into another leg lower.

This is not the signal coming from other indicators such as HIA new home sales and dwelling approvals but the space is clearly worth watching given the range of headwinds impacting new building.

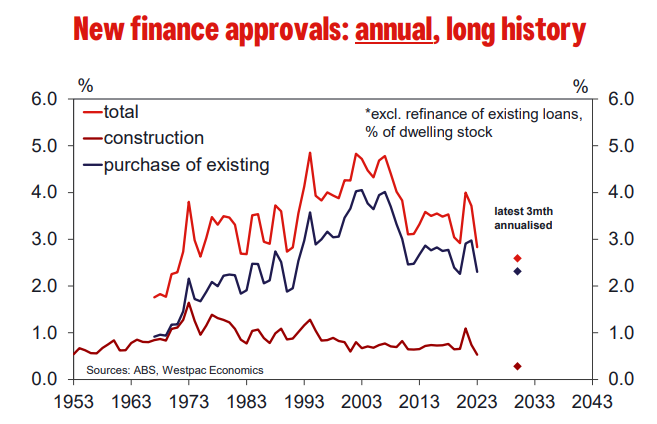

It should also be noted that current levels of new construction finance approvals are already extremely low – record 70yr lows when viewed as a proportion of the existing dwelling stock.

The July report had less detail than usual as estimates of first home buyer lending have been suspended due to data reporting issues that need to be resolved.

The state breakdown for the total value of loans showed, slightly bigger declines in SA (–4.3%mth) Vic (–3.3%mth) and WA (–3.2%mth), a milder 0.6%mth fall in NSW and Qld holding about steady.

The total value of investor loans was broadly unchanged, the state detail showing a strong 6.8%mth rise in Qld was offset by declines elsewhere including sizeable 2.6%mth dips in both Vic and SA.

Aside from the weakness around construction lending, the July report was broadly consistent with a continued gradual upturn in established markets, albeit hinting at some loss of momentum.