Westpac has the note.

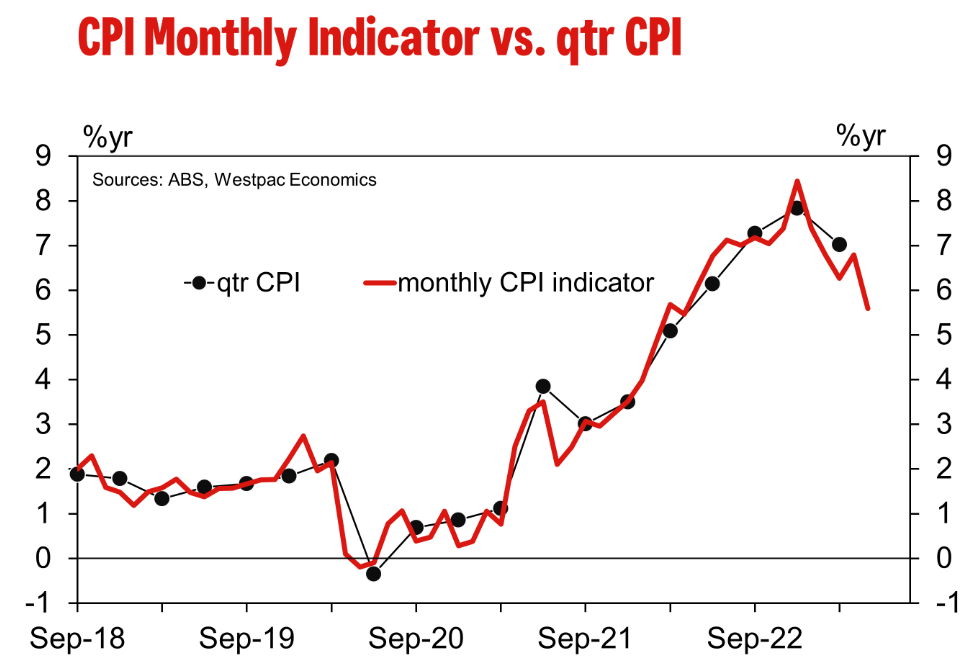

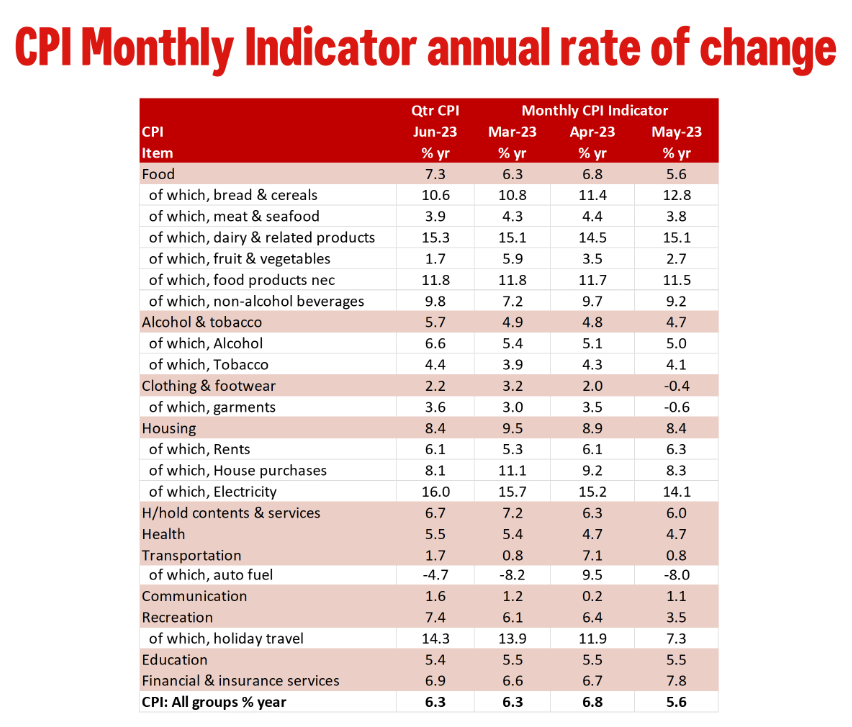

The Monthly CPI Indicator rose 5.6% in the year to May compared to Westpac’s and the market’s 6.1%yr forecast. With May’s weakness following April’s strength, risks to our Q2 Headline CPI forecast of 1.1%qtr/6.3%yr are now more evenly balanced.

