We have already seen multiple reports on loss-making investors pulling the pin and selling their homes to avoid further losses.

The next chart from CoreLogic encapsulates the trend, with investors accounting for 32.7% of new for sale listings, according to CoreLogic:

That is up from a decade average share of 25% of new listings.

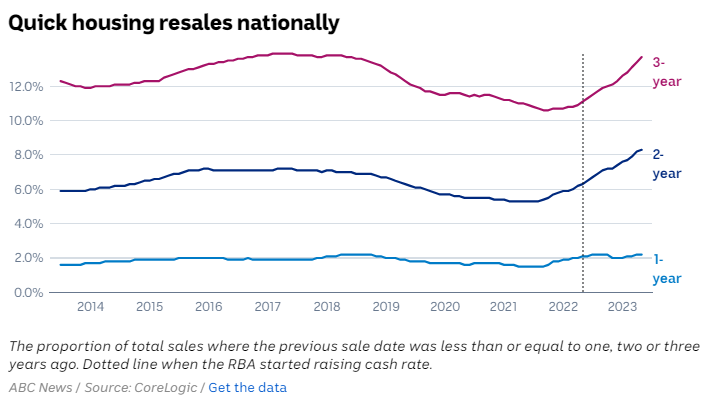

Now The ABC is reporting that the share of homes for sale that were purchased less than two years ago is at its highest level since at least 2014, reflecting rising levels of mortgage stress:

“We’ve seen a lot of stock that’s recently come on that has turned over in the last one to three years”, Brisbane real estate agent Jett Jones said.

“A lot of the first-time buyers that might have overextended the budget have come back and said, ‘Yeah, look, we need to sell'”.

“Or a lot of the time as well we’ve had investors that have said, ‘Yeah, we want to retire,’ or, ‘We need to get rid of it because it’s costing too much for us to keep the property now'”, she said.

According to CoreLogic, 8.3% of homes sold have previously changed hands within the previous two years, representing a significant increase since a pandemic low in mid-2021.

Almost 14% of properties sold in Australia in April had previously changed hands during the preceding three years.

According to Eliza Owen, CoreLogic’s head of Australian research, house flipping typically rises during booms as investors seek quick profits.

However, this time around an exceptionally high number of homes are being sold at a loss after being held for less than two years.

“We’ve seen these short-term loss-making resales of two years or less go from 3.4% of loss-making resales in the March quarter of 2022 to over 12% in the March quarter of 2023”, Owen says.

“So a lot more short-term sellers are willing to sell at a loss at the moment”.

Owen believes this reflects an increase in forced sales as those who purchased at ultra-low interest rates during the pandemic find themselves unable to keep up with rising mortgage payments:

“That could be because of issues of mortgage serviceability”.

That is, “people having no choice but to sell into a market that’s not as strong as when they purchased”.

“This is a different kind of short-term resales environment that we’re in”.

“It’s not so much about speculation — it’s some investors who maybe can’t hold on to their property because they’re facing higher mortgage rates; owner-occupiers, first home buyers who have potentially gotten in over their head”, Owen said.

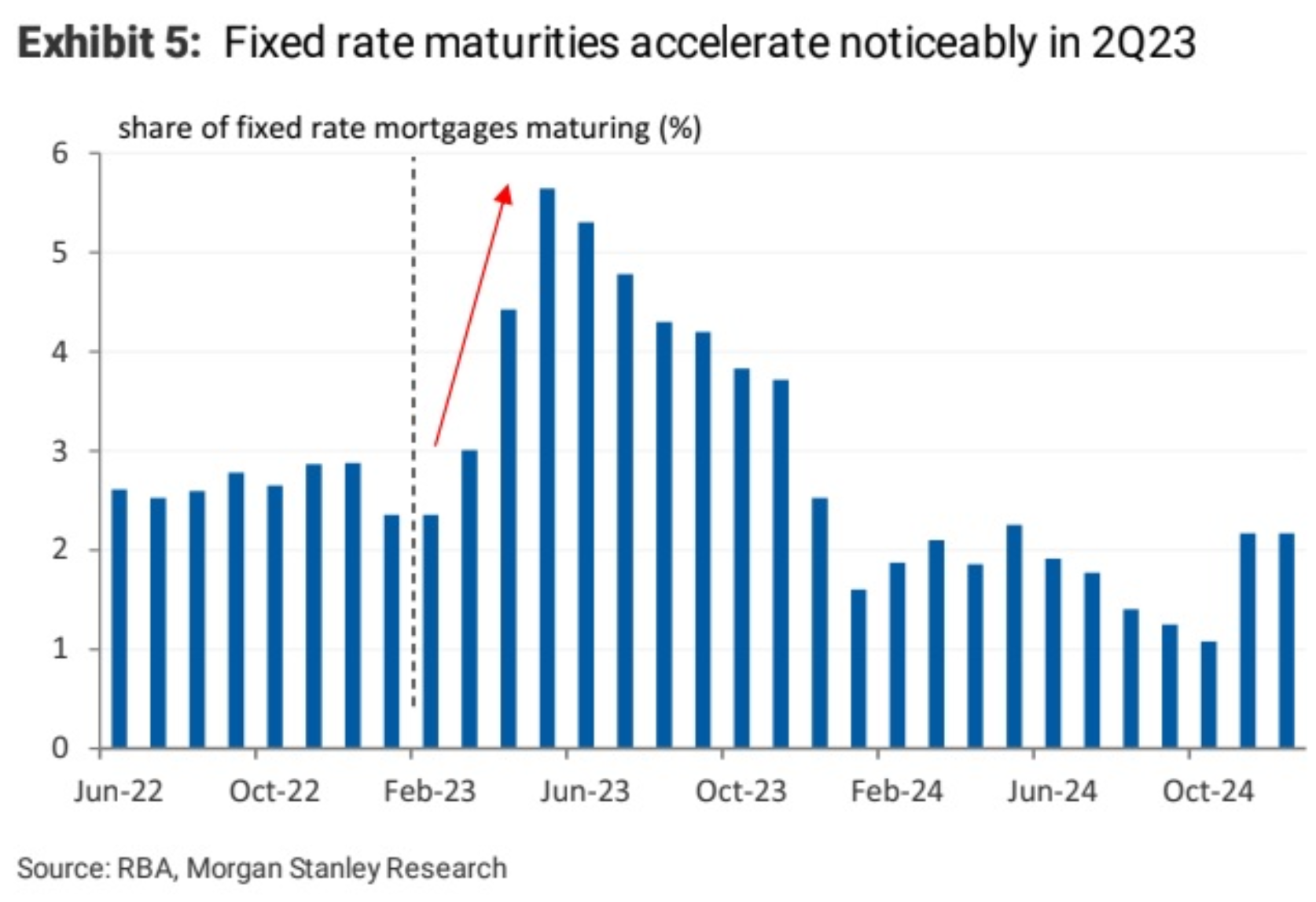

Logically, forced property sales should rise given we are currently at the peak of the fixed rate mortgage reset, which will see borrowers switch from cheap pandemic fixed rates of 2% to variable rates approaching 7%:

There were nearly 500,000 fixed rate mortgages scheduled to expire over the second half of 2023, which will push some mortgage holders into negative cash flow positions, forcing them to sell.