CBA economist Harry Ottley has released a detailed analysis of Australian dwelling construction. Ottley forecasts that dwelling investment will decline by around 3.5% in 2023 and register only flat or slightly positive growth in 2024.

Housing is the most responsive sector of the economy to changes in interest rates, and the 4.0% of monetary tightening from the RBA will constrain the supply response to record levels of population growth.

Key Points:

- We anticipate dwelling investment and building commencements will remain soft in the near term.

- Interest rate cuts in 2024 should stimulate the sector but from a low base.

- We forecast dwelling investment will decline by ~ 3½% in 2023 and register flat or slightly positive growth in 2024.

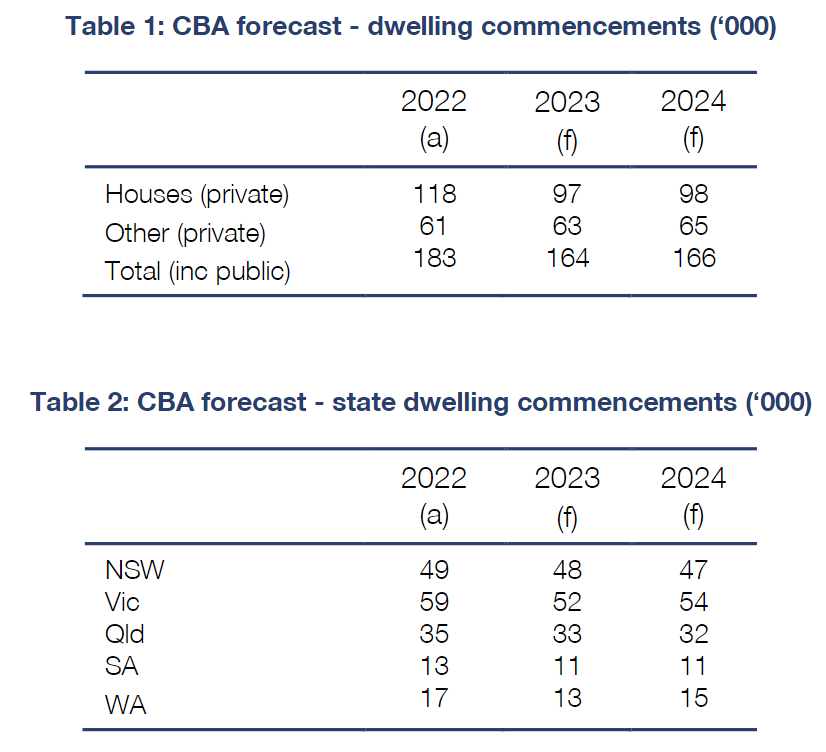

- We estimate building commencements will total 164,000 in 2023 and 166,000 in 2024.

This note outlines our latest views on the outlook for residential dwelling investment and building commencements to year-end 2024.

In the short term, dwelling investment is forecast to remain soft, with commencements drifting lower before starting to lift in 2024 as monetary policy is eased, supply challenges are slowly unblocked and demand increases.

Dwelling investment forecasts

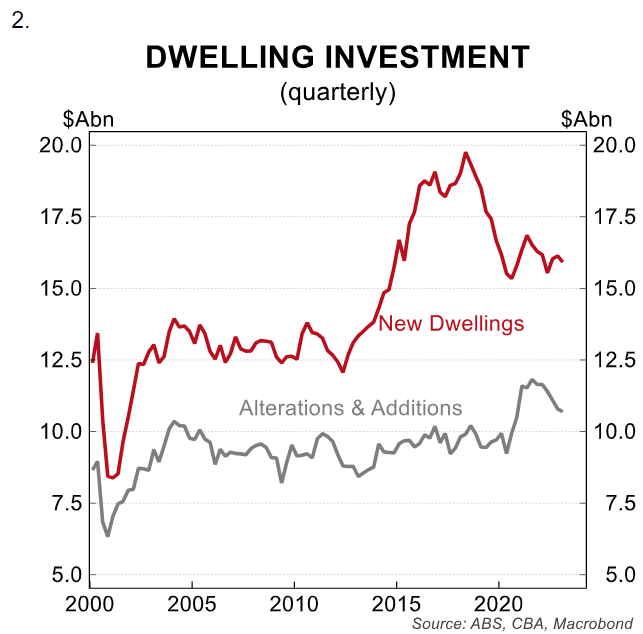

Dwelling investment accounts for ~5% of GDP in Australia. Around 60% of dwelling investment (since 2000) is the construction of new dwellings with the rest being made up of renovation activity.

