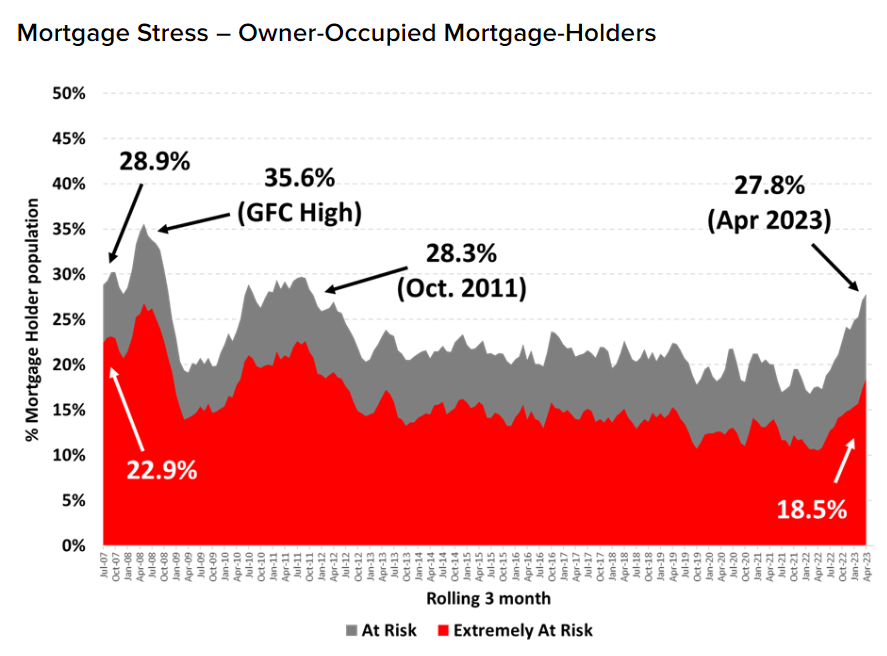

According to Roy Morgan, mortgage stress has reached its highest level since August 2008, with 27.8% of mortgage holders being rated ‘At Risk’ following 3.50% of interest rate hikes from the RBA:

Roy Morgan considers a borrower “At Risk” if their mortgage payments surpass a predetermined level (between 25% and 45%, depending on income and consumption).

The figures for April 2023 take into account ten RBA interest rate increases which lifted official interest rates from 0.1% in May last year to 3.6% by April.

The RBA subsequently increased the official cash rate another 0.25% in May and 0.25% on Tuesday to 4.10%, which is not captured above.

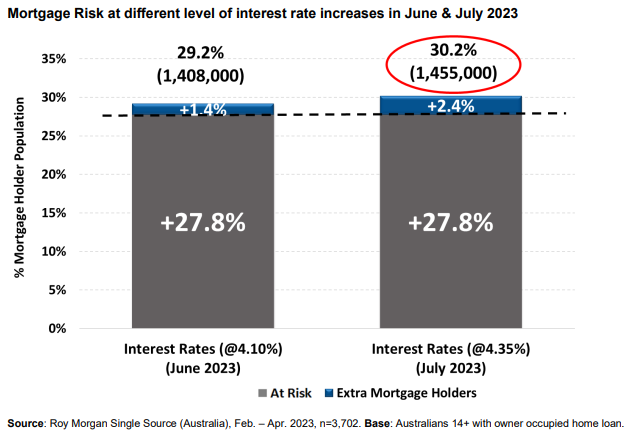

Nevertheless, Roy Morgan estimates that following the RBA’s latest 0.25% hike (to 4.10%), 29.2% of mortgage holders will be in stress.

And if the RBA hikes one more time (to 4.35%), then 30.2% of mortgage holders will be in stress:

Roy Morgan uses “a conservative model, essentially assuming all other factors remain the same”.

Thus, if unemployment rises materially, then mortgage stress would be higher than estimated above.

