By Belinda Allen, senior economist at CBA:

Key Points:

- We expect the RBA to leave the cash rate unchanged at 4.10% in September, for the third consecutive month.

- The hurdle to hike rates again is high and the data flow since the August meeting has been on the softer side.

- There is no catalyst to push the cash rate higher in September.

- We expect the cash rate to be on hold for the remainder of 2023 as prices, wages and activity data indicate no further tightening is required. We then expect an easing cycle to commence in Q1 24, although the clear risk is a later start date.

The RBA on hold in September

The coming week is a big one for the Australian economy and financial markets. The RBA September Board meeting is on Tuesday 5 September, in what will also be Governor Lowe’s last RBA decision.

Deputy Governor Michele Bullock formally takes over on Monday, 18 September. Governor Lowe will also deliver a speech on Thursday titled “Some closing remarks” at the Anika Foundation/Australian Business Economists in Sydney.

Also out next week will be the Q2 23 National Accounts data on Wednesday 6 September. We expect the National Accounts to show a relatively weak set of numbers for domestic demand, but with GDP growth expected to be boosted by a large contribution from net exports.

We currently have pencilled in a small quarterly lift in GDP of ~0.3%. We will firm up our estimate early next week once the remainder of the partial data is released.

The National Accounts data will include readings on how the expenditure side of the economy (household spending, dwelling and business investment) is reacting to higher interest rates.

Data on income, savings, productivity and unit labour costs will also be actively watched. The RBA has elevated the importance of productivity and unit labour cost data in recent speeches.

Based on the lift in employment and hours worked in the quarter versus the expected lift in GDP, we do not expect to see improvements in productivity in the quarter.

However, the RBA will not have the Q2 23 National Accounts data on hand Tuesday, instead just the partial data. Instead the main data the RBA will be deciphering will be the July labour force report, Q2 23 WPI and the July monthly CPI indicator.

Offshore news will also be discussed. The economic data flow out of China has deteriorated over the past month. Offsetting this is the fact that the Australian dollar has continued to fall, particularly against the US dollar. And in the US, stronger readings of economic activity, concerns over the US budget deficit and debt levels have led to higher government bond yields.

The RBA Board August Meeting Minutes also indicated a watering down of forward guidance “members agreed that it was possible that some further tightening of monetary policy might be required to ensure that inflation returns to target in a reasonable timeframe”. Our bolding.

The word ‘possible’ was added into the Minutes and was not included in the post meeting statement.

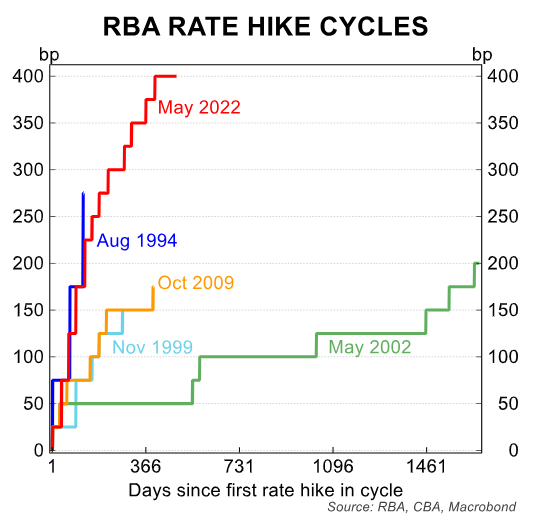

Overall we expect the cash rate to remain on hold at 4.10% in September. We do not view the meeting as a line ball call, unlike the finely balanced decisions in July and August.

The data flow over the past month and the large amount of rate hikes delivered to date make it a clearer decision in September.

However we expect the RBA will still run through the case to hike and maintain a tightening bias. Deputy Governor Michele Bullock noted in the Q&A following a speech on Tuesday this week that the RBA “may still need to raise rates again” and they will be watching the monthly databetween now and the end of the year.

Our most recent note on the RBA expand sour thinking on the outlook and risks to the cash rate beyond the September meeting.

Economic data since the August meeting

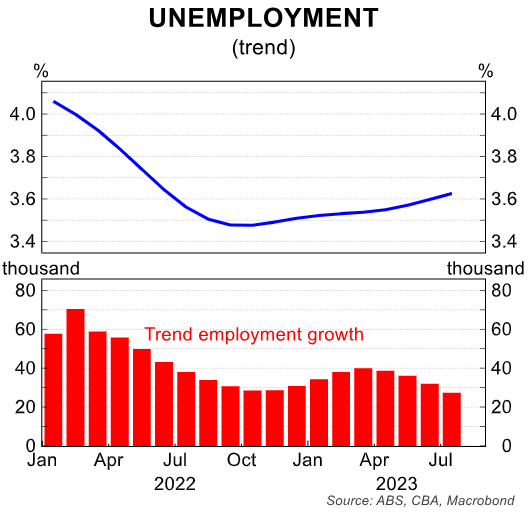

The July labour force survey was on the soft side. Employment fell by 14.6k and the unemployment rate lifted to 3.7% from 3.5%.

