Yesterday’s monthly inflation revealed where Australia’s inflation problem is coming from.

Straight from Albo’s front door to you. Westpac has the details:

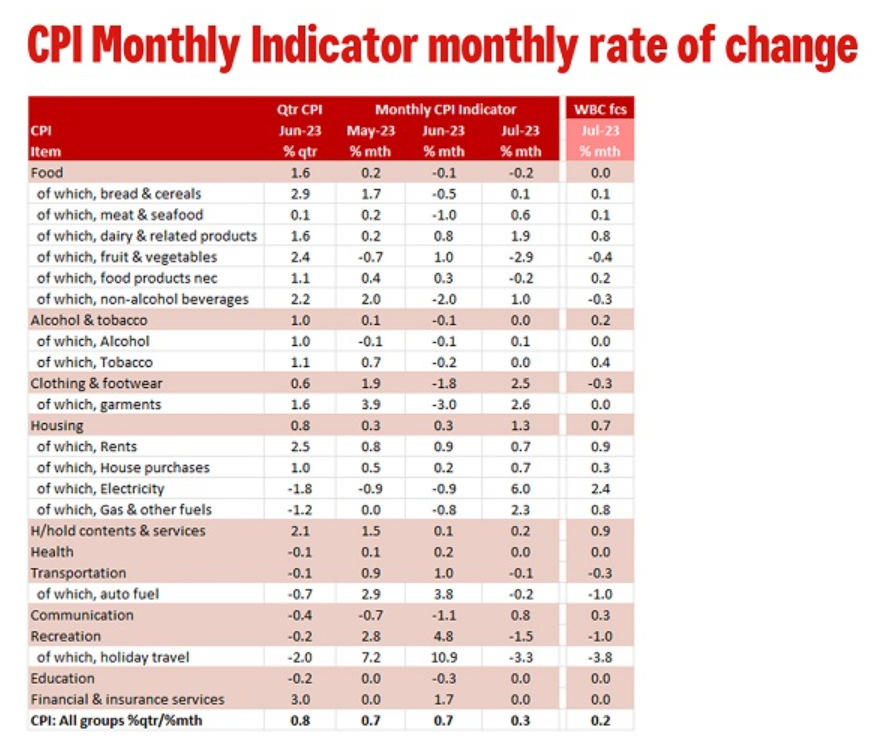

The Monthly CPI Indicator printed 0.3%mth/4.9%yr, very close to Westpac’s 0.2%mth/4.8%yr forecast but quite a bit softer than the market’s 5.2%yr forecast.

As expected, electricity presented a key upside risk printing 6.0%mth vs 2.4%mth forecast. Also on the upside was gas & other fuels (2.3%mth vs 0.8%mth forecast), auto fuel (–0.2%mth vs –1.0% forecast), clothing & footwear (2.5%mth vs -0.3% forecast) and dwelling purchases (0.7%mth vs 0.3%mth forecast). All up housing surprised to the upside at 1.3%mth vs 0.7%mth forecast.

Offsetting was falling prices for food (–0.2% vs flat forecast), recreation (–1.5%mth vs –1.0% forecast).

We will process the numbers in more detail and will make any revisions that are necessary, with note to the stronger than expect housing costs but weaker household contents & services. Overall, with a headline print so close to our forecast we doubt any revisions will be significant.

As such it is also consistent with out view that there is no near term pressure for the RBA to increase rates again.

In short, over the last three months, Alboflation in energy and rents – derived from failed gas policies (plus spillovers) and mass immigration – has added 1.5% annualised to the 6.8% total.

But, the broader economy is deflating much faster than Alboflation is. Over the last month alone, Alboflation in rent and energy added an astounding 0.5% before spillovers.

We should add back in some inflation for stronger wages without immigration. But wage growth was never very strong so it would not add much.

Moreover, it would mean real wages were actually growing instead of falling and the RBA would be slashing rates into outright deflation. Broad living standards would be rising at a good clip.

What a shocking economic mismanager for workers this government has been.