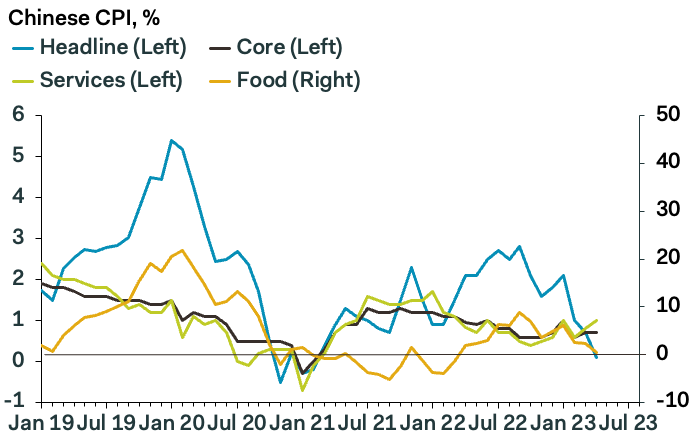

The widening gap between core goods and services prices is a product of the lopsided recovery. People are spending in restaurants, leisure services and tourism, after the ending of zero-Covid policy, but less so on goods. Domestic tourist numbers rebounded to almost 20% above 2019 levels during the five-day May Holiday at the start of the month. Travel prices accelerated 3.8pp to 9.1% y/y in April.

Core goods inflation slowed 0.7pp to zero in April. Excess production capacity has emerged in several sectors as a result of the fall in exports since H2 2022, caveated by the bump in March/April, which likely represents manufacturers catching up with back orders. Global demand is likely to remain weak. Domestic retail sales of goods are recovering much more slowly than for services.

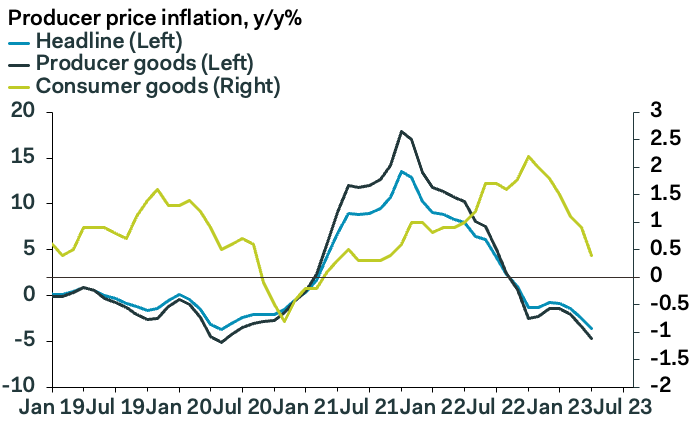

Producer prices continue to fall, after capacity build up

The decline in Chinese producer prices steepened 1.1pp to 3.6% in April, the sharpest fall since May 2020. Base effects play a role, especially in falling year-over-year commodity prices. But the fundamental story is a gap between supply and demand, thanks to China’s build up of productive capacity through strong investment over the last several years, while demand remains soft, both at home and abroad. Industrial capacity utilisation fell 1.4pp from Q4 to 74.3% in Q1.

…We expect producer prices to continue to fall this year, as a result of restrained growth policy support, symbolised by the relatively conservative “about 5%” GDP growth target. Continued strong manufacturing investment will expand supply, while the domestic demand recovery is measured, and exports should fall off in H2, as global demand weakens. We stick by our view that China is likely to export disinflation, not inflation, to the world this year.

That is not painting the picture of a strong economy. And why would it? Without external demand and internal property demand, China is a broken developed economy. This is ex-growth China.