The ABS did note that seasonal factors could be changing with the timing of school holidays influencing when people start a new job.

The trend numbers through are slowing and suggests that the labour market is loosening, albeit slowly and from a very tight level.

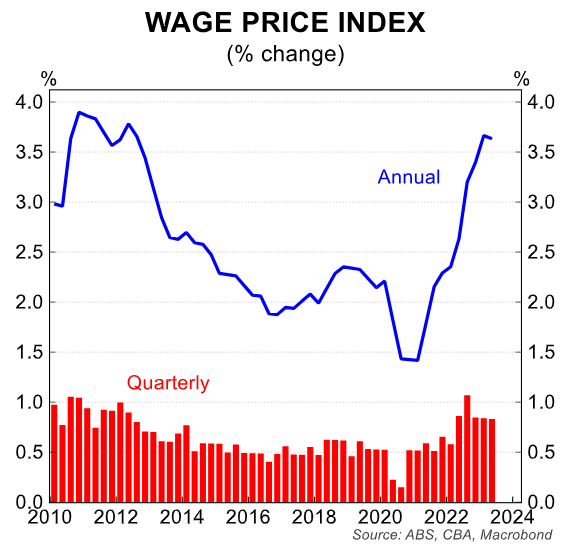

The Q2 23 WPI showed a lift of 0.8%/qtr and 3.6%/yr, below both consensus and the RBA’s expectations. There has been no acceleration in the pace of wages growth in the past three quarters, despite a resilient labour market.

Other prices data including NAB labour costs, SEEK advertised salaries and enterprise agreements suggest wages have risen in the past month.

Forward looking indicators of wages growth also suggest limited signs of acceleration.

CBA’s internal wage indicator for July has not shown an acceleration, although we note this would only have partially picked up the lift in minimum and award wages due to the indicator’s methodology.

The Q3 23 WPI released on Wednesday 15 November will capture the full lift in the minimum and award wage. The RBA’s implicit forecast we think is 1.4%/qtr.

Retail sales data released for July showed a 0.5% lift, after a 0.8% fall in June. The data has been volatile of late due to changing seasonal patterns. In annual terms, the pace of growth sits at 2.1%/yr.

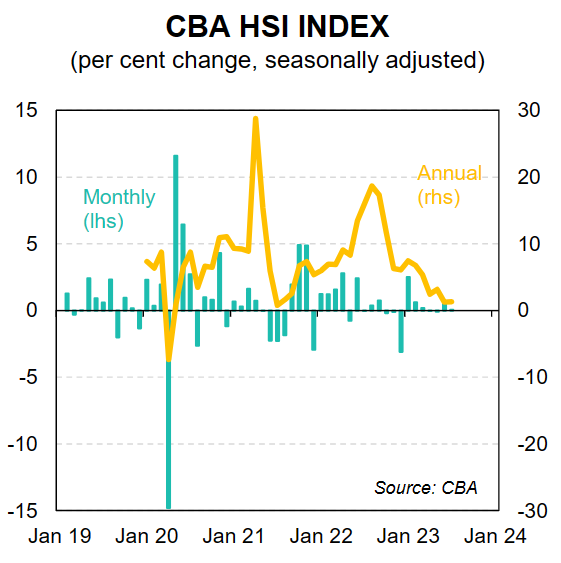

Our Commbank HSI Index for July, which captures total household spending (and not just retail spend), was flat in July, with annual growth sitting at just 1.3%/yr.