Given dwelling investment is a relatively smaller portion of total GDP, weakness or strength in the sector does not have as big of an economic growth impact as household consumption or business investment.

Even so, it is of particular importance currently due to issues related to housing supply and large rent increases. A material increase in dwelling investment in the near term is unlikely, in our view.

For year-end 2023 and 2024, we forecast dwelling investment in through the year terms to be ~3½% lower and flat to a small increase respectively. As such, we anticipate dwelling investment will be a drag on GDP through the remainder of 2023 and most of 2024.

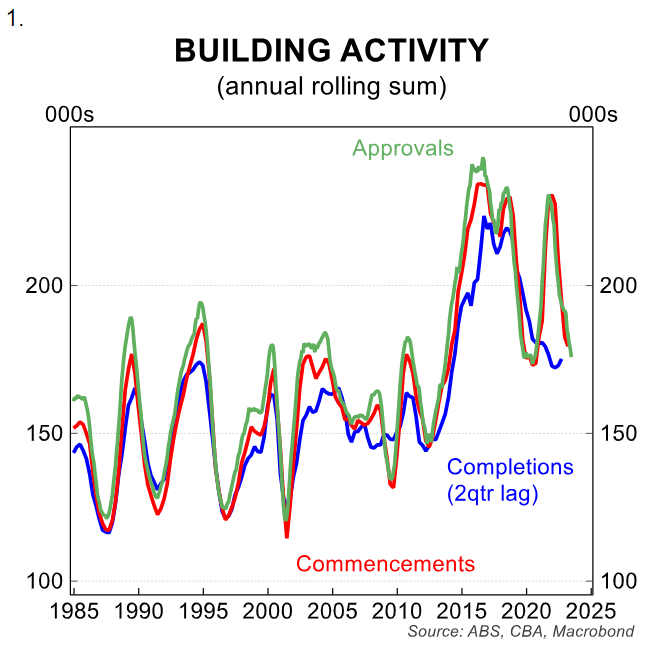

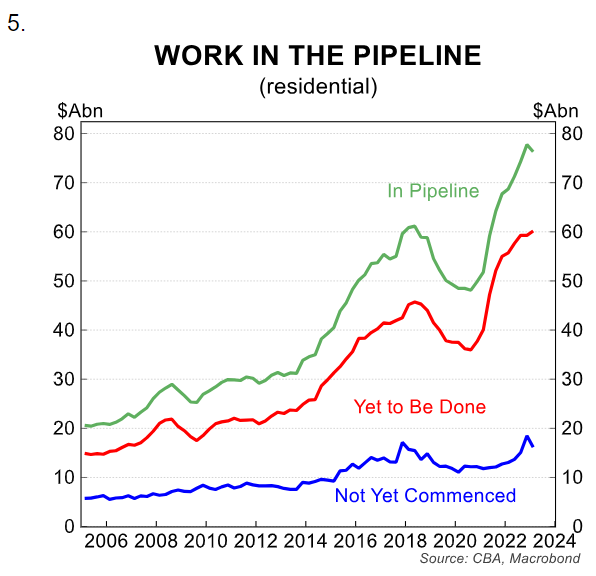

There is a risk that dwelling investment is stronger than our forecasts if the pace at which the large pipeline of work to be done increases, leading to a lift in completions and renovation activity (chart 1 and 5).

The RBA has stated that while material shortages and supply chain issues are largely resolved, labour shortages of key trades remains a significant constraint to the industry and so it is likely this pipeline of work will be more elongated than usual.

