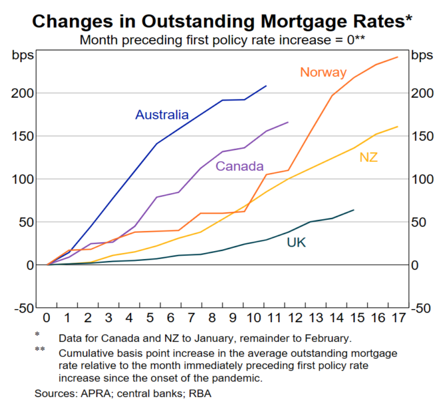

The Reserve Bank of Australia (RBA) recently published the below chart to demonstrate that Australia’s mortgage rate increase has been more pronounced than almost any other developed nation:

Despite the RBA raising official interest rates less than most other central banks, typical mortgage rates in Australia have increased more quickly:

The Reserve Bank of New Zealand has boosted its cash rate by 5% over this cycle, easily outpacing the 3.75% increase in Australia’s official cash rate.

However, compared to New Zealand, where average mortgage rates have increased by about 160 basis points, Australia’s rates have increased by about 210.

According to RBA governor Phil Lowe, “the predominance of variable-rate mortgages” in Australia “means this is a more powerful transmission mechanism of monetary policy than in many other countries” and that is why mortgage rates have increased excessively here.

In New Zealand, the vast majority of mortgages have fixed rates.

Whereas the US is not even listed on the above chart because mortgage rates there are normally set for the whole 30-year loan term.

According to The SMH’s Money contributor, Nicole Pedersen-McKinnon, Australian mortgage holders are now hurting more than borrowers did when interest rates hit 17% in 1989-90.

Pedersen-McKinnon explains that the typical mortgage size averaged $67,350 when rates hit 17% and the average salary was $26,437, according to ABS data.

That’s a loan-to-take-home multiple of 2.5 times.

Now, the average mortgage is now worth $586,366 and the average wage is $93,907.

Thus, the loan-to-take-home multiple has ballooned to 6.2 times.

“At an interest rate of 17% in 1989/90, the mortgage consumed 44%”, Pedersen-McKinnon says.

But at the current discounted rate of 6.16%, “the mortgage cut of your money is 49%”.

“Housing stress is defined as when the roof over your head costs more than one-third of your salary. The average Aussie is well past that”, Pedersen-McKinnon warns.

“Here we are with still-exorbitant house prices, virtually stagnant wages and suddenly, brutally higher interest rates. Making the mortgage was super tough in the later ’80s and early ’90s”.

“It is now equally tough, at best”, Pedersen-McKinnon concludes.

I’ll go one further. Today’s generation of mortgage holders has the worst of all worlds: high house prices relative to incomes, high rates, and the worst mortgage affordability on record.

The deposit required is also much higher reflecting the extreme price appreciation relative to wages.

Better stop eating those smashed avocado sandwiches, hey?