CBA’s head of Australian economics, Gareth Aird, has described Australia’s strong house price rebound as “remarkable” given it has coincided with three 0.25% interest rate hikes from the Reserve Bank of Australia.

Aird also believes the supply and demand imbalance in the housing market is “concerning” and unlikely to improve in the near term.

The turnaround in property prices over the last three months has been nothing short of remarkable given the RBA has continued to lift the cash rate over that period.

Most forecasters will be frustrated at their home price models as the usual inputs didn’t pick this turning point. And the strength of the rebound in prices has caught almost everyone off guard.

Historically rents and vacancy rates have a strong inverse relationship. But home prices have generally been impacted by changes in mortgage rates rather than rents.

The old adage ‘this time is different’ has rung true.

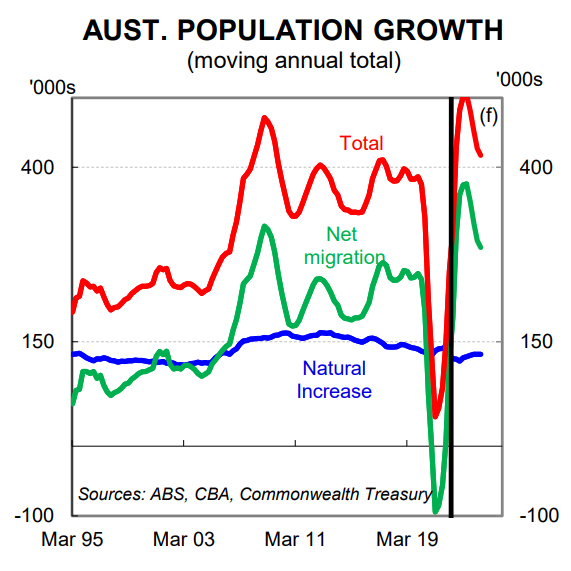

Population growth has massively exceeded expectations. The Commonwealth Government had forecast population growth to be 1.4% in 2022/23 in the October 2022 Budget.

But in the May 2023 Budget this forecast was upgraded to 2.0% this fiscal year and 1.7% in 2023/24.

Given the size of Australia’s population (26 million) the upgrades in the Budget are very significant from a levels sense. And by extension the impact these upgrades have on the underlying demand for housing.

Net overseas migration is forecast to be 400k in 2022/23 and 315k in 2023/24. Such outcomes would be much bigger than the pre-pandemic average of ~250k per year.

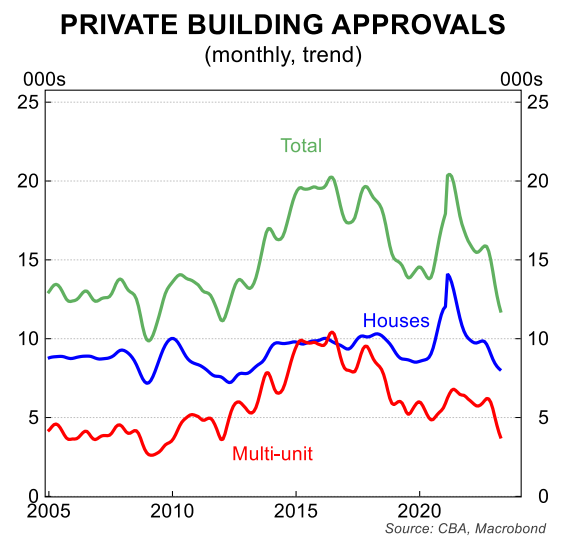

The surge in net overseas migration has occurred at a time when building approvals have collapsed. For context building approvals in April 2023 hit their lowest monthly number since April 2012.

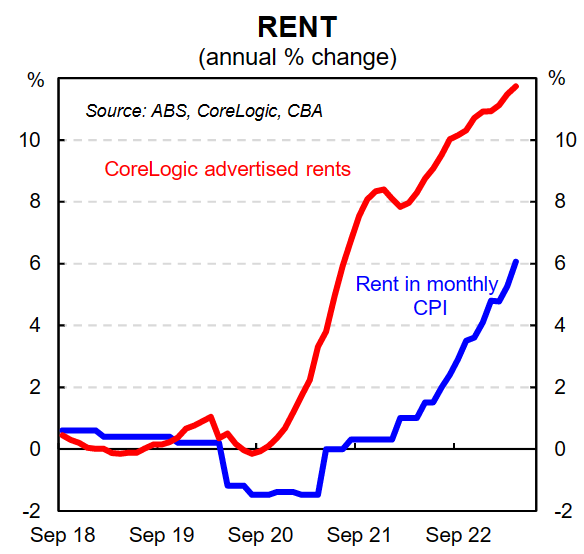

The upshot is that rental inflation is rising quickly.

RBA Governor Philip Lowe yesterday said the RBA has forecast rent inflation to rise to around 10%/yr.

Rents are part of the CPI basket. But higher interest rates don’t help the supply side of the housing equation as residential construction is negatively impacted by higher interest rates.

The problem in the housing market is quite easy to define. Everyone needs a roof over their head. So more people means more underlying demand for housing.

But the supply of new housing has not kept pace with the lift in population growth.

The solution to the problem is a little more complex. And it is not the role of a market economist to weigh into the policy debate.

We would simply highlight that the supply and demand imbalance in the housing market is concerning. And it does not appear like it will improve in the short run.

This means that home prices are likely to trend higher despite the deterioration in affordability.

Potential entrants into the housing market and renters feel the impact of the supply and demand imbalance most acutely.

Meanwhile many home borrowers with a mortgage are also feeling the pain of significantly higher mortgage rates.

It is no wonder consumer sentiment for renters and those with a mortgage sits at incredibly low levels.

The Outlook

Price momentum looks entrenched over the near term given the big imbalance between underlying demand and supply.

Further rate hikes could dampen price outcomes as they weigh on affordability and borrowing capacity.

But any additional policy tightening will put more downward pressure on residential construction and by extension upward pressure on rents.

Our point forecast is for home prices to lift by 3% in 2023 and a further 5% rise in 2024.

The risk to our dwelling price forecast in 2024 is firmly to the upside given we expect the RBA to be in an easing cycle.

We don’t have high conviction in our home price forecasts though given we are in the midst of a largely unprecedented situation of a highly aggressive RBA tightening cycle, record high immigration, surging rents and a collapse in building approvals.