Tradespersons for the latter stages of builds have been particularly hard to come. This means completions and renovation activity renovation activity are being held up.

These delays are causing costs to rise, impacting cash flows and increasing insolvencies in the construction sector. More favourable costs and the ease of getting materials will not be able to increase the amount of done if labour constraints do not ease.

Construction workers are in high demand given the large pipeline of residential work and non-residential work in both the private and public sector.

Soft building activity to persist in 2023 and 2024

Building approvals are the highest-frequency measure of building activity. Typically commencements follow with a lag of around one quarter, though this can be longer for large developments. Building completions then follow.

As above, issues related to cost and labour/material constraints in the construction industry are extending the lag to completions at present (chart 1.).

There was a boom in approvals during 2020 & 2021 which was mostly centred on detached housing. The driving force behind this rise was a reduction in borrowing costs as monetary policy eased and targeted fiscal policy at the construction sector, the most significant of which was HomeBuilder.

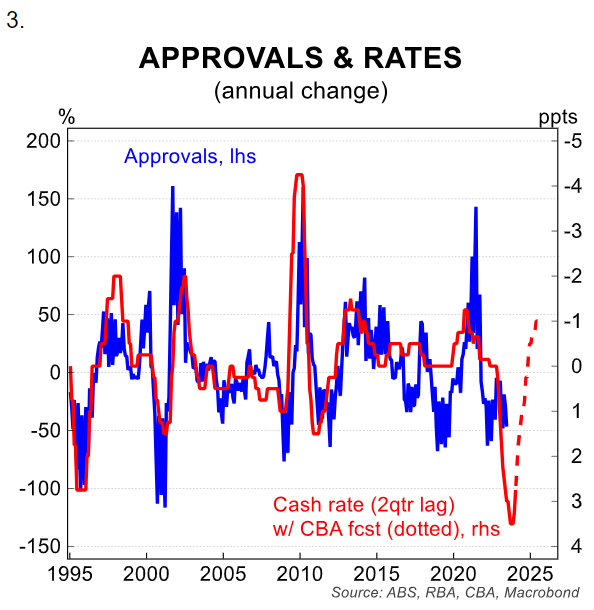

Since then, weakness has emerged. Approvals and construction activity more broadly are highly correlated with movements in mortgage rates (chart3).

While other inputs such as home prices and real income are also statistically correlated with building activity, the cost of borrowing has the most significant impact.

Indeed, housing is the most responsive sector of the economy to changes in interest rates. Given the rapid tightening cycle that began in May last year, it has been unsurprising to see approvals come off their highs.

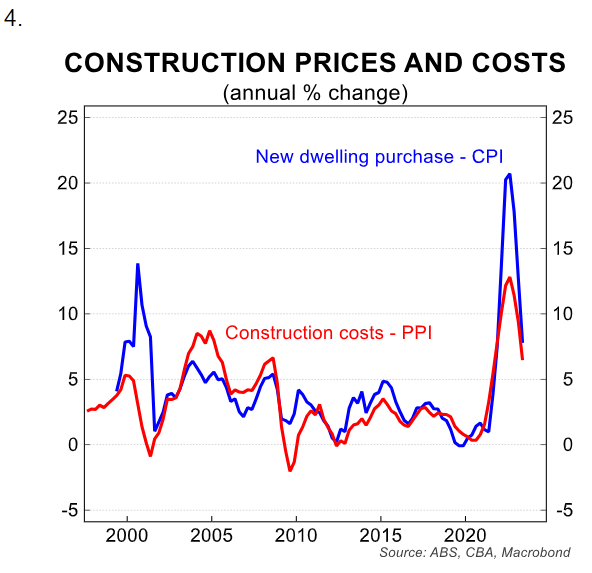

Real incomes are also in the negative and home prices until recently were in a downward cycle. Further, the cost of building a new dwelling surged during the pandemic years, reaching above 20%/yr in Q3 22.

The higher cost of building as well as borrowing for new dwellings has been a significant headwind for building activity. Prices for consumers had surged because input prices for the construction industry were inflated during the pandemic with exceptionally strong demand meeting constrained supply (chart 4).