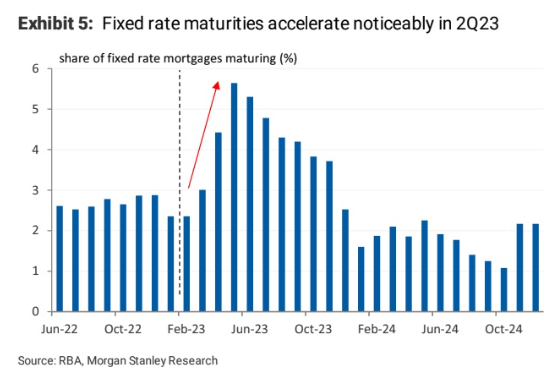

I will add that more that hundreds of thousands of fixed rate mortgages are scheduled to expire over the remainder of this year:

These fixed rate expiries will see mortgage rates jump from around 2% to 6%.

As a result, even if the RBA maintains interest rates at current levels, Australian households will continue to face increased financial strain as a result of the fixed-rate “mortgage cliff”.

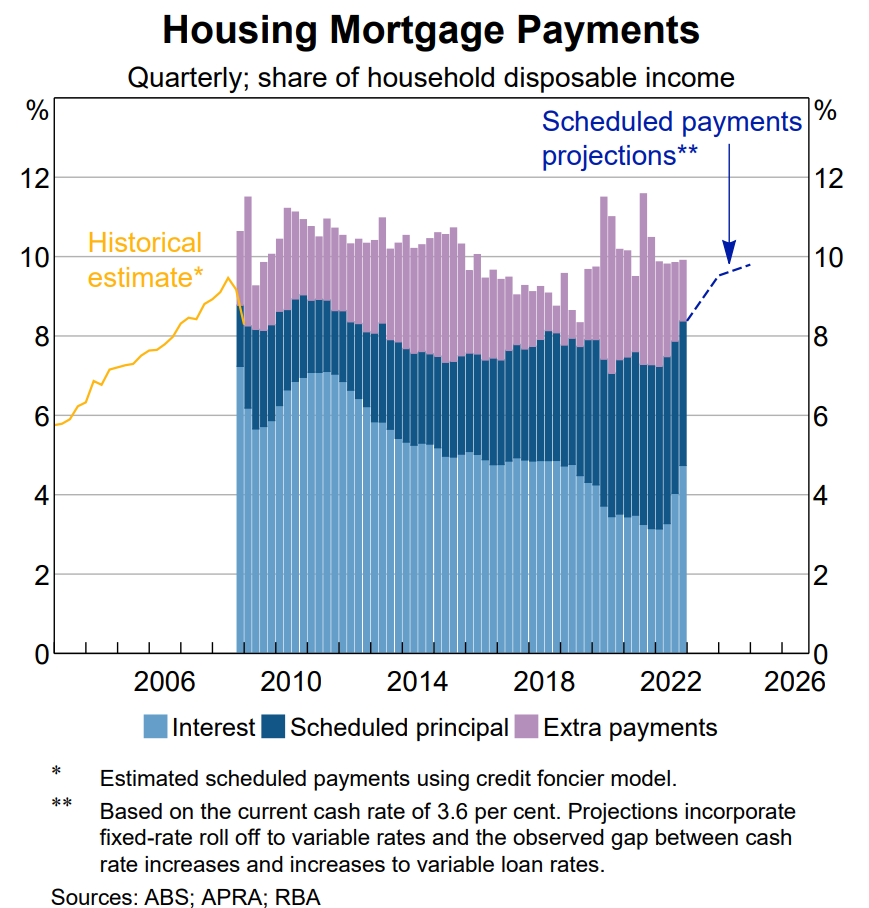

The graphic below, from the RBA’s most recent Financial Stability Review, illustrates the implications of this fixed-rate “mortgage cliff”:

As you can see, after the fixed rate mortgage reset is completed, scheduled mortgage repayments are expected to reach a record percentage of household income.

Mortgage rates have already climbed above the APRA-mandated 3% mortgage serviceability buffer, which was established when these fixed-rate mortgages were originated.

As a result, many borrowers risk falling into debt when their fixed-rate mortgage periods end.

Finally, data from S&P Global Ratings shows that mortgage arrears in Australia have risen to a two-year high.

S&P notes that 30-day prime mortgage arrears rose to 0.95% of borrowers in the March quarter, compared with 0.76% at the end of 2022; the latter followed a historic low of just 0.68% in the September quarter:

Mortgage arrears reached a record high of 1.69% in 2012, and the growing prospect of further increases in the cash rate could see arrears test this level again.