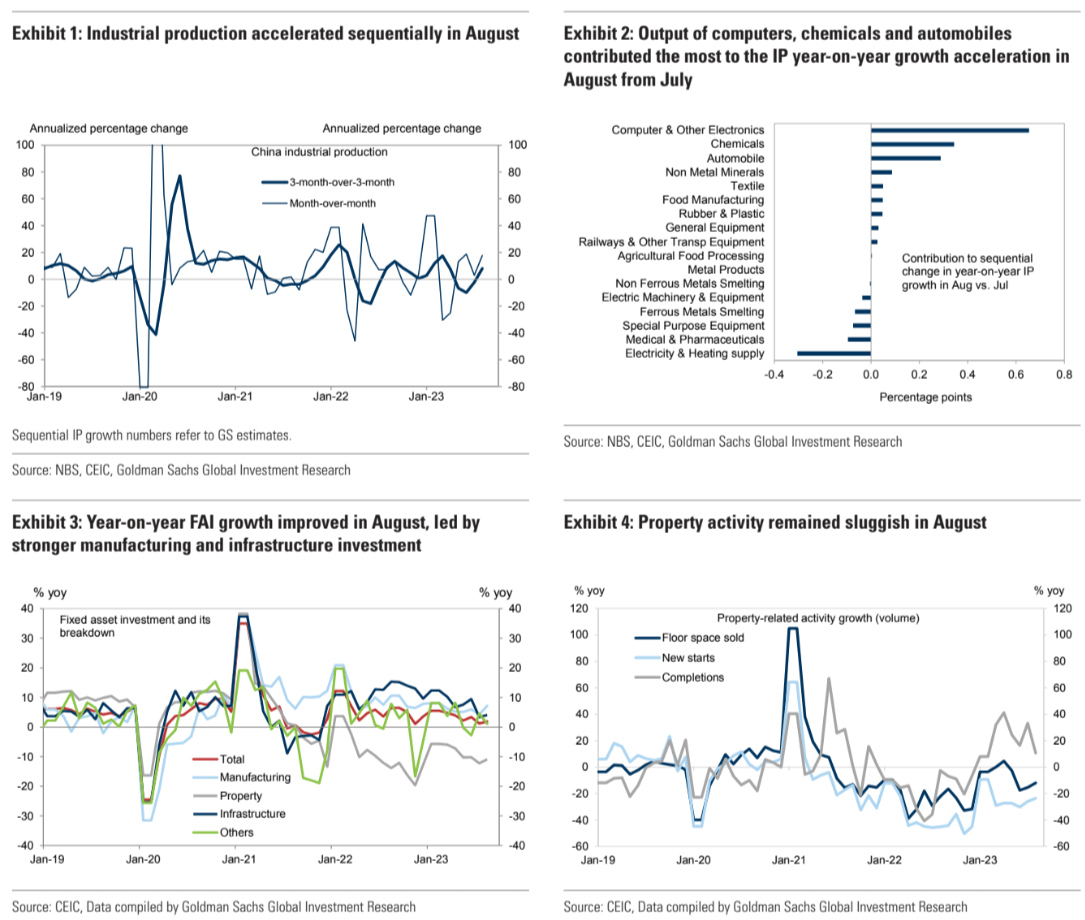

August activity data mostly improved from July and beat market expectations. Industrial production growth rose in August amid improved export growth, driven mainly by faster output growth in computers, chemicals and automobiles. Year-on-year growth in retail sales and the Services Industry Output Index both rose in August, thanks mainly to stronger auto and gasoline sales, although Covid-sensitive restaurant sales growth slowed. Fixed asset investment growth increased in August, led by manufacturing and infrastructure investment, but the magnitude of improvement was slightly smaller than expected, due partly to the prolonged drag from depressed property investment. Property-related activity remained sluggish in August despite the ongoing piecemeal housing easing. Taking into consideration the stronger-than-expected August activity data and our high-frequency trackers for the first half of September, we maintain our Q3 GDP growth forecast at 4.9% yoy, despite elevated uncertainties around the property sector.

The energy transition boom in EVs, PVs and renewables is where output growth is.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.