Approvals have been weak this year. So far, we have 6 months of approvals data in 2023. With an average of ~13,100 monthly approvals, total approvals would come in at just 157,000 for the calendar year at current trends.

This would take annual approvals down to levels not seen since around 2011. Strong population growth and a tight rental market are so far not providing enough upward pressure on approvals to offset other factors.

The RBA left the cash rate on hold in August. We have updated our view and now expect the current cash rate of 4.1% will be the peak for this cycle.

The rate of change of the cash rate is what drives activity rather than the level. As can be seen in chart 3, the annual rate of change in the cash rate will fall from here which should support a slow recovery in approvals going forward.

If the economy evolves as we expect, the RBA is expected to cut rates to a more neutral setting in 2024. At this stage we anticipate the cutting cycle will commence in Q1 24, though the risk is a later start date to the easing in monetary policy. This easing in policy should stimulate building activity further.

The large lift in population as well as Federal and state government focus on unlocking supply challenges also provides some upside risks to activity in 2024.

Building commencement forecasts in detail

As discussed above, we anticipate building activity to remain weak in the short term.

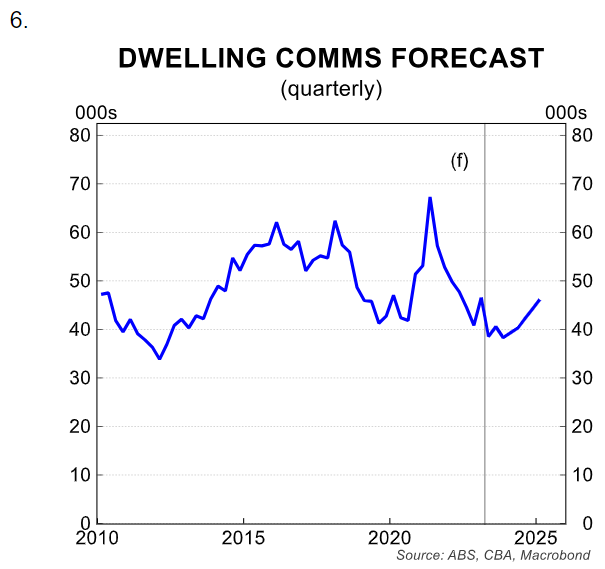

A total of ~183,000 dwellings were commenced in 2022. We forecast this number to fall to 164,000 in 2023 before seeing a modest rise to 166,000 in 2024.

Our previous set of forecasts for commencements, released in November last year, also had 164,000 in 2023 and we see no reason to change that forecast based on current trends.

For 2024, we have downgraded our forecast (from 177,000) due to current weakness and a larger and more prolonged hiking cycle than we had anticipated in November last year.

Quarterly commencements are expected to remain subdued through the remainder of this year before starting to lift modestly from low levels in early from 2024.

The lag from approvals to commencements means that total commencements for 2024 will be only marginally stronger than in 2023 despite a solid upward trend emerging in quarterly figures.

There are several risks to this forecast, mostly related to the monetary policy outlook.

On the downside, if the RBA does indeed raise rates again this year, approvals are more likely remain softer for longer.

Also, there is risks in terms of the timing of the RBA’s cutting cycle, which we currently have starting in Q1 24. If the cuts came later, building activity is likely to be weaker than currently forecast for 2024.

It is also worth noting some of the upside risks that fall outside the usual drivers. These include the current stress in the rental market incentivising renters to decide to purchase anew dwelling and developers entering the market to take advantage of structurally higher rents and easing cost pressures.

Persisting labour constraints would be a headwind to these influences particularly given the large pipeline of Federal and state government capex spend.

Policy support from Government that stimulate supply such as flagged zoning reform can also boost activity, though the likelihood of this remains unclear and timelines could be too tight for our forecast horizon.

Incentives for build to rent are another slated policy option that could boost approvals (especially for apartments) but again the timeframe where we could see a significantly impact of this is over the medium term.

Tables outlining our headline forecasts along with state breakdowns are below.