Westpac with the note.

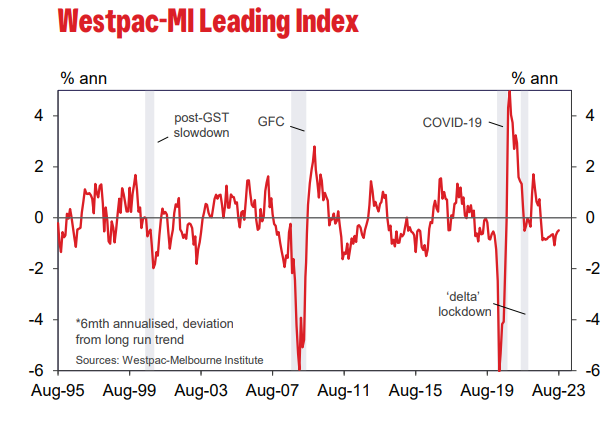

- Leading Index growth rate still negative at –0.5%.

- Negative reads have now persisted since August 2022.

- Indicator correctly predicted growth slowdown in 2023.

- Growth outlook for next 3–9 months remains poor with per capita GDP declines likely to continue.

The economy continues to move through an extended period of weakness. Despite another slight improvement this month, the Leading Index growth rate continues to track in negative territory, the measure having now been below zero for just over a year.

Negative prints for the Index indicate the economy is likely to grow at a below-trend pace.

This string of negative prints began in August last year accurately foreshadowed the sudden slowdown in the economy in 2023. Over the March and June quarters the economy has expanded at a 1.6% annualised pace – well below trend growth, which is closer to 3%yr.

Westpac expects this weak performance to continue over the next year or so with growth expected to come in at less than 1% for the year to June 2024. There may be some upside risks to that downbeat number now that population growth is likely to exceed 2% in 2023.

Even so, economic growth is likely to continuing lagging behind population growth with the pattern evident in both the March and June quarters, which saw GDP per capita contract by 0.3% in each quarter, likely to persist over the next year.

The Leading Index growth rate has improved marginally since the start of the year, from –0.73% in February to –0.50% currently, a lift of 0.24ppts.

Component-wise, the main improvement has come from stabilisations in components that had previously been weakening. Steadying consumer expectations and labour market assessments have added 0.11ppts and 0.2ppts respectively. The steadying in the yield spread as RBA rate hikes have come to an end has added a further 0.2ppts to the Index growth rate. There have also been more positive signals from both US industrial production (adding 0.15ppts) and dwelling approvals (adding 0.14ppts).

These improving signals have been partially offset by a sharp weakening in commodity prices in AUD terms (a 16% fall since February taking a third off the Index growth rate); and some slowing in monthly hours worked (–0.16ppts).

Overall, the mix is seeing a reduced drag from financial conditions and domestic conditions but continued weakness in international conditions, especially relating to commodity prices.

The Reserve Bank Board next meets on October 3. The Board is almost certain to hold rates steady for another month.

In the minutes to the September Board meeting it was again noted that “… some further tightening in monetary policy may be required should inflation prove more persistent than expected”. In making this decision, the most critical update will be the September quarter inflation report, which will not be available until the November Board meeting.

Given the overall tone of the minutes, it seems that the ‘hurdle’ for a further rate hike will be high and certainly not consistent with our current forecasts for inflation.

That will equate to an endless per capita recession.