The Reserve Bank of New Zealand’s aggressive interest rate hikes, which have lifted the official cash rate by 5.25%, have crashed household consumption.

However, independent economist Tony Alexander believes the weaker-than-expected data could also prompt the Reserve Bank to begin its monetary easing cycle earlier than expected.

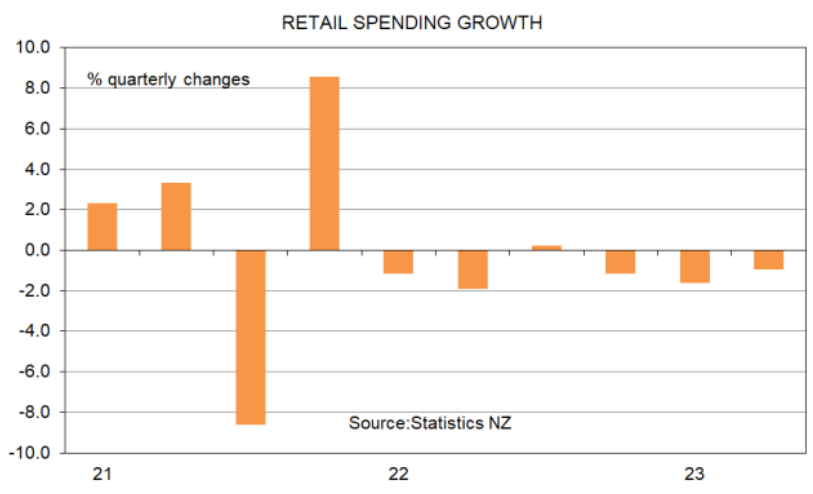

Last week Statistics New Zealand released data telling us what happened with retail spending during the June quarter. The main outcome of a 1% fall in sales after adjusting for inflation and seasonal effects was weaker than generally expected.

This suggests that the economy is performing less strongly than anticipated by the Reserve Bank and strengthens the case for the official cash rate coming down much sooner than the late-2024 timing which the Reserve Bank have pencilled in.

Spending has shrunk for five of the last six quarters.

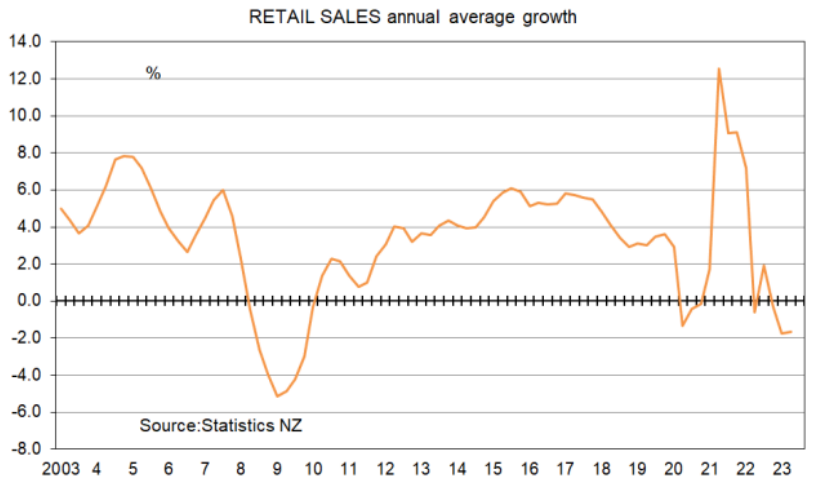

If we look at the year to June, we see spending on retail goods and services fell by 1.7% after inflation. This is the weakest growth (greatest shrinkage) since the Global Financial Crisis and there are many factors behind this situation.

Top of the list is tight monetary policy. The explicit intention of the Reserve Bank when it raises interest rates is that people with mortgages feel the pinch and cut back on their spending.

They also want to see weakness in the labour market and people made unemployed who will then also cut back on their spending.

They also want people to be fearful of losing their jobs and hope they also will cut back on their spending.

Then there is the exchange rate effect. The Reserve Bank hopes that higher interest rates will cause a higher NZ dollar which will cause weakness in incomes for exporters who will then cut their spending. Imported goods prices will also fall a bit.

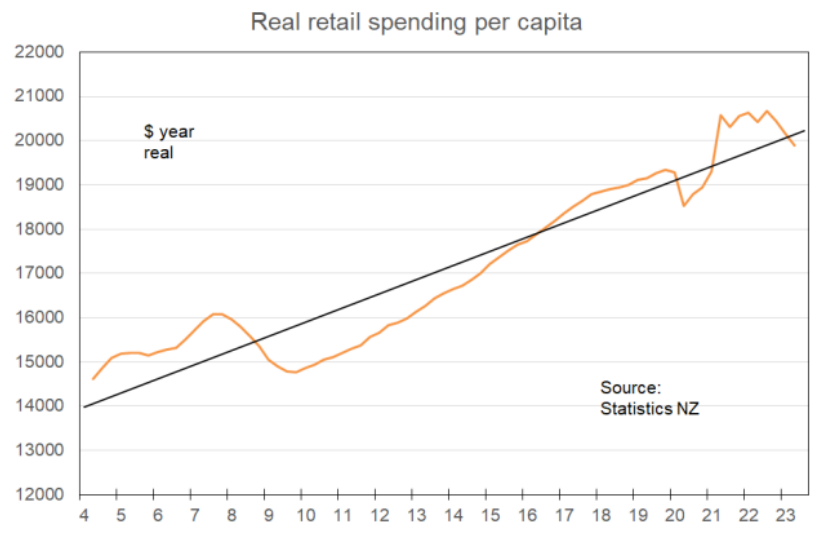

The exchange rate leg isn’t operating at all this time around, but clearly the other avenues are, and this is happening even with the population growing by 2.1% in the past year.

