Westpac with the note.

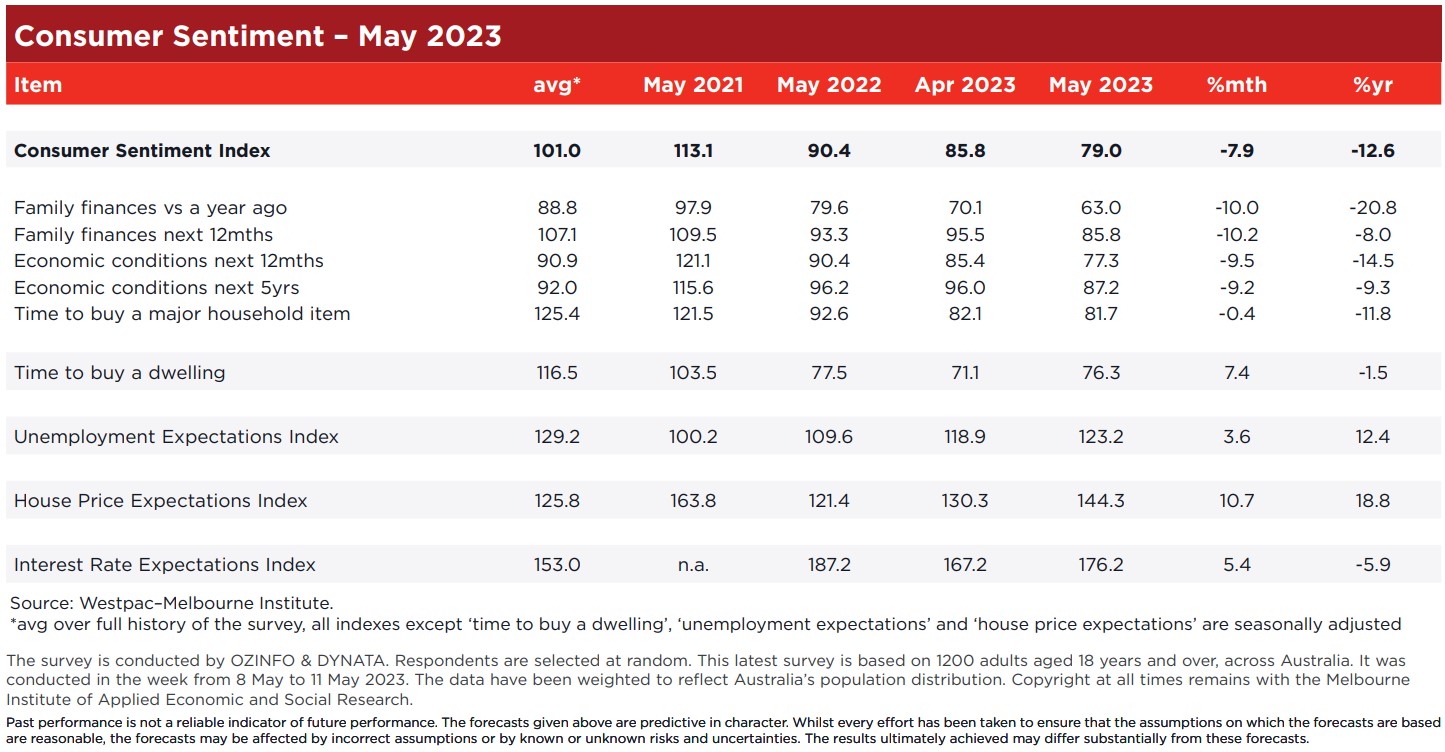

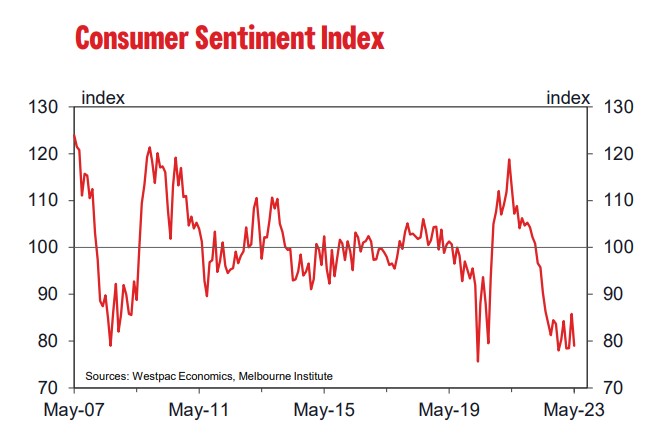

The Westpac Melbourne Institute Consumer Sentiment Index fell by 7.9%, from 85.8 in April to 79.0 in May.

The Index has fallen back to just above the dismal levels seen back in March, which recorded the lowest monthly read since the COVID outbreak in 2020 and, before that, since the deep recession of the early 1990s.

The two key developments over the last month have been the surprise decision by the Reserve Bank Board to lift the cash rate by a further 0.25% in May and the Federal Budget.

The survey is usually conducted in the week of the Reserve Bank Board meeting but was delayed a week to gauge the sentiment impact of the Federal Budget. While this means we do not have ‘before’ and ‘after’ reads on the surprise RBA decision, we do have a clear ‘before’ and ‘after’ picture on the Budget.

Sentiment amongst those surveyed before the Budget announcement showed an index read of 81.3 (down 5.3% compared to April). Sentiment amongst those surveyed after the announcement came in at 75.3, down an additional 7.4%. A strict interpretation would attribute about 60% of the May fall to the Federal budget and the remaining 40% to the interest rate decision and other factors.

That is probably being too harsh on the Budget. Sentiment typically dips between pre- and post-Budget surveys. Some consumers may also have had unrealistic expectations going into

Budget 2023 – especially around the scope to deliver cost-ofliving relief without adding to the task of reining in high inflation.

