The Council of Financial Regulators last week confirmed that it would not lower APRA’s 3% mortgage serviceability buffer.

The 3% mortgage buffer is “designed to reinforce the stability of the financial system… ensuring the financial system remains safe, and that banks are lending to borrowers who can afford the level of debt they are taking on – both today and into the future”.

When Australian mortgage rates were at record lows and home values were rising at an unprecedented rate, the buffer was increased from 2.5% to 3.0% in late 2021.

Since then, the Reserve Bank of Australia (RBA) has raised the official cash rate by 4.0%, which has pushed up mortgage rates by similar amounts.

Currently, record numbers of borrowers are switching from ultra-low fixed mortgage rates of roughly 2% to variable rates reaching 7%.

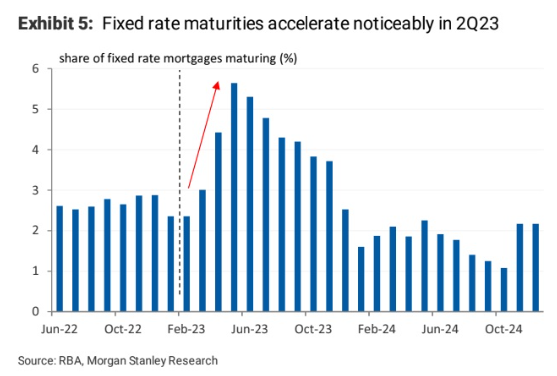

According to the RBA, 880,000 fixed-rate mortgages will expire this calendar year, with the majority of them resetting in the second half:

First home buyers are most impacted, given more than half took out fixed rates mortgages over the pandemic (versus 40% across the overall market):

These fixed-rate borrowers were assessed at mortgage rates ranging from 4.5% to 5% (i.e. 2% fixed rate plus a 2.5% or 3% buffer).

If they want to refinance, they will now be assessed at mortgage rates close to 10% (i.e., up to 7% variable rate plus a 3% buffer).

Most borrowers will be unable to fulfil these serviceability requirements.

As a result, many borrowers have/will become “mortgage prisoners,” unable to refinance and paying uncompetitive rates with their present lenders.

In last week’s interview with Sky News’ Ross Greenwood, I explained why APRA’s 3% mortgage buffer should be removed for those seeking to refinance.

My reasoning was as follows:

- These individuals are already ‘in the market’ and were assessed for serviceability when they took out their loans.

- Trapping them with their current lenders at uncompetitive interest rates is potentially harmful for financial stability since it could lead to additional forced sales.

- Creating ‘mortgage prisoners’ is also detrimental to competition, since lenders would have no incentive to offer a better rate if they know their borrower will be unable to leave.

- Forcing first-time home buyers out of their homes to bear the interest rate increase is inequitable.

In short, keeping the 3% mortgage serviceability buffer on mortgage refinances is illogical, unfair, detrimental to financial stability, and detrimental to competition.

Thankfully, the CBA has chosen to override APRA’s 3% buffer for mortgage refinances. CBA will instead allow only a 1% buffer provided:

- The application fails servicing using the standard 3% interest rate buffer.

- The refinanced loan(s) are structured as a 30 year loan term with P&I repayments.

- The loan(s) being refinanced have been open for a minimum of 12 months.

- The LVR is ≤ 80%.

- Loans which will require LMI or an LDP as part of the refinance will not be accepted.

- There are no delinquencies over the most recent 12 months (or for the full time the liability has been open if less than 12 months).

- There is no additional lending/top up/cash out for any purpose outside the refinancing of existing home loan(s).

- The loan involves personal applicants only, with a maximum of 2 applicants.

- Simple Liability Verification processes are not used.

- Alternate Servicing scenarios are not used.

Given CBA is Australia’s largest bank, I expect other lenders to follow suit.

If you are looking to save thousands of dollars in mortgage repayments, try the MB Compare n Save mortgage comparison tool. It takes less than a minute. And if you choose to refinance, Compare n Save will handle the process.