Retail spending per capita has declined by 2.6% in the past year, as shown here. Spending per person is now below trend after an extended period above trend.

This brings us to the second reason why we are cutting our spending.

We have already bought a lot of what we need during the pandemic. We could not travel so we embarked on a period of bringing forward planned expenditure on home renovations, landscaping, spas, swimming pools, new appliances, new furnishings, floor coverings and so on. We binged.

But you only need a new spa every four decades or so and now that we have had our binge there is a “hole” in spending which would otherwise have occurred this year and next.

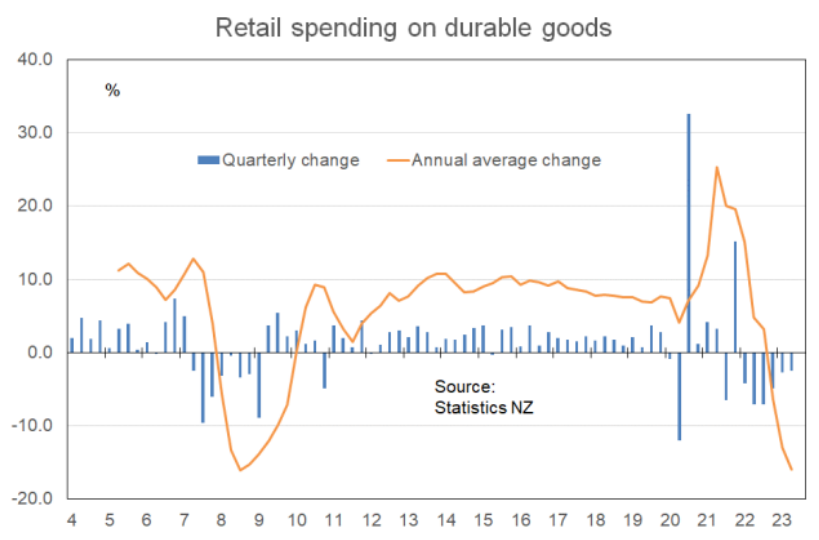

Hence the greatest spending weakness is for what we call durable goods. These are things which last a long period of time.

This next graph shows the durables binge most easily as the orange line representing the annual average rate of growth. Note the 2021 surge and the latest result of -16% which matches GFC weakness.

Speaking of the GFC, there is a factor which was in play back then which has also been in play now – falling house prices. Some people allow their spending to be influenced by their paper wealth and higher asset prices mean they will spend more. This would have accentuated the pandemic binge.

When asset prices fall, they will cut back on their spending. As recently expressed by the Reserve Bank, I also have a view that this effect is not particularly large. But it exists, so we’d best mention it.

Are there other factors helping to explain household spending weakness? Yes – we can now travel offshore again.

Normally, as in pre-pandemic – we would spend about $10bn travelling offshore. For the past year we have been able to do that again after the borders had been closed for two years.

Our determination to travel means we are allocating funds from other areas towards travel, accommodation, attractions, and offshore eating and drinking.

That is, extra weakness exists in spending domestically.

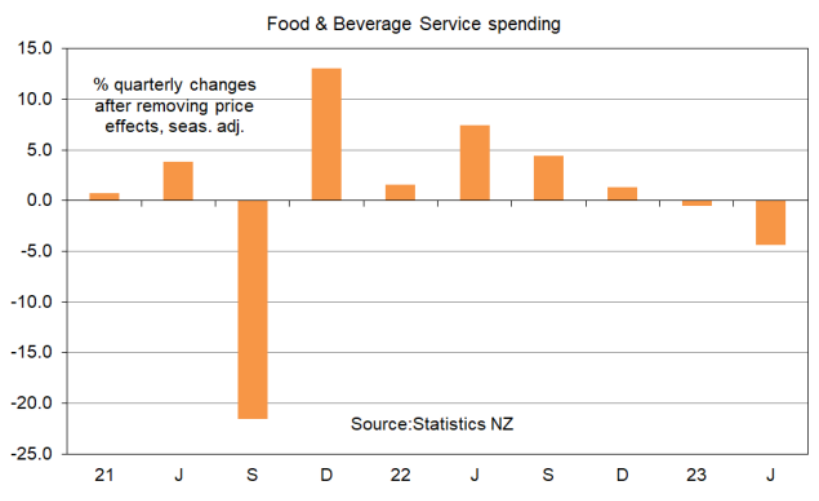

But there is an offset from people offshore coming here to engage in their revenge travel. In the year to June spending on Food and Beverage Services jumped by 14% – almost the exact opposite of the change in spending on durable goods discussed above.

However, this spending is fading and this likely reflects our having satiated our desire to eat out once pandemic restrictions were eased and our focus now on tightening the belt for a tougher environment. Eating out is one of the easiest things to cut back when times get tough.

Those tough times include a soaring cost of living – high inflation – which is another reason why retail spending levels are falling.

We have to keep buying groceries and paying things like insurance and rates, but our concerns about future price rises mean we are exercising caution when it comes to buying other things. This may be the case even if we can afford them.

Older people who have already lived through similar periods of high interest rates and other negative shocks have probably paid off their mortgages and are receiving some benefit from rising interest rates.

The current mortgaged generation will be in this position in 20-30 years time and a lot sooner for many.

But despite some extra interest income from bank deposits, these older people also will be exercising caution in their spending because of the soaring cost of living.

Many have progressed to fixed retirement incomes and ability to keep up with inflation probably weakens the older one gets.

Young people have a greater tendency to shift employer than people who are older and it is through changing boss that one generally gets the best remuneration increase in New Zealand.