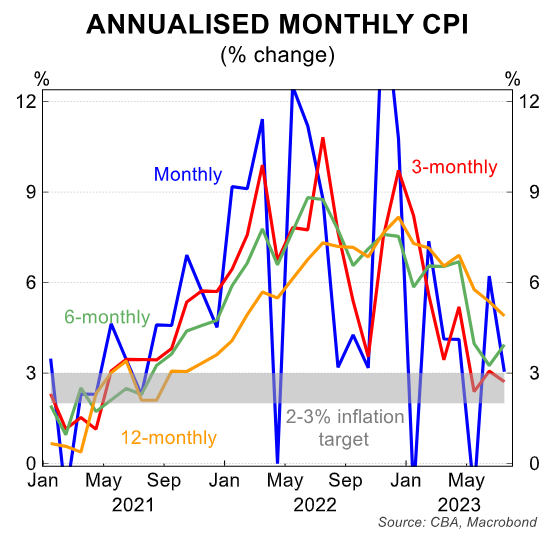

Given strong population growth of 2.8%/yr and inflation of 4.9%/yr, real per capita spending is very weak. And finally the July Monthly CPI showed a deceleration in the pace of inflation to 4.9%/yr, from 5.4%/yr in June. This is good news. However we do expect a bounce back above 5% in coming months as services items are measured.

The movement in petrol prices will also be important, but at this stage inflation is running in line or slightly below the RBA’s Q3 23 implied forecast.

The relative lack of data on services prices in the month of July, the main area of concern for the RBA will likely keep them on high alert.

Overall though inflation is heading in the right direction and adds to the considerable amount of softer data released this past month that makes the case for the cash rate to remain on hold.

Other factors to consider

Offshore factors can also factor into the Board’s thinking. Over the last month the news in the world’s two largest economies have continued to diverge. This is having some large consequences for financial markets.

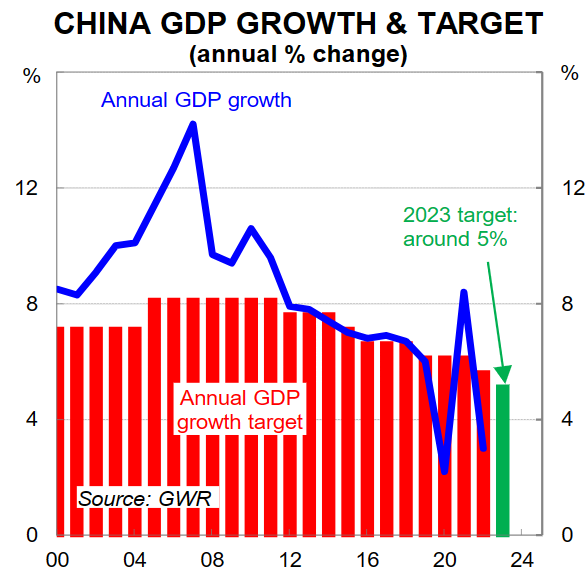

China’s economy has continued to lose momentum and the policy response to consistently weak economic data has been modest.

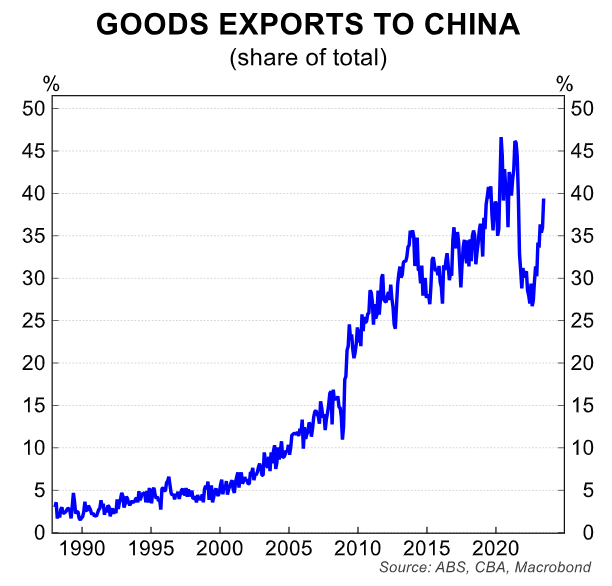

There are two key consequences for Australia. First the weak Chinese economy is a drag on commodity prices and demand for commodities, particularly for our iron ore exports if the property sector slows and requires less steel.

This sees a decline in the terms of trade and sustained weakness could mean a weaker Australian dollar, presenting some upside pressure to imported prices. But the size of this impact is small in our view, especially given the weaker consumer demand environment in Australia.

The RBA elevated China to one of three key domestic uncertainties in the August Statement on Monetary Policy.

Beyond a pullback in commodity prices, a slower domestic Chinese consumer could also see slower tourism and education exports in Australia.

Second, the US economic data has shown resilience recently. There is also a growing focus on the deteriorating budget and debt position of the US government. US bond yields have risen as a result.

In Australia fiscal policy is moving in the opposite direction, ie. pushing the budget back into surplus, and is working with monetary policy to slow aggregate demand.

In contrast to the US, the Australian budget position remains in good shape.