The sub-group detail highlights both sides of this tension with big post-Budget sentiment declines for those most dependent on cost-of-living relief (low-income households, the unemployed and some renters) but also a big decline in the group that has most at stake around inflation – households with a mortgage.

More specific responses on the impact of the Budget on family finances show this year’s Budget is expected to deliver some relief.

Our survey included the standard question we have asked after every Budget since 2010 on the expected impact on finances over the next 12 months. For 2023, 15.5% of those surveyed after the Budget expected it to improve their finances and 27% expected to be worse off.

While self-assessed ‘Budget-losers’ outnumber ‘Budget-winners’ this is nearly always the case. Indeed, outside of the pandemic period (when generous fiscal measures were required), the average gap between optimists and pessimists has been over 25%. Viewed against history, the 2023 ‘gap’ of 11.5% is much less unfavourable than that of the previous Budget in October (28%) and is only bettered by one budget in the 2010-19 period – the 2018 Budget that announced a major series of income tax cuts and saw a ‘gap’ of just 9.1%.

This historical comparison, and the clear inflation-related limitations on policy suggest the Federal government should be satisfied with the consumer response to this year’s Budget.

Interest rates were again a key driver of the May survey. As noted, the RBA raised the official cash rate by a further 0.25% at its May meeting in the week before the survey. The move came as a major surprise to markets and most commentators, clearly stoking consumer fears of more increases to come.

Nearly 70% expect a further rise in variable mortgage rates over the next 12 months, with just over 40% expecting them to rise by 1ppt or more. This compares to 61% and 34% respectively following the RBA’s ‘on hold’ decision in April (albeit well down on November’s peak of 81.5% and 60%). Consumers are right to heed the RBA Governor’s explicit warning that “some further tightening of monetary policy may be required” but the extent of these fears seems excessive.

The sub-group detail shows bigger sentiment declines for those with low incomes (–15%), renters (–13%), mortgagors (–10%) and women (–10%). By state, sentiment posted notably sharper falls in WA (–23%) and Queensland (–13.3%). The bigger fall in confidence amongst renters than mortgagors came despite the strong interest rate theme and highlights the extent to which tight rental markets and surging rents are putting intense pressure on a group, that makes up around 30% of households.

All index components fell in the month, views on family finances and expectations for the economy showing a deeper plunge, with attitudes towards major household purchases more settled but at a very low level by historical standards.

Views on finances reversed all their April gains, the ‘finances compared to a year ago’ sub-index dropping 10% and the ‘finances, next 12 months’ sub-index down 10.2%, both moving back to their March lows. The ‘economy, next 12 months’ subindex dropped 9.5% and the ‘economy, next 5 years’ sub-index fell 9.2% – the latter moving back to the low seen in November.

The ‘time to buy a major household item’ sub-index dipped just 0.4%, but at 81.7 this reading is still amongst the weakest seen in the history of this measure going back to the mid-1970s.

Notably, it is weaker than any print during the deep recession of the early 1990s. While still modest, the improvement over the last two months may be a tentative early sign that the surge in goods prices that has weighed so heavily on buyer sentiment over the last year, may be starting to moderate.

On jobs, consumers remain relatively upbeat but are continuing to show a gradual loss of confidence. The Westpac-Melbourne Institute Unemployment Expectations Index increased 3.6% from 118.9 to 123.2 (recall that a higher index means more consumers expect unemployment to rise in the year ahead).

While the index is still comfortably below its long run average of 129, the 23.6% rise from its most recent low in September is consistent with a significant cooling in labour market conditions.

Housing-related sentiment posted a sharp lift in May, despite the weak picture on sentiment overall and clear ongoing concerns about interest rates.

The ‘time to buy a dwelling’ index lifted 7.3% in May, extending the 8.2% gain in April. Buyer sentiment is still only reversing the sharp 16% weakening through February-March. At 76.3, the index is back in the narrow 75-80 range that has prevailed since rates began rising in March last year. The level of the index in May is still 42% below the most recent peak in November 2020.

The standout result in this month’s survey is the House Price Expectations Index. This staged a remarkable 10.7% surge to 144.3, hitting the highest level since February last year. Recall that the ‘100’ level on the index marks the point where there are an equal number of respondents expecting house prices to rise and fall. At 144 optimists heavily outnumber pessimists (literally, by four to one). This optimism is despite widespread expectations of further interest rate rises.

Recent shifts in housing-related sentiment are ‘internally inconsistent’ – buyer sentiment, which is heavily affected by affordability, does not typically see sustained gains when house prices and interest rates are rising. While strong immigration is clearly influencing markets, this tension is likely to be resolved in the near term. A possible signal in this regard is the more restrained price expectations amongst women – up 5.1% compared to a 16.5% surge for men. Overall, the house price index for women is 8.5% lower than the index for men.

The Reserve Bank Board next meets on June 6. We expect it to leave rates on hold.

For the Board, the May Consumer Sentiment Survey is sending somewhat mixed messages.

On the one hand, consumer sentiment is back near the historic lows we have only really seen on a sustained basis in the deep recession of the early 1990s. The entrenched pessimism is clearly reflecting intense pressure on household disposable incomes resulting from high inflation and the sharp rise in interest rates. This signal is apparent in actual activity with a range of spending indicators now pointing to a sharp slowdown.

On the other hand, the survey continues to show resilience around labour market conditions and signs of renewed confidence in the housing market. Both were cited in theBoard’s surprise decision to raise rates in May.

We expect the Reserve Bank Board to pause again in June and await more information around inflation and the state of the economy. Our central view is that the weakness in the economy coupled with clear progress towards the Board’s inflation target will see the current level of the cash rate hold as the peak, but the risks remain evenly balanced.