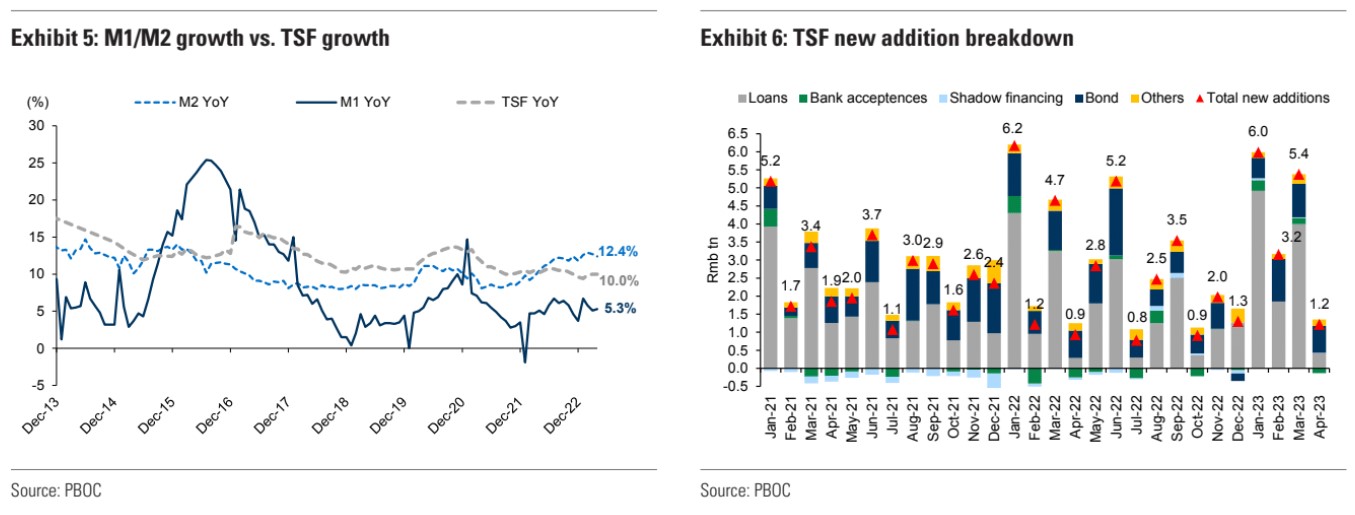

Moreover, it is getting worse. Goldman wraps New Yuan Loans for April which came in at roughly half expectations:

Advertisement

April 2023 TSF data was released on May 11, with new TSF and loans of Rmb1.2tn/443bn vs. Rmb 933bn/362bn in April 2022. TSF/loan balance growth came in at 10.0%/11.7% yoy in April 2023 vs. 10.2%/10.7% in April 2022. We summarize the data as 1) gov. credit demand remains strong, on more gov. bonds and mid/long term corporate loans; 2) both retail deposits (Rmb -1.2tn) and loans (Rmb -241bn)declined. That said, we expect this normalizing credit growth post1Q23 credit impulse, due to the increasing constraints of bank credit supply on weakening capital accumulation.

Here is my key chart which can hardly count as a credit recovery at all with broad credit stalled at 10%:

Advertisement

As well, household loans, mostly mortgages, contracted by 241.1 billion yuan in April, compared with 1.24 trillion yuan in March, while corporate loans slid to 683.9 billion yuan last month from 2.7 trillion yuan in March.

All gloomy stuff.

