The recent DXY pop took a breather last night:

AUD repaired some damage:

Commodities are not well:

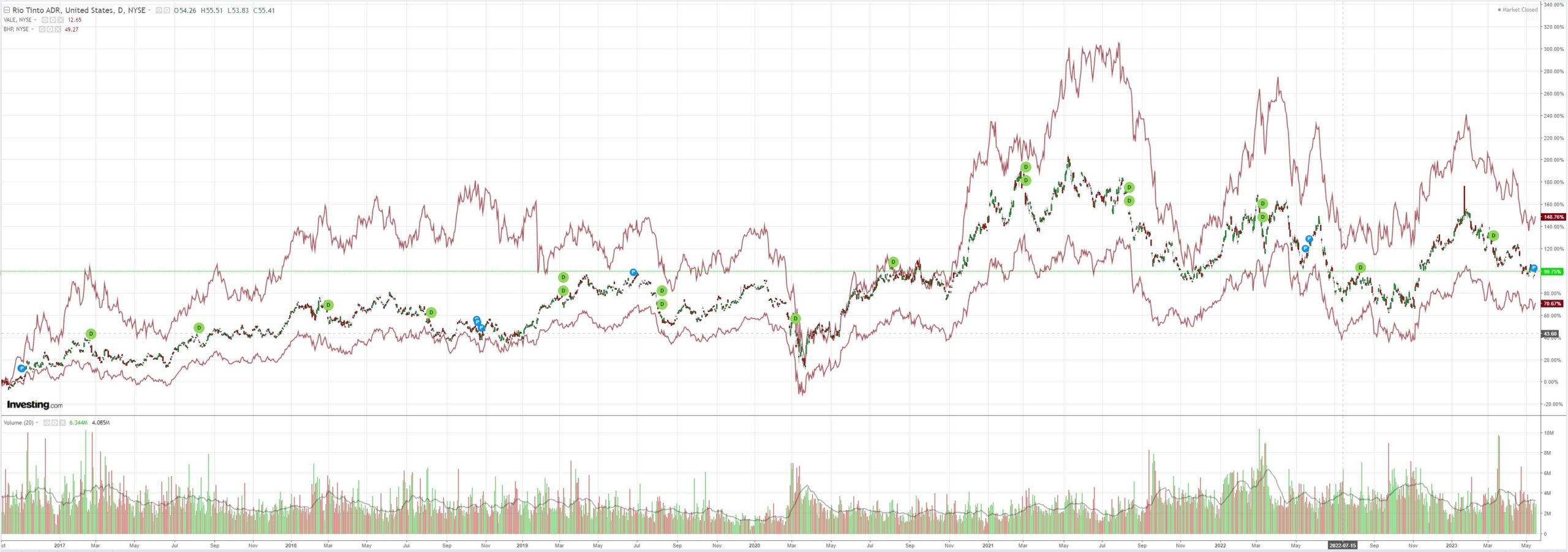

Miners offered pennies in front of the steamroller:

EM stocks are slowly drowning:

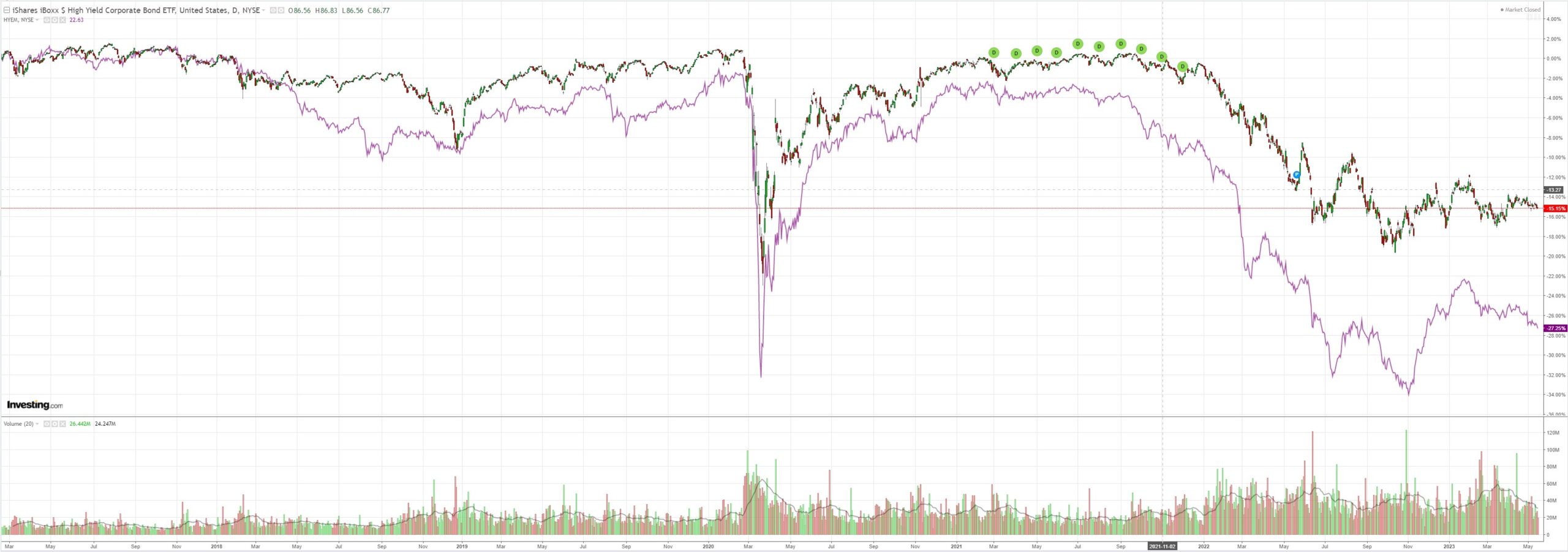

As junk warns:

