By Gareth Aird, head of Australian economics at CBA:

Key Points:

- Employment rose by avery strong 75.9k in May following a 4k fall in April.

- The unemployment rate edged lower to 3.6% and the participation rate popped higher to 66.9% (a record high).

- An RBA 25bp rate increase in July now looks a 50/50 proposition (we previously favoured one final 25bp rate increase in August). We will wait for the monthly May CPI indicator, due for release 28 June, before finalising our July call.

A very strong set of labour force numbers that look inconsistent with other economic data

The monthly ABS labour force is colloquially known amongst financial market participants as the ‘labour force lottery’.

The survey nature of the release means that on any given month a set of numbers can print that defy logic and completely miss market expectations. The figures on Thursday very much fall into that category.

The headline numbers in the May labour force survey were unquestionably strong.

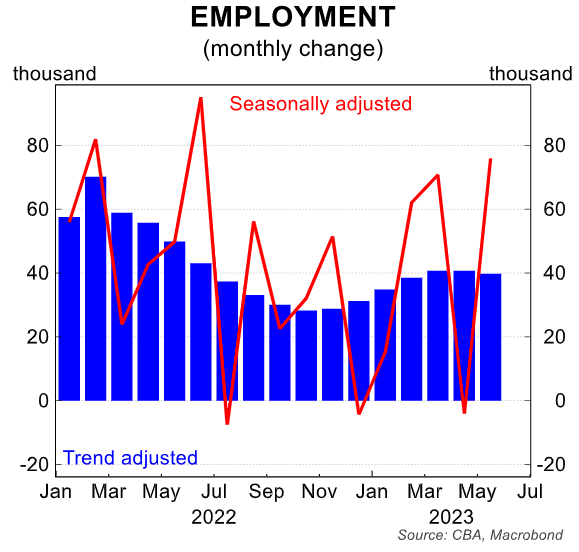

The increase in employment of 75.9k over the month was larger than the market median forecast of+17.5k; CBA a touch above consensus at +20k.

The bumper lift in jobs over May follows a decline in April of 4.0k.

The swings in the monthly seasonally adjusted change in employment have been very big over the past year. As the below chart shows, the trend change in employment is a lot more meaningful as it smooths out the large swings in the monthly seasonally adjusted change.

On that score, trend employment is running at ~40k a month. This is broadly the number of jobs required each month to keep the unemployment flat on an unchanged participation rate.

So the trend unemployment rate has essentially tracked sideways at ~3.5% over most of the past year.

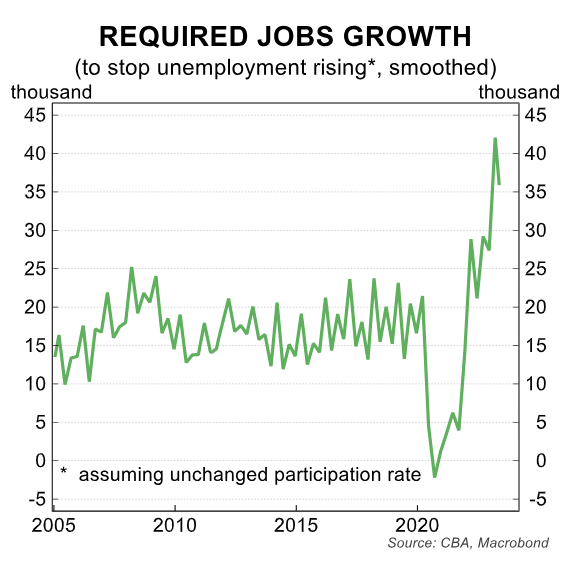

The number of jobs required to keep the unemployment rate flat on an unchanged participation rate has surged due to record high net overseas migration.

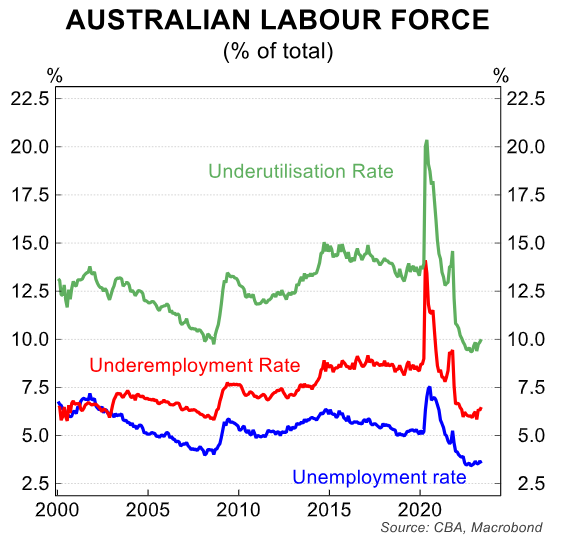

Back to the detail. The big increase in the headline change in employment was enough to drop the unemployment rate from 3.7% to 3.6% despite a 0.2ppt increase in the participation rate.

The participation rate now sits at a record high. The underemployment rate shot up by 0.3ppts to 6.4% -its highest level since February 2022.

As a result, the underutilisation rate, which is the broadest measure of labour market slack, lifted to 10.0%. It has increased by 0.6ppts since November 2022.

The message we take from the data is the labour market is loosening. But not via the traditional mechanism of an increase in the unemployment rate. Rather it is loosening via more workers looking for extra hours.

In time the unemployment rate will lift given below-trend economic growth. But it is simply just taking more time than would be expected given the slowdown in the economy.

On that score the labour force survey sits at odds with other important economic data.

The economy went backwards on a per-capita basis in Q1 23. And the early indicators of economy activity in the June quarter suggest further weakness over the current quarter.

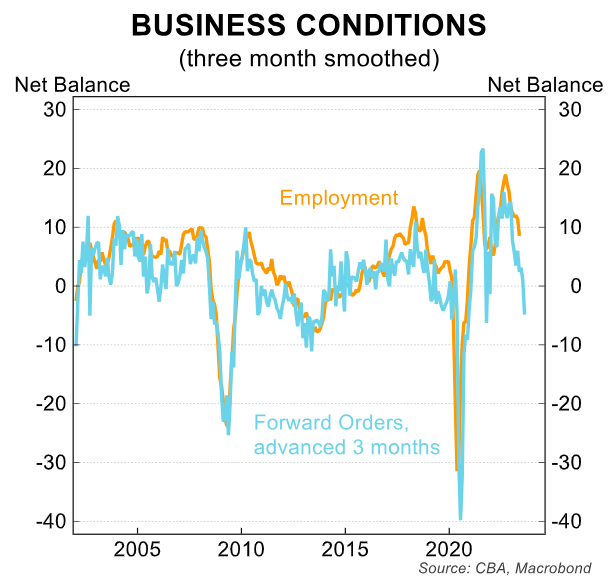

Forward orders, for example, in the May NAB Business survey were a shocker. Forward orders declined 6pts to -4 index points. Forward orders have historically had a strong leading relationship with employment growth.

The RBA meeting in July is clearly ‘live’ and the labour force survey today sees us put the odds of a 25bp increase in the cash rate at 50%.

The RBA is aware of the lag between slowing spend and the impact it has on the unemployment rate. Initially firms will keep workers on the books as demand slows. This weighs on measured output per hour worked.

Output (i.e. production) slows faster than the demand for inputs (i.e. labour). So productivity remains weak and unit labour costs stay elevated for a period of time.

But this dynamic does not last indefinitely. Once demand has slowed for a sufficient period of time some firms will respond by decreasing the hours they require their staff to work.

A reduction in headcount also occurs. This is expected to happen in the discretionary parts of the economy where spending is forecast to contract.

These outcomes are being engineered by restrictive monetary policy in order to drop the rate of inflation.

That all said, patience within the RBA Board for a more material loosening in the labour market is likely to be wearing thin given they recently ramped up their concerns around the outlook for higher wages growth and more persistent services inflation.

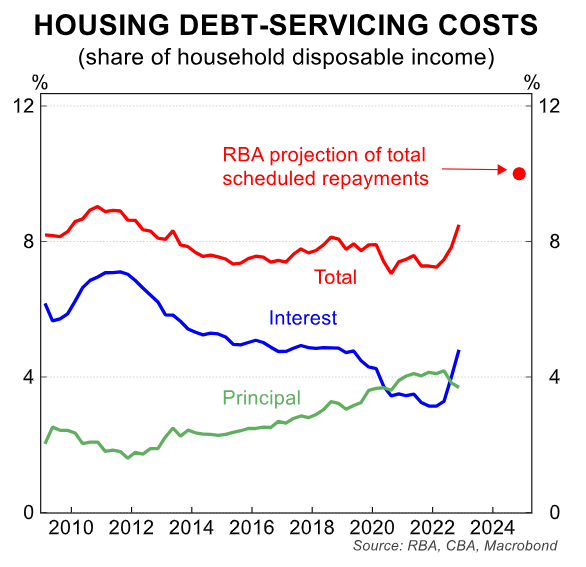

Only around half of the RBA’s already delivered 400bps of policy tightening has hit the household sector. So there is plenty more tightening built into the system.

But the Board might feel the policy response of least regret at this stage is to pull the rate hike trigger again in July.

The monthly May CPI indicator will be the key release before the July Board meeting. We will firm up our call for the JulyBoard meeting after that prints (28/6).