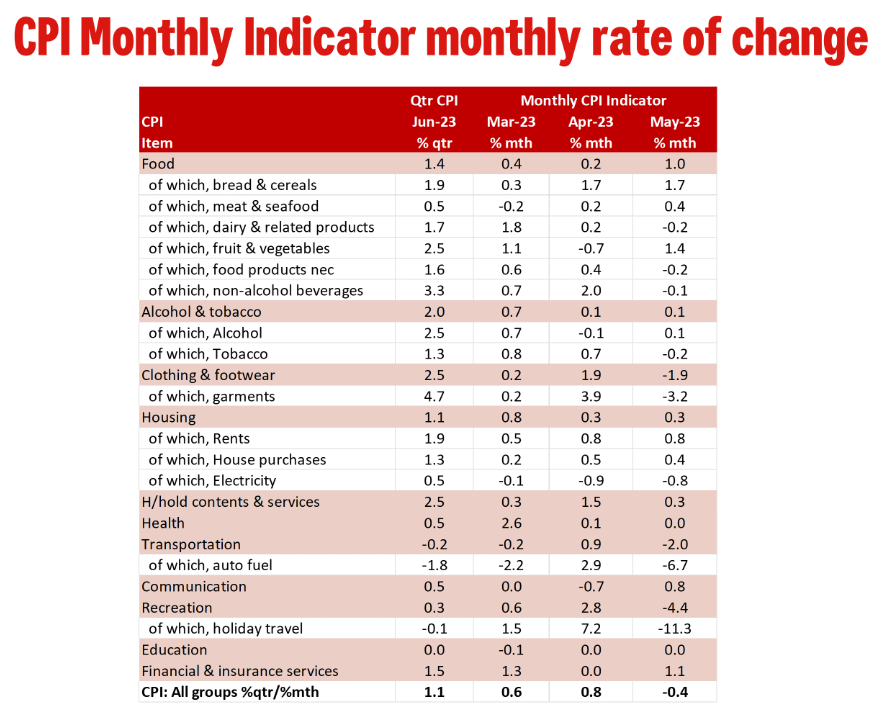

In May, the headline index declined by 0.4% compared to our forecast for a 0.1% gain; we assume the market median would have matched our own given the same 6.1%yr forecast.

This represents a partial unwind of April’s 0.8% gain, bringing the annual pace down from 6.8%yr to 5.6%yr, well off the December peak of 8.4%yr.

It is worth highlighting the ABS’ comment that “CPI inflation is often impacted by items with volatile price changes like automotive fuel, fruit and vegetables, and holiday travel.”

In essence, with the CPI Indicator being a monthly series, it is subject to a significant amount of seasonality, some of which is generated by having some elements surveyed only once a quarter or even once a year.

With May being the second month in the quarter, we received an update on more services components that are only measured once a quarter, including restaurant and takeaway meals; hairdressing and other household services; vehicle services; and some recreational services.

The positive drivers highlighted by the ABS were largely anticipated, with a lift in housing (+0.4% vs. Westpac’s +0.3%); food and non-alcoholic beverages (+1.0% vs. Westpac’s +0.8%) and household contents and services (+0.3% vs. Westpac’s +0.4%) all reported as significant contributors.

It is interesting to note the underlying strength of services components within these categories.

For example, the lift in housing was centred on a 0.8% increase in rents, raising the annual rate from 6.1%yr to 6.3%yr while new dwelling purchases moderated from 9.2%yr to 8.3%yr.

The ABS also notes on food and non-alcoholic beverages, there was up-tick in meals out and takeaway foods from 7.3%yr to 7.7%yr as “higher costs of ingredients, rents, utilities, and wages were passed on”.

Other services categories also had a stronger-than-expected rise but these were modest in terms of their contribution to the Monthly Indicator, including a lift in communication services (+0.8% vs. Westpac’s +0.2%), financial and insurance services (+1.1% vs. Westpac’s +0.1%) and other recreational services (+1.7%).

Offsetting the above was a moderation in automotive fuel and holiday travel. Since we have good data on weekly petrol prices the decline in fuel prices was well anticipated, having printed broadly in line with Westpac’s forecast and left the transport category down 1.9% in the month (vs. Westpac’s –2.0%).

From our perspective, the key downside surprise was a stronger-than-expected decline in holiday travel and accommodation prices, down 11.3% in the month (–15.5% for domestic; –4.7% for international), well below our forecast for a 4.9% fall.

This more than reversed April’s robust gain of 7.2% and now leaves this category at an annual rate of 7.3%yr, down from April’s 11.9%yr.

This decline in holiday travel and accommodation prices was worth about –0.34ppts, explaining a large part of the downside surprise relative to our forecast.

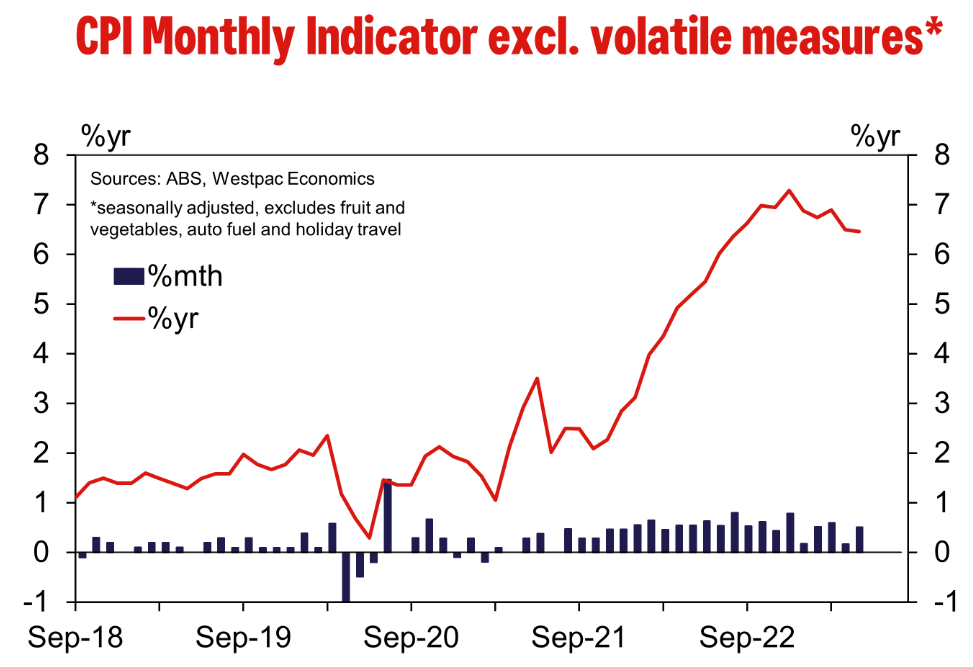

Indeed, the Monthly CPI Indicator excluding volatile items (fruit and vegetables, automotive fuel and holiday travel) was reported to have been virtually unchanged in May, holding at 6.5%yr in seasonally adjusted terms and slipping to 6.4%yr in original terms.

The seasonally adjusted version of this indicator is still well below its peak of 7.3%yr in December last year, though its monthly pace has picked-up from 0.2% in April to 0.5% in May, similar to what was seen in prior months (0.5% in February; 0.6% in March).

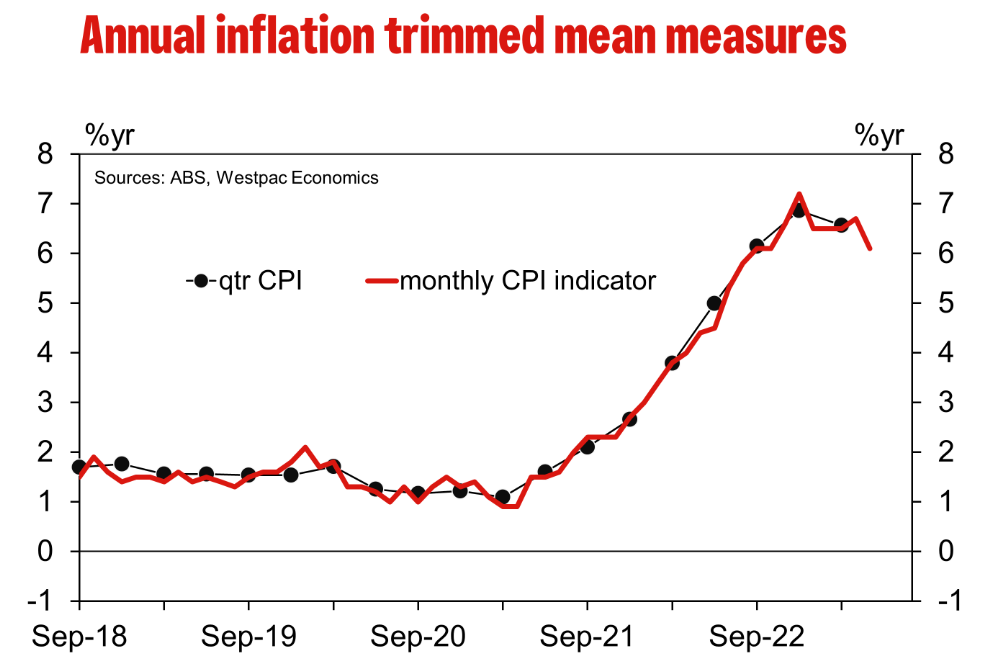

The annual trimmed mean measure, which was reinstated in April following some adjustments to be more consistent with the quarterly series, was reported to have eased from 6.7%yr in April to 6.1%yr in May.

The upside risk associated with our Q2 Headline CPI forecast of 1.1%qtr/6.3%yr following April’s strength now looks to have eased following May’s weakness. Whereas for underlying inflation, the May update now presents downside risk to our Q2 Trimmed Mean CPI forecast of 1.2%qtr/6.1%yr.

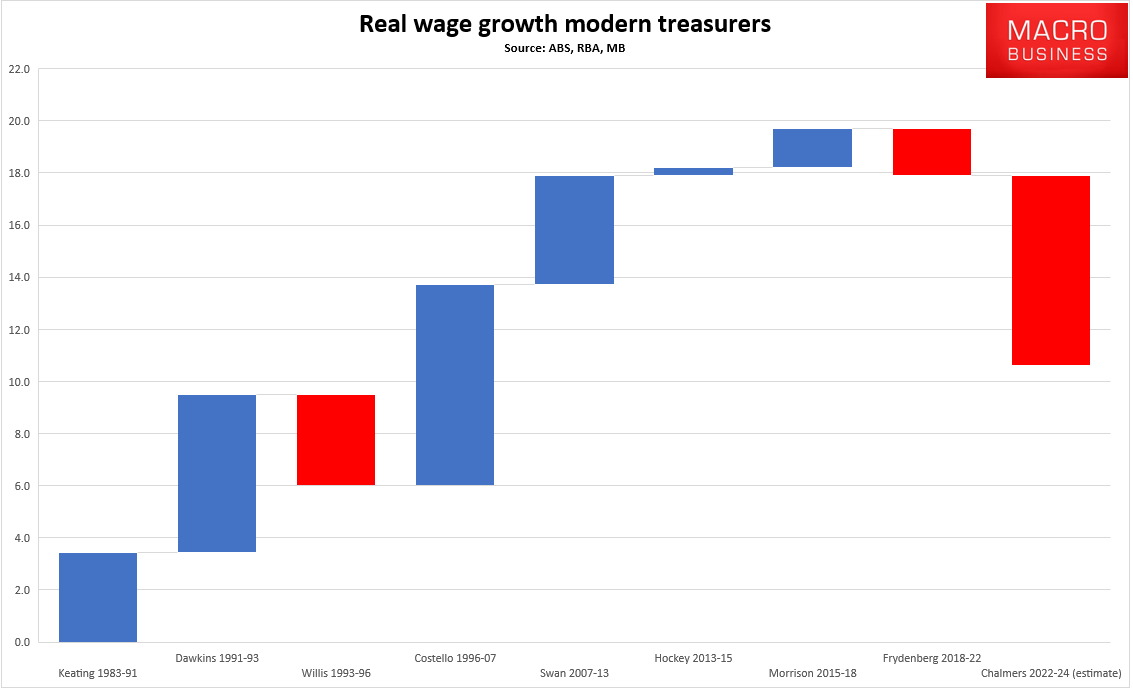

In short, most of the stimulus and supply chain inflation of the pandemic and Ukraine War is gone.

Agriculture, supply chain and packaging costs have crashed globally. It is now processing and retailing costs that are driving food price gains. They are driven by Albo’s energy shock.

Housing construction costs are falling, but inflation in the segment has been passed to rising rents via Albo’s mass immigration shock.

Take Alboflation out of food and rents and the month-on-month Aussie CPI craters.

Meanwhile, the Albo’s mass immigration also crushes wages.

Thus real incomes crater:

If Albo’s oft-referenced working-class mother were here today, she would be disgusted.