TSLombard with the stinging truth for commodities.

A significant monetary injection has failed to trigger any meaningful increase in assets prices, inflation or output. Why did money not flow to the real economy? Simply put, precautionary savings have surged, and negative wealth effects – particularly in property – have scarred households, businesses and local governments. A balance-sheet recession has been under way for some time. Politburo and PBoC statements indicate policy will remain accommodative but suggest no major increase in monetary stimulus for now. Confidence is key; and based on our below-consensus forecast for H2/23 and the fact that pent-up demand is showing some weakness in Q2 (earlier than we expected), we think the velocity of money is likely to improve only marginally, with limited pass-through to the real economy in 2023.

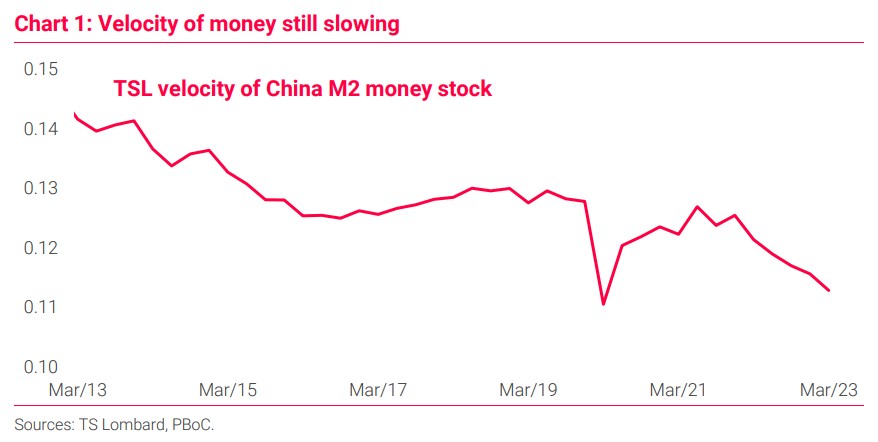

The PBoC is still pushing on a string. For some time now, we have noted that the credit transmission channel in China is impaired. This is largely a structural issue following property overbuilding and household-debt saturation; and it also reflects a change in the Party stimulus reaction function and a tolerance for slower growth. Cyclically, the combined Covid and property shock clearly lowered the velocity of money and the multiplier effect of credit stimulus (Chart 1).