Westpac with the note.

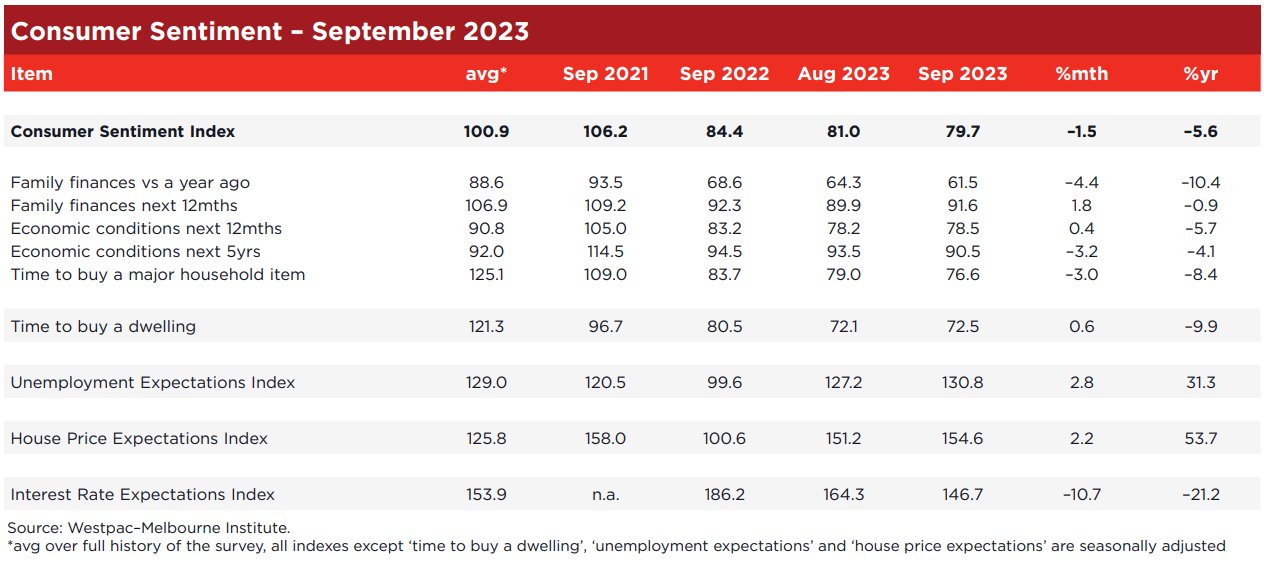

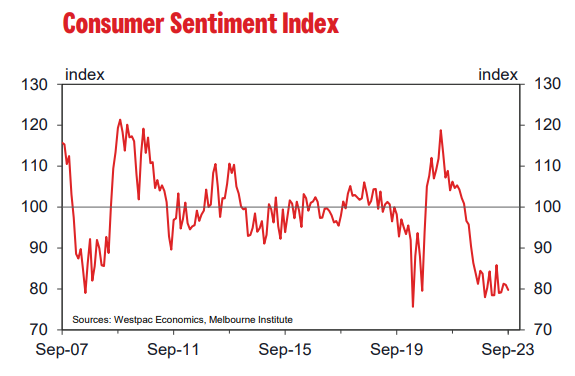

The Westpac-Melbourne Institute Index of Consumer Sentiment slipped 1.5% to 79.7 in September from 81.0 in August.

Sentiment has languished at deeply pessimistic levels for more than a year now. Since the survey began in 1974, the only comparable period of such sustained weakness was during the recession of the early 1990s when even weaker levels held for more than two years.

Persistent pessimism has continued despite easing fears of further interest rate rises. This has seen a clear lift in the confidence of mortgage holders, up 7.8% in the latest month.

However, this gain was more than offset by a 6.1% fall in the confidence of renters and a 5.8% fall in the confidence of consumers that own their home outright.

The strong message from survey detail is of ongoing intense pressures on family finances. Most notably, the sub-index tracking assessments of finances compared to a year ago recorded another 4.4% fall and is now at its lowest level in this current cycle. Those concerns would have been exacerbated by the 15% lift in petrol prices over the last two months, coming on top of already strong rises in rent and electricity.

