The intergenerational lottery has been won by the baby boomers.

For decades, successive Australian governments have stacked policy in favour of the old over the young.

We’ve provided huge tax benefits to the elderly. Older persons can earn significant incomes that are mostly tax-free, whereas young people earning the same amount must pay up.

Baby boomers have by far the highest rate of home ownership in Australia and were fortunate to have entered the market when houses were still fairly priced.

They then reaped the benefits of rapid housing price appreciation, while younger Australians have been priced out.

Many baby boomers have also been able to purchase one or two investment properties.

Most decent jobs did not require a higher education 40 to 50 years ago. However, most boomers who did attend university received free education, whereas tuition for younger Australians has become a substantial financial barrier early in life.

For baby boomers, the pandemic was a financial boon:

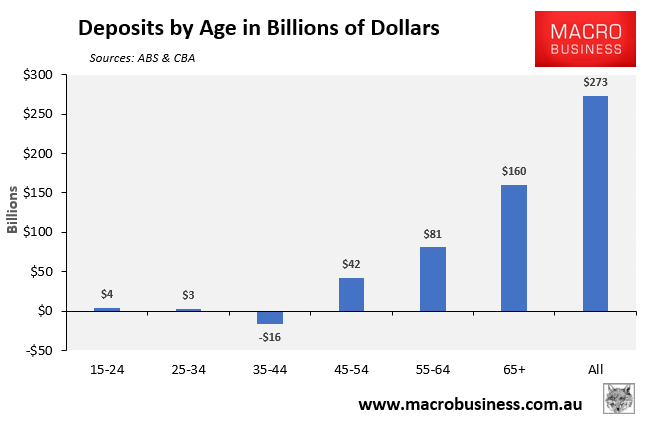

According to Australia’s national accounts, Australian households saved an astonishing amount of money during the COVID-19 pandemic, thanks to the government’s various stimulus packages and reduced spending during lockdowns.

However, as shown in the following graph, the majority of these savings ($160 billion) have gone to Australians aged 65 and more, followed by Australians aged 55 to 64 ($81 billion):

Younger Australians under 45, on the other hand, have seen their savings fall, with those in the important property buying and child-rearing demographic of 35 to 44 being the hardest hit.

Because Baby Boomers have the highest rate of house ownership in the country (most without a mortgage), they have also had the greatest increase in wealth since the pandemic began.

According to Roy Morgan’s Wealth Report 2023, which was released this month, Australia’s wealth climbed by 7.0% between March 2020 (pre-COVID) and March 2023.

This gain in wealth was mostly driven by an increase in the value of owner-occupied homes, which grew by 43.2%, from $4.16 trillion to $5.95 trillion.

Currently, half of the population, predominantly homeowners, account for 95.4% of Australia’s net wealth.

By contrast, the bottom half of the population, largely renters, only accounts for 4.6% of Australia’s net wealth.

Post-COVID, the Boomers’ dream run has continued:

Right now, there are three Australias.

Rapid interest rate increases by the Reserve Bank of Australia (RBA) have a direct impact on roughly one-third of mortgage-holding households, particularly Generation X and Millennials with young children.

Their mortgage payments have increased by about 50% while their disposable income has been eroding at the quickest rate on record due to inflation and greater cost-of-living:

Source: Tarric Brooker

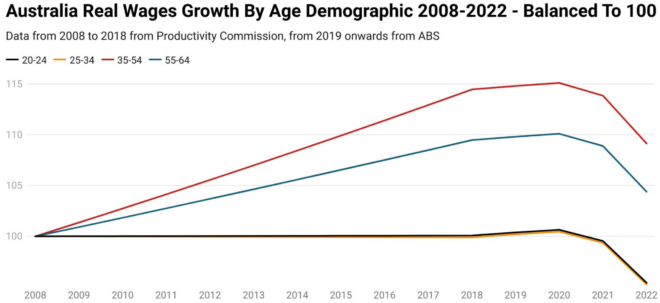

Australians under the age of 35 earn less in real terms than they did in 2008.