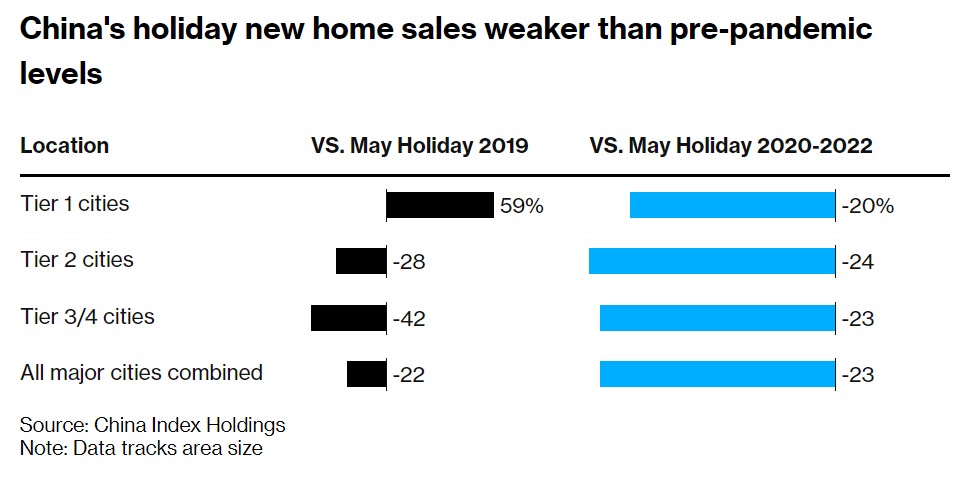

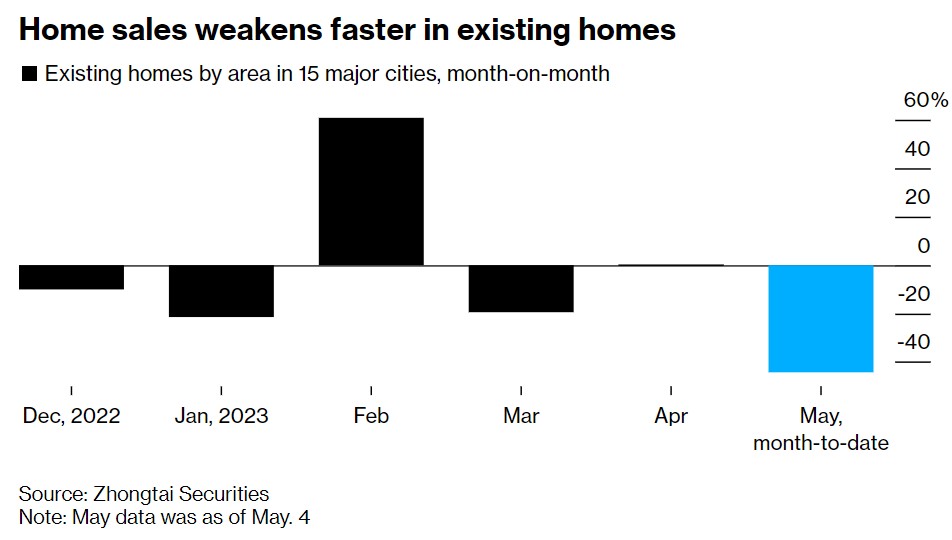

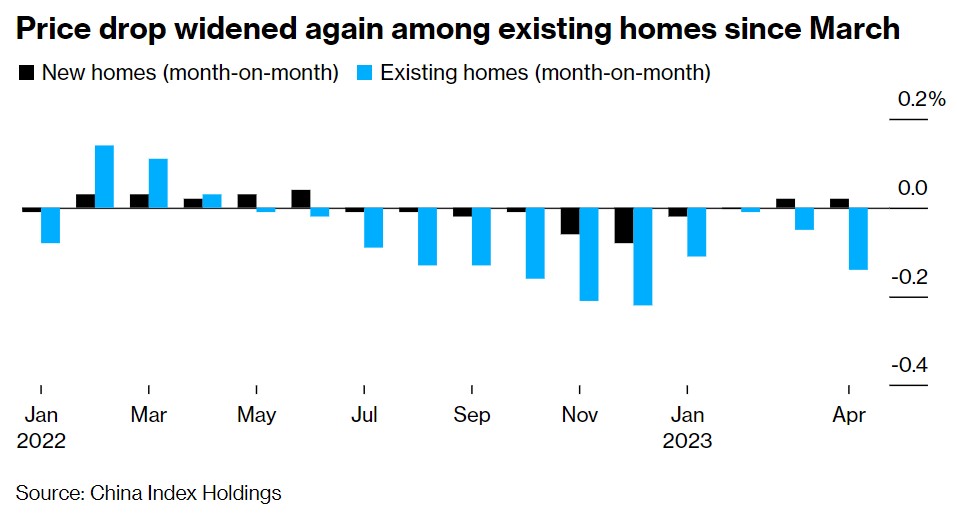

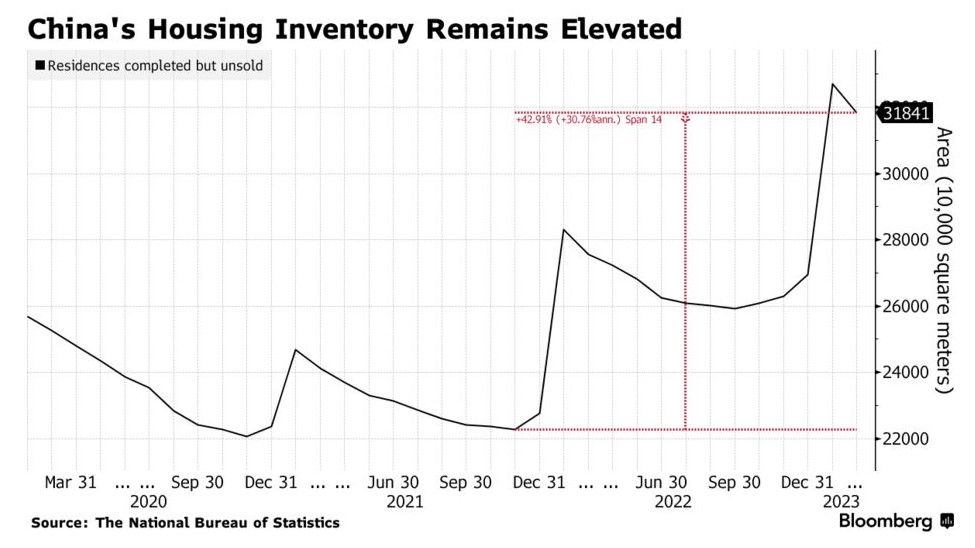

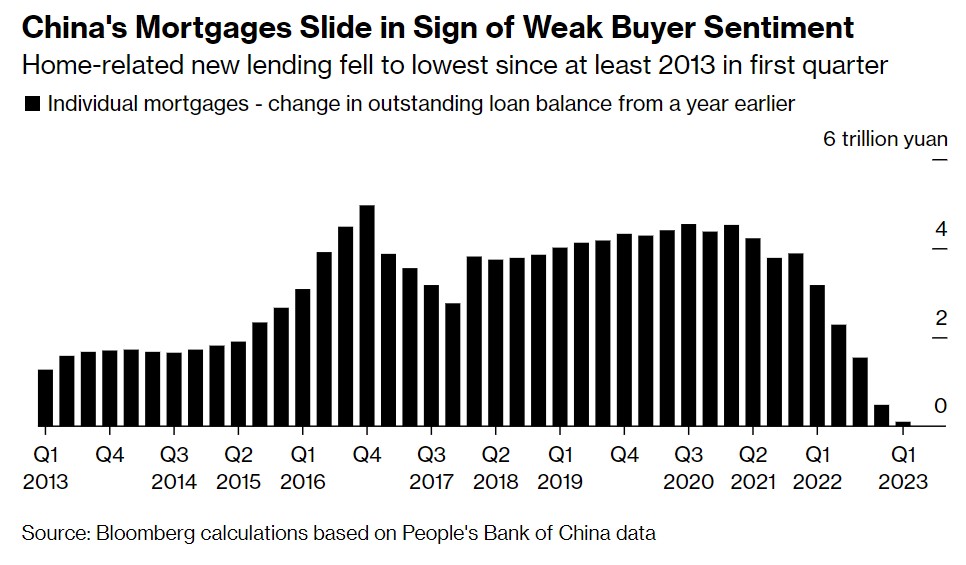

It is no wonder that the housing recovery is stalling, More charts. Sales suck:

Advertisement

Prices volatile:

Inventory LOL:

Advertisement

Mortgages liquidity trap:

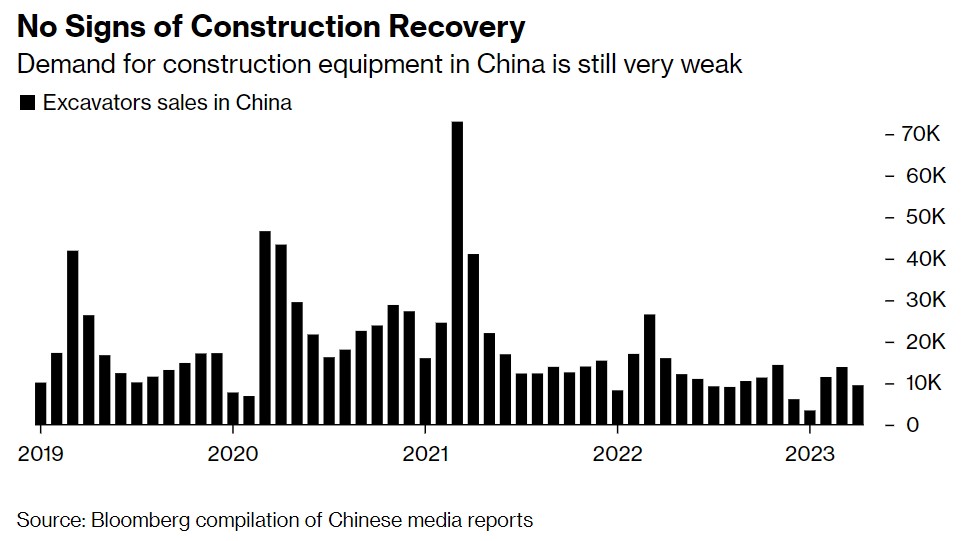

Construction caput:

No wonder iron ore is so buggered. Shanghai rebar futures fell again yesterday though TSI held on:

Advertisement

But Dalian futures plunged late in the day and closed at new lows overnight:

Advertisement

Unless China stimulates quickly, it looks like more iron ore falls dead ahead. Even then I would sell the rip.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.