When asked about the news items that resonated the most in September, the topics with the highest recall amongst consumers are: inflation (53%), budget and taxation (34%); economic conditions (34%); interest rates (25%) and employment (23%).

The recall numbers for inflation have fallen a little over the last three months but this remains the dominant topic by a wide margin, especially compared to interest rates. The cost of living remains the key negative for confidence in this cycle. While the ‘threat’ of rising rates is expected to ease further, a sustained recovery in confidence will only emerge when households are much more comfortable with the cost of living.

Consumers again assessed news on all topics as being more negative than positive, deteriorating significantly since June in the case of ‘budget & taxation’ and ‘employment’. News on ‘inflation’ and ‘interest rates’ was viewed less negatively than three months ago although 70–80% of consumers still report news on these topics as unfavourable.

It is noteworthy that ‘budget and taxation’ continues to figure prominently in recall results, and that the news on this front is viewed more negatively. This is despite a generally improving fiscal position and suggests that consumers may instead be looking for different news – namely, more support with cost of living difficulties – either direct or through tax relief.

There was a notable shift in interest rate expectations. Amongst those surveyed after the RBA decision, 48% expect rates to rise over the next year, down sharply from the 68% of those surveyed following the August RBA meeting. This follows two years in which every survey has found an outright majority of consumers expecting rates to move higher. That said, only 15% of consumers expect rates to be cut over the next year.

The component sub-indexes again showed mixed results in September.

As noted, the ‘family finances vs a year ago’ sub-index fell 4.4%, more than reversing a modest gain in August to hit a new 31-year low of 61.5. The fall came despite an improvement amongst those in the mortgage belt which was more than offset by big declines amongst renters, 18–34 year olds and low income earners.

Year-ahead expectations for family finances and the economy both improved slightly (1.8% and 0.4% respectively). However, both sub-indexes remain in pessimistic territory.

The ‘economic outlook, next five years’ sub-index fell 3.2% to 90.5.

The ‘time to buy a major household item’ sub-index fell 3% to just 76.6. This component is particularly troubling because, unlike the overall Index and the other components, it is tracking well below the levels seen in the recession of the early 1990’s – the average seen during that period was a much milder 91 The Westpac-Melbourne Institute Unemployment Expectations

Index rose 2.8% to 130.8 in September, nudging back above the long run average of 129 (recall that higher index reads mean more consumers expect unemployment to rise in the year ahead). The index has been moving sideways since mid-year after surging 32% over the previous 12 months. That suggests labour market conditions have softened on a year ago but have not deteriorated further since the middle of 2023.

The ‘time to buy a dwelling’ index posted a very slight 0.6% gain but at 72.5 remains at very weak levels overall.

The Westpac Melbourne Institute House Price Expectations Index rose a further 2.2% to 154.6, a new cycle high. Over 65% of consumers expect prices to rise over the next 12 months. The Index is now 70% above the recent low in November 2022 and only 5.5% below the peak during the housing boom in 2021.

Consumer risk aversion eased a touch after hitting new record highs back in June. Updates on our ‘wisest place for savings’ questions, run every three months, show ‘safe-haven’ options and paying down debt continue to be heavily favoured. Over half of all consumers nominate either ‘bank deposits’ (33%) or ‘pay down debt’ (23%) as the wisest place for savings.

Conversely, very few consumers favour riskier options. Just 7% nominate ‘real estate’ and shares respectively.

The Reserve Bank Board next meets on October 3. The Minutes of the August Board meeting showed that the Board had become more confident that inflation was heading in the right direction and that tight conditions in the labour market had eased somewhat.

The evidence from the September Consumer Sentiment survey is pointing to ongoing weakness in consumer demand.

Spending in the June quarter was reported in the national accounts to have increased by only 0.1% following tepid gains of 0.3% in the preceding December and March quarters.

Under these conditions the case for the Board to increase rates further is quite weak.

We continue to expect rates to remain on hold until the August Board meeting in 2024. By then we anticipate inflation to have fallen to 3.4%; the unemployment rate to have risen to 4.5% and annual growth in consumer spending to have slowed to just 0.8%.

By then it will certainly be time for both the monetary and fiscal authorities to provide some much-needed support for Australian households.