Yellow Brick Road chairman, Mark Bouris, does not expect Australian house prices to continue increasing in the face of rising mortgage rates.

Bouris predicts housing supply will surge during the spring as people feel the full impact of interest rate increases and are forced to sell – a “fire sale”.

Bouris told Sky News that “first and foremost the thing that creates increases in prices is when either one or two things occurs”.

“First if demand outstrips Supply. In other words, we get a an increase in demand and usually increase in demand is caused by more affordability and more affordability is created when interest rates fall”.

“I do not expect to see interest rates fall over the next six months or up to January or February next year and, therefore, I don’t expect to see affordability of houses at the current price increase”.

“That’s the first thing. The second thing that can create house price increases at the same rate that we had in the last six months is if all of a sudden, supply – if Supply stays the same, in other words stays very low”.

“I’m expecting come the spring period… I’m expecting supply to increase because we’ve had a low supply of housing over the last six months”.

“I expected [supply] to increase and when Supply increases house prices tend to go down”.

“The reason why I think house supply will increase is because the fixed rates are going to start to bite – a ‘fire sale'”.

“A lot of people are saying, a lot of agents are telling me people are hanging out to see whether or not this rhetoric which we’re hearing at the moment our house prices are going to go up before they sell people are hanging out for that period and if they don’t see that period, they’re going to have to sell and they’re going to sell into a big Supply market”.

“NAB are now talking… it looks as though rates will top out at 4.6%. That’s going to feed into that argument people just can’t afford to pay things back, regardless of whether you’re on fixed or variable rate”.

“I’m suggesting that even if interest rates don’t go up, there’s still a lack of affordability”.

“But if you put interest rates up two more times, like NAB is suggesting, then totally you’re going to get this position where affordability is non-existent”.

“Those people who currently have a home loan – and if they’re going from fixed to variable, which hasn’t actually started to catch up to us yet, it’s starting to catch up now – then those people are going to be in a lot of strife and they’re going to sell unfortunately”.

A lot will obviously depend on what the RBA does with interest rates. If it hikes a few more times, then we could see a tidal wave of forced selling.

The fact remains that there is still a lot of monetary tightening to come even if the RBA keeps rates on hold.

The recent rate hikes have yet to be fully passed on to variable mortgage holders.

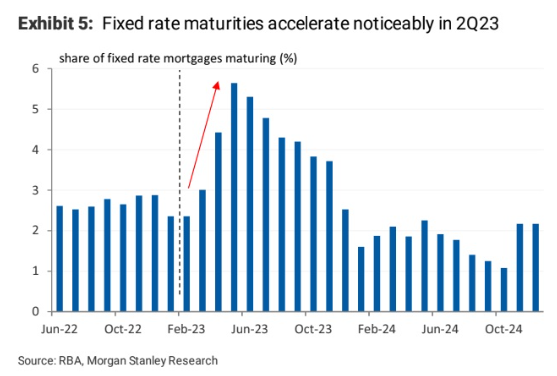

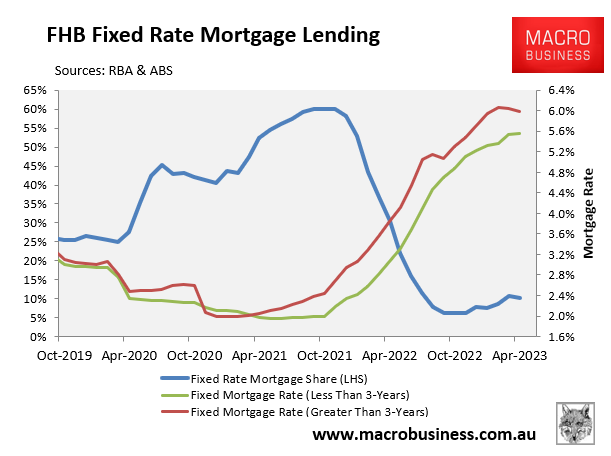

Worse, there are still around half a million fixed rate borrowers that will revert to variable this year:

These borrowers will suddenly jump from rates of around 2% to rates approaching 7% – or worse if the RBA keeps hiking.

Many of these fixed rate borrowers were first home buyers that borrowed near their maximum capacity over the pandemic and won’t be able to meet their new repayment schedules.

This house price rebound has been highly unusual given it has occurred alongside falling sales volumes and rising mortgage rates.

Surely at some point, the gravity of rising borrowing costs and falling borrowing capacity should reassert itself?

But who knows? The Australian housing market has a tendency to defy gravity and logic. This time might be no different.