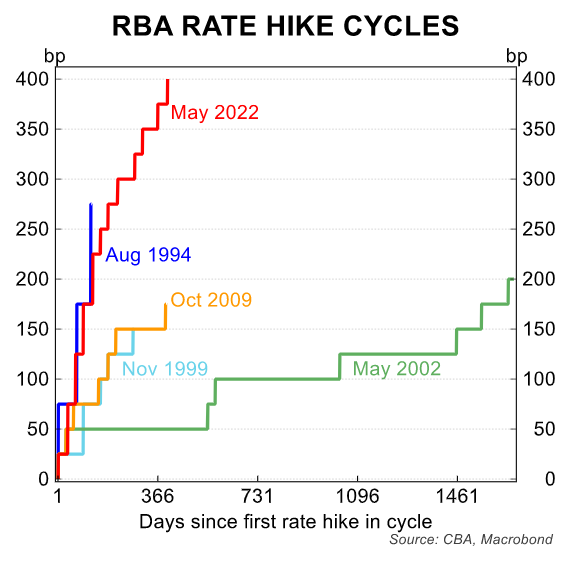

This week’s 0.25% interest rate hike from the Reserve Bank of Australia (RBA) feels like it could have been the last straw for many Australian mortgage holders.

After the fastest increase in interest rates in history, variable mortgage repayments have risen by around 50%, adding at least $1,200 a month in repayments to a typical $600,000 mortgage.

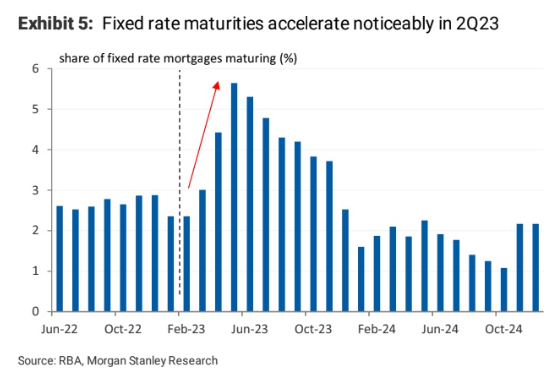

The situation will only worsen from here, with hundreds of thousands of cheap fixed rate mortgages scheduled to roll off over the remainder of the year, which will see mortgage rates more than double for these borrowers:

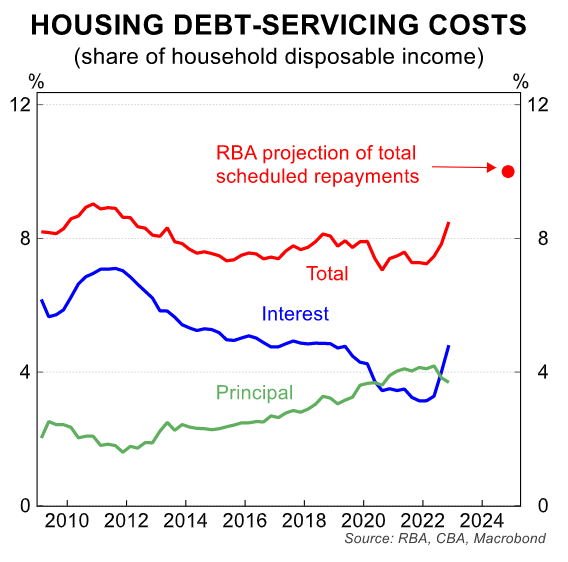

By next year, the share of household income devoted to mortgage rates will hit an all-time high, dwarfing the Global Financial Crisis peak:

Following the RBA’s latest rate hike, SQM Research managing director Louis Christopher stated that he now expects “distressed activity to rise based on a new round of forced and panicky selling starting sometime the second half of this year”.

In turn, he told market participants “to be prepared for a new round of housing price falls starting in the second half of 2023”.

Coolabah Capital’s Chris Joye also said that top real estate agent Alexander Phillips called him claiming the “market is turning”, with “nervous vendors” inundating him with requests to quickly list their properties before prices fall:

Phillips also reportedly believes the last quarter’s house price gains will be wiped out by the end of the year.

Finally, prominent Sydney agent and auctioneer, Tom Panos, believes the RBA has pushed rates to a “tipping point” that will push the housing market over the edge.

“I think this is the tipping point. I think this is the bit where mum’s and dad’s today are going to sit home with a calculator and say ‘you know what? How are we going to do this? We can’t do this anymore'”, Panos said via video.

“You know what’s going to happen? You are going to start seeing the property market affected”.

“At the moment we’ve got this artificial housing market that’s going gangbusters. Not because of any economic reasons. Purely because of demand and supply”.

“Wait until you see the stock that comes on the market. Let’s see how the demand and supply curve works then”.

“I’m calling this the tipping point”, Panos concluded.

Of course, we will only know in hindsight whether this is indeed the ‘tipping point’.

However, this price rebound has been highly unusual since it has occurred amid falling sales volumes and rising interest rates.

At some point, the gravity of higher borrowing costs and reduced borrowing capacity should logically reassert itself.