This week’s labour market data effectively killed the prospect of further interest rate hikes from the Reserve Bank of Australia (RBA).

On Tuesday, we received the Wage Price Index (WPI) for the June quarter, which came in well below economists’ and the RBA’s expectations.

Wages grew by 0.8% over the quarter, below expectations of a 1.0% rise. Over the year, wage growth fell to 3.6%:

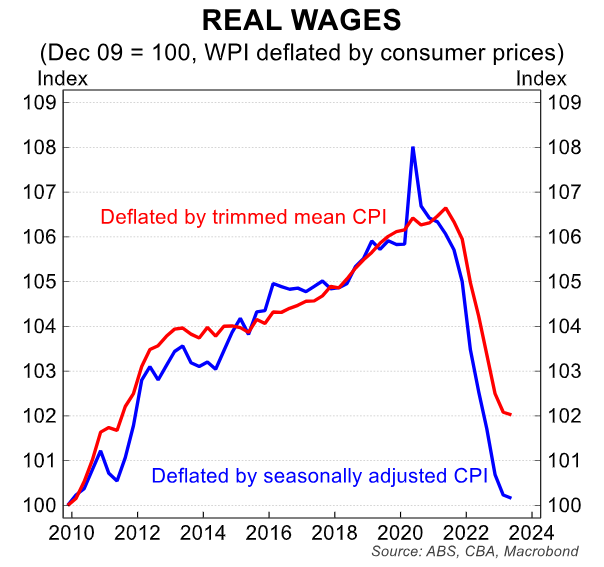

Real wages have fallen at an astonishing rate:

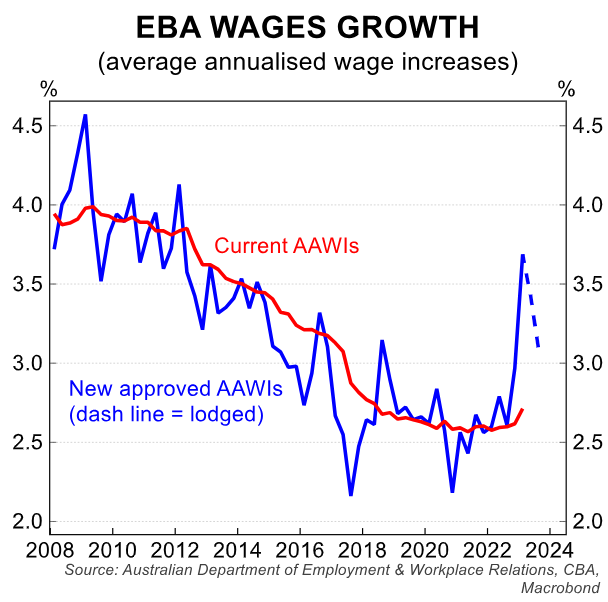

Enterprise agreement wage growth has also fallen (blue line below):

On Thursday, the ABS also released data on average weekly earnings, which complements the WPI.

Average weekly ordinary time earnings for full-time adults (FT AWOTE) rose by 3.9% over the year to May 2023, whereas average weekly earnings for all employees rose by 4.1%.

While the annual rate of FT AWOTE growth has accelerated in the last six months, the six-month annualised rate has slowed.

The annualised six-month change in FT AWOTE was 3.4%. This represents a slowing of growth from 4.3% in November 2022. It is also slightly lower than the 3.7% recorded in May 2019, before the epidemic began:

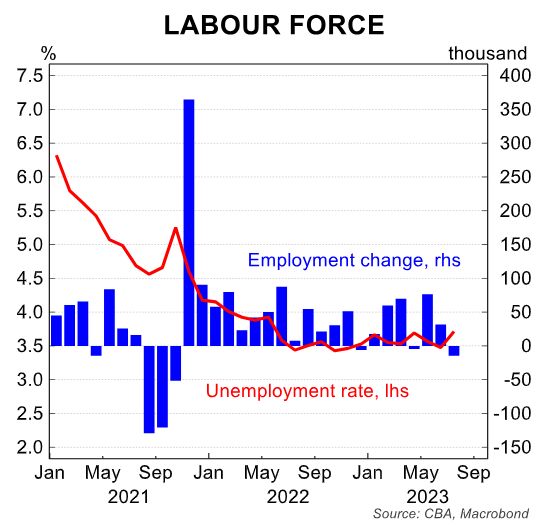

Thursday’s labour force report from the ABS also came in soft.

Employment fell by 14,600 in July, whereas the unemployment rate rose to 3.7%, the highest since May 2022:

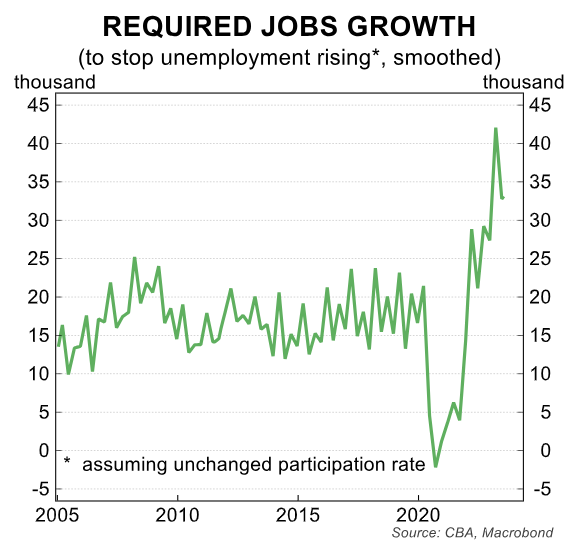

The next chart illustrates a key factor behind the labour market softening:

Australia’s labour supply is growing strongly due to the federal government’s extreme immigration policy.

The economy needs to generate around 35,000 jobs per month just to keep the unemployment rate stable.

Given labour demand is running well behind supply, unemployment will inevitably rise, which will drag wage growth lower.

While this is bad news for workers, at least it means the RBA will keep interest rates on hold.