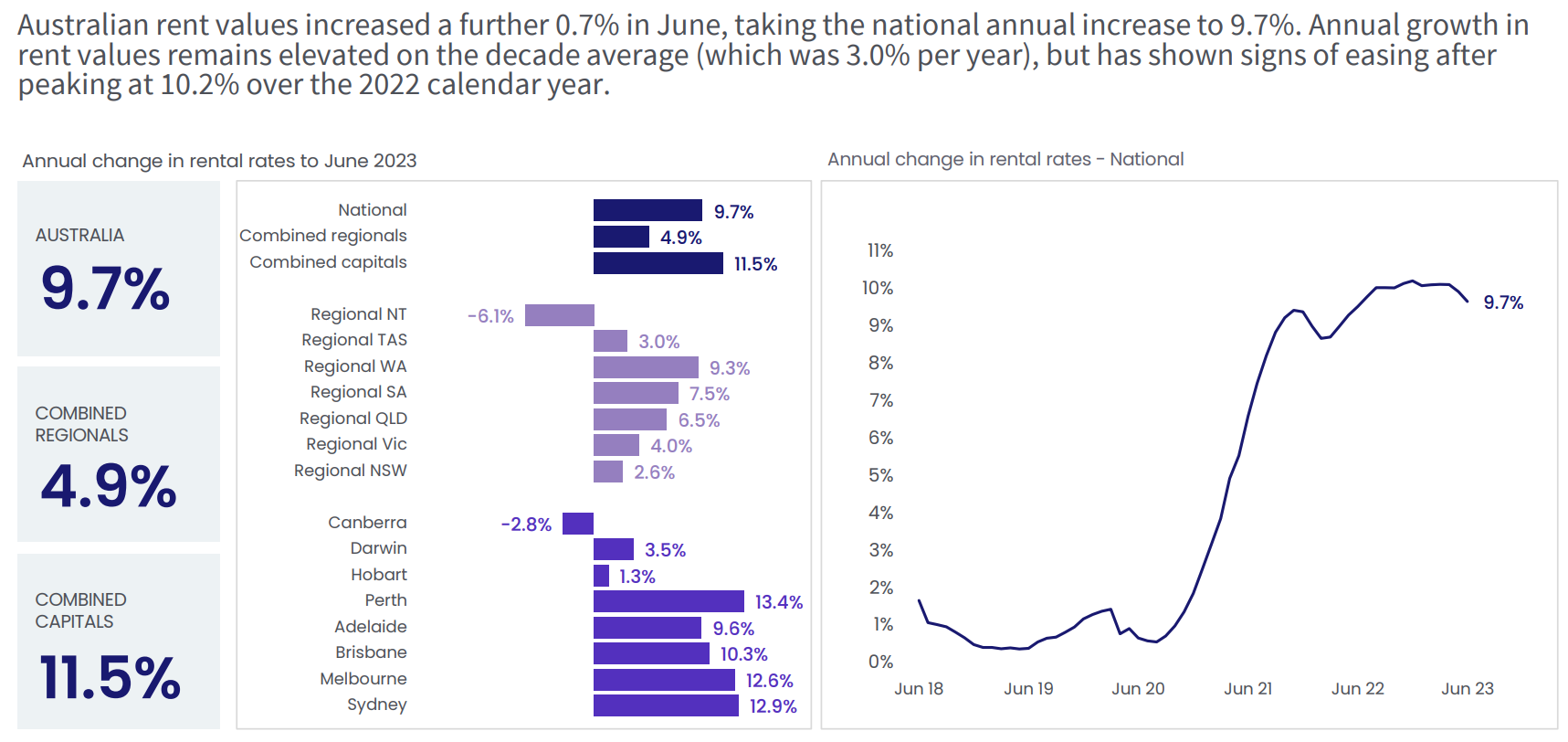

Another one-third of renting households (mostly young) are being impacted hard by some of the fastest rent increases on record, as well as plummeting real wages, which is limiting their discretionary spending.

Rents increased by 9.7% nationally and 11.6% across the combined capital cities in the year to June, according to CoreLogic, driven by record net overseas migration and a chronic scarcity of stock:

Source: CoreLogic

The remaining third of Australians are dominated by older generations (headed by baby boomers) and are on the other end of the economic spectrum.

They generally own their homes outright and are unaffected by rising mortgage rates nor rent increases.

Some baby boomers are even profiting from rising rents, as they own a sizable portion of the nation’s investment properties (many of which are mortgage-free).

Meanwhile, unlike employees’ income, Australians on the aged pension have their payments tied to inflation, ensuring that their spending power remains stable as prices rise.

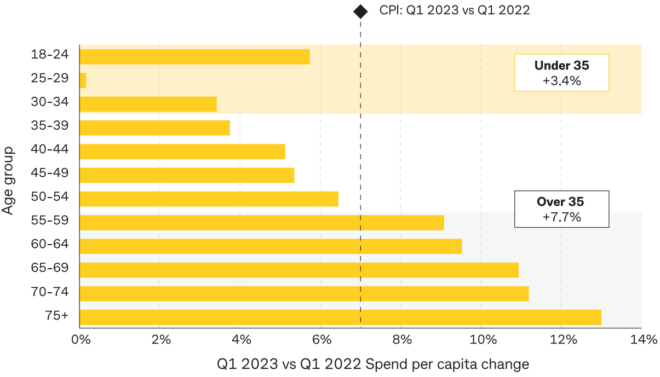

Baby boomers are spending a lot of money, which is fueling inflation:

Spending per capita for all age groups under 55 declined relative to the rate of inflation in the year to March 2023, according to an examination of seven million CBA members’ purchasing habits:

Source: CBA

In the year to March, Australians under 35 increased their spending by only 3.4%, less than half the rate of inflation.

As a result, the average young person is purchasing fewer products and services.

25 to 29-year-olds were the hardest hit, with spending remaining nearly flat in value over the previous year despite a 7% increase in prices.

Spending among the over 55s, on the other hand, increased faster than inflation in the year to March, with CBA customers over the age of 75 increasing their spending by almost 13%.

The CBA’s statistics also revealed that the significant increase in spending at cafés and restaurants reported by the Australian Bureau of Statistics was driven by older cohorts, who spent 18% more on dining out than the previous year, compared to a 7.1% increase among under-35s.

According to PEXA data from last month, more than one-quarter of all property sales in the eastern states – including dwellings and land – were done without a mortgage.

$122.5 billion worth of cash-funded homes sold in 2022, accounting for 25.6% of all residential sales in New South Wales, Queensland, and Victoria.

Mike Gill, PEXA’s head of research, explained that the majority of cash buyers were older homeowners who had previously paid off their mortgages.

Therefore, older generations are driving Australia’s household consumption and pushing up house prices, forcing the RBA to respond with higher interest rates, which is badly harming younger Australians with mortgages.

Older Australians also appear to have tightened their grip on the nation’s housing stock.

The data clearly shows that the spoils of the economy have gone to the baby boomers.

Now watch on as they devour smashed avocado toast.