The retirement system in Australia is built on the assumption that the majority of people will own their homes.

However, that assumption is collapsing due to falling homeownership rates and people carrying mortgage debt well into their retirement years.

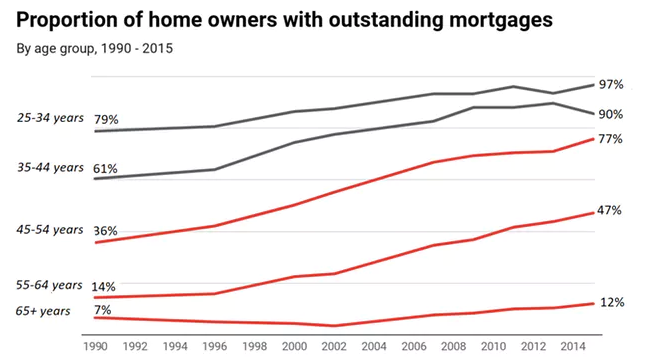

As shown below, older Australians are carrying larger mortgage debt into retirement (with notable rises in the 55-64 and 45-54 age groups):

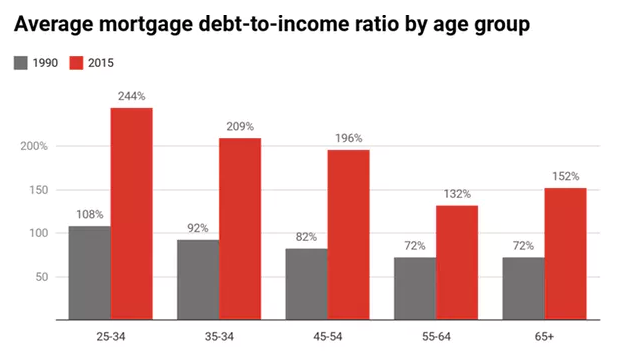

The situation will obviously have worsened materially since 2015:

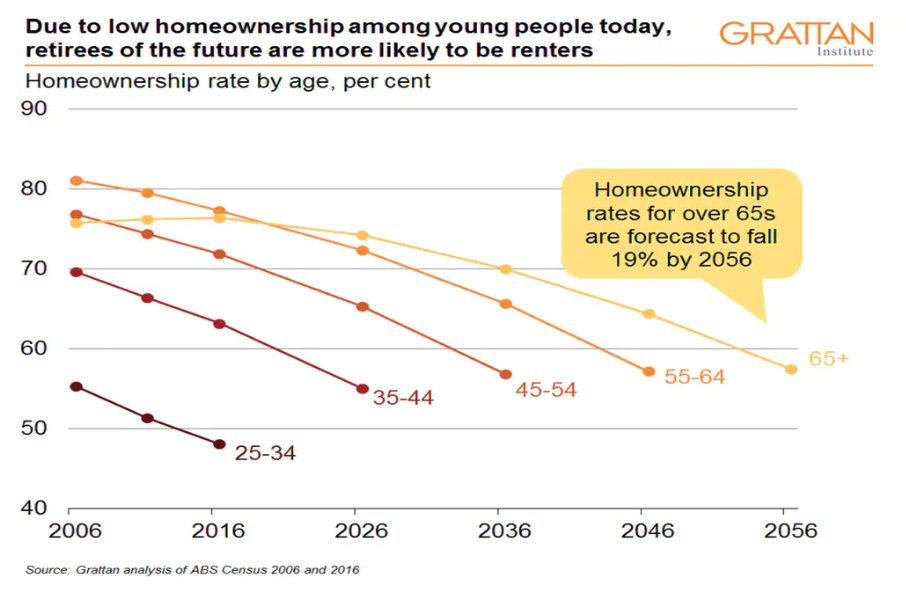

Meanwhile, the proportion of people over the age of 65 who own a home is expected to shrink from 76% now to 57% by 2056, according to the Grattan Institute.

Less than half of low-income pensioners will own a home in the future, down from more than 70% today:

Harry Chemay has posted an article in Michael West warning that the nation’s housing crisis, and the sharp fall in home ownership rates, risks blowing up the nation’s retirement system:

“At the heart of Australia’s retirement income system (albeit more whispered in policy circles than shouted) is the presumption of home ownership, unencumbered by debt. The rate of the Age Pension reflects this assumption”.

“Right across the working age spectrum, from 25 to 64, rates of property ownership have declined over the past four decades”.

“At present, the full Age Pension for a single person is approximately $27,600 per year. For a couple, the equivalent amount is approximately $42,000. To which the soon-to-be-increased Commonwealth Rent Assistance (CRA) may add a further circa $4,500 per year at best”.

“According to CoreLogic data, the current median rent for all dwellings across the country is $577 per week, and $603 in capital cities”.

“Taking the nation-wide average, that’s approximately $30,000 in annual rent, which would obviously consume more than an entire single full Age Pension, and be met (just) only with the help of the additional Commonwealth Rent Assistance benefit”.

“In the case of a retired couple, the current median private rent would consume some 65% of their combined full Age Pension and CRA”.

“Those who have managed to break into homeownership aren’t exactly out of the woods either, with research done in 2019 showing that the proportion of homeowners aged 55 – 64 with outstanding mortgages had increased from 14% in 1990 to around 50% by 2015”.

“And of the main uses of super lump sums during 2016-17, mortgage and other debt retirement accounted for over 40% of such withdrawals”.

“It basically means: hitting retirement either as a renter or as a heavily indebted mortgagor is going to impact the retirement security of very many Australians, possibly putting pressure on both the Age Pension and superannuation system”.

“Whichever way governments of either persuasion slice or dice it, housing security and retirement security are two sides of the same coin”.

In summary, future retirees will increasingly rent, while others will carry higher levels of mortgage debt.

Both will put significant strain on the retirement system.