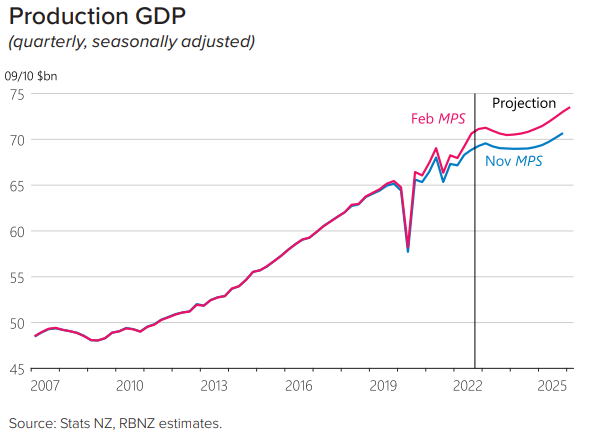

The Reserve Bank of New Zealand’s February Monetary Policy Statement explicitly forecast a recession, predicting a “peak-to-trough decline in the level of GDP over 2023… [of] about 1%” due to “higher interest rates, lower house prices, and a weaker labour market”:

However, it did not anticipate a recession until later in the year:

The December quarter national accounts were then released and showed that the economy was already halfway into recession, with GDP contracting 0.6% over the quarter.

That was a far worse result than anticipated by economists and drastically lower than the 0.7% increase in quarterly GDP forecast by the Reserve Bank.

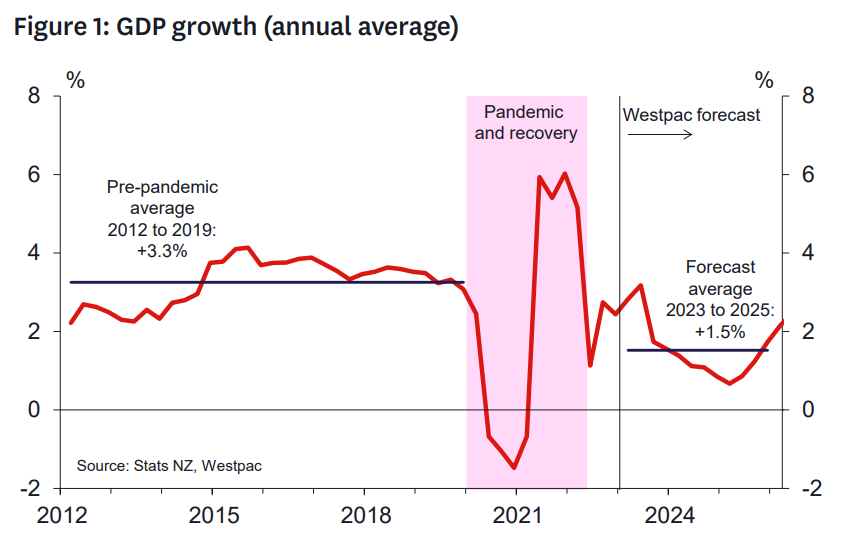

Westpac’s latest economic overview, released this week, estimated that “economic output fell by 0.8% over the December and March quarters combined”, thereby fitting the definition of a ‘technical recession’ where GDP falls for two consecutive quarters.

Westpac also predicted that “the rapid economic growth we saw in the wake of the Covid-lockdowns will now give way to an extended period of subdued growth”:

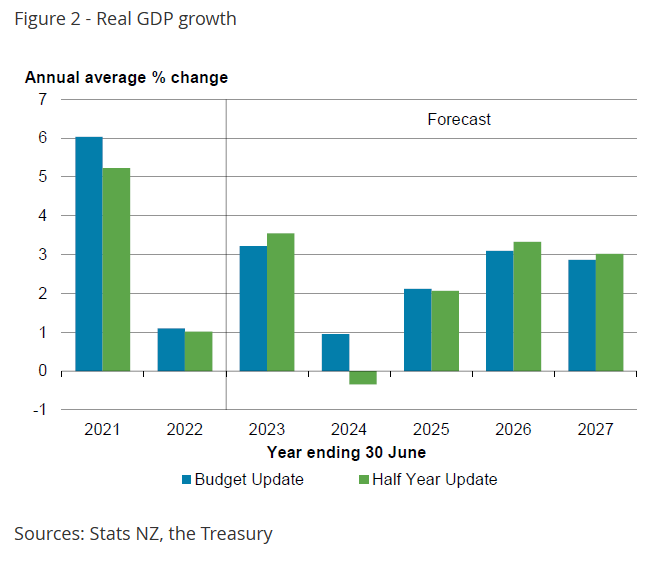

The New Zealand Treasury on Thursday released the 2023 Budget, which forecast that New Zealand would avoid recession to grow by 1.0% over 2024:

Ongoing strength in tourism and the unexpected boom in net overseas migration will keep the country out of recession, according to the updated forecasts.

However, unemployment will rise to 5.3% in late-2024 (from 3.4% currently), before falling back to 4.8% in the end of the forecast period.

Moreover, amid strong projected population growth of 1.4%, real GDP per capita will contract by 0.4% in 2024, according to the Budget.

Therefore, while New Zealand may or may not experience a technical recession, it will feel like one given the projected 1.9% rise in unemployment and the decline in per capita output.

Similar per capita recessions are also forecast for Australia and Canada.