Goldman finally catches up to MB.

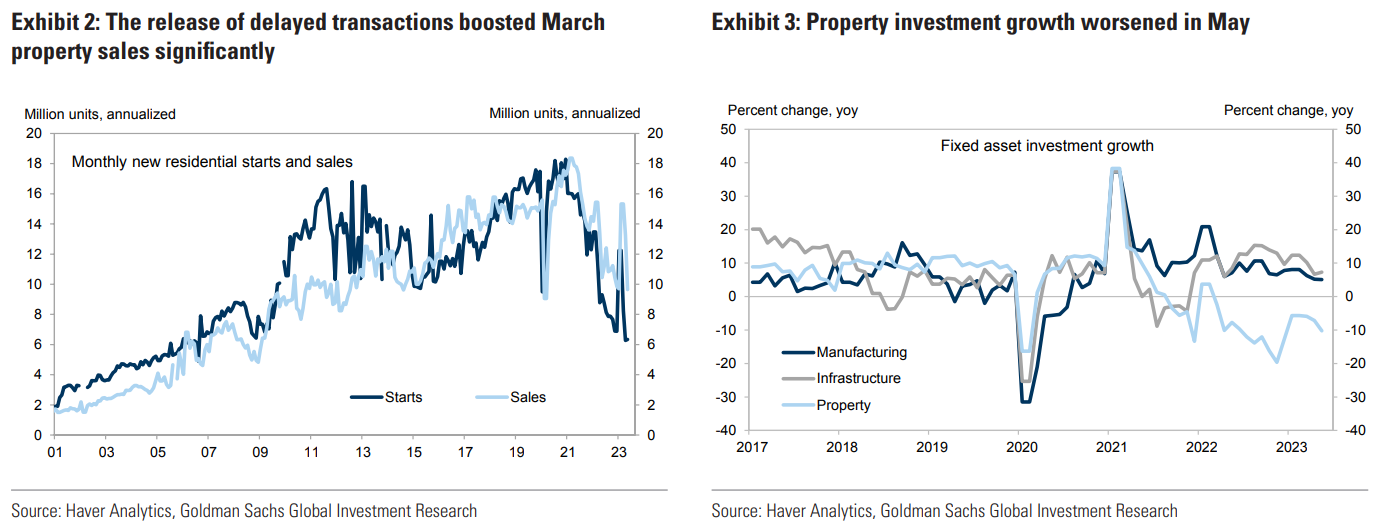

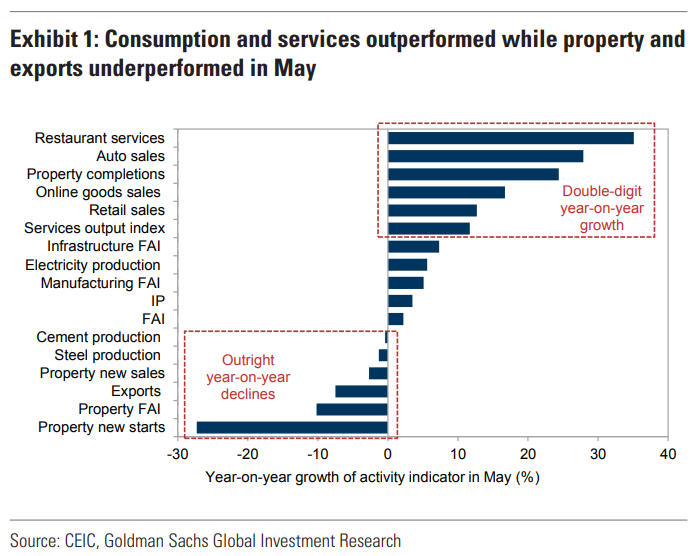

After a strong start in Q1, China’s post-reopening recovery appears to have fizzled out in Q2. Although contact-intensive services sectors continued to heal, May activity data show that the property market, the largest sector in the economy, weakened again. Property investment growth declined to -10% yoy and property-related products underperformed in detailed industrial production and retail sales data. With no “easy fix” on the horizon, the property market’s weakness and its negative impact on the rest of the economy is likely to persist.

The combination of deteriorating activity in the property market and a sharp decline in exports have triggered policy reactions. On June 13th, the PBOC cut OMO rate by 10bp. On June 16th, Premier Li Qiang held a State Council meeting calling for a basket of easing measures to be rolled out soon. We expect more policy easing for the remainder of 2023, including another RRR cut in Q3 and another 10bp OMO rate cut in Q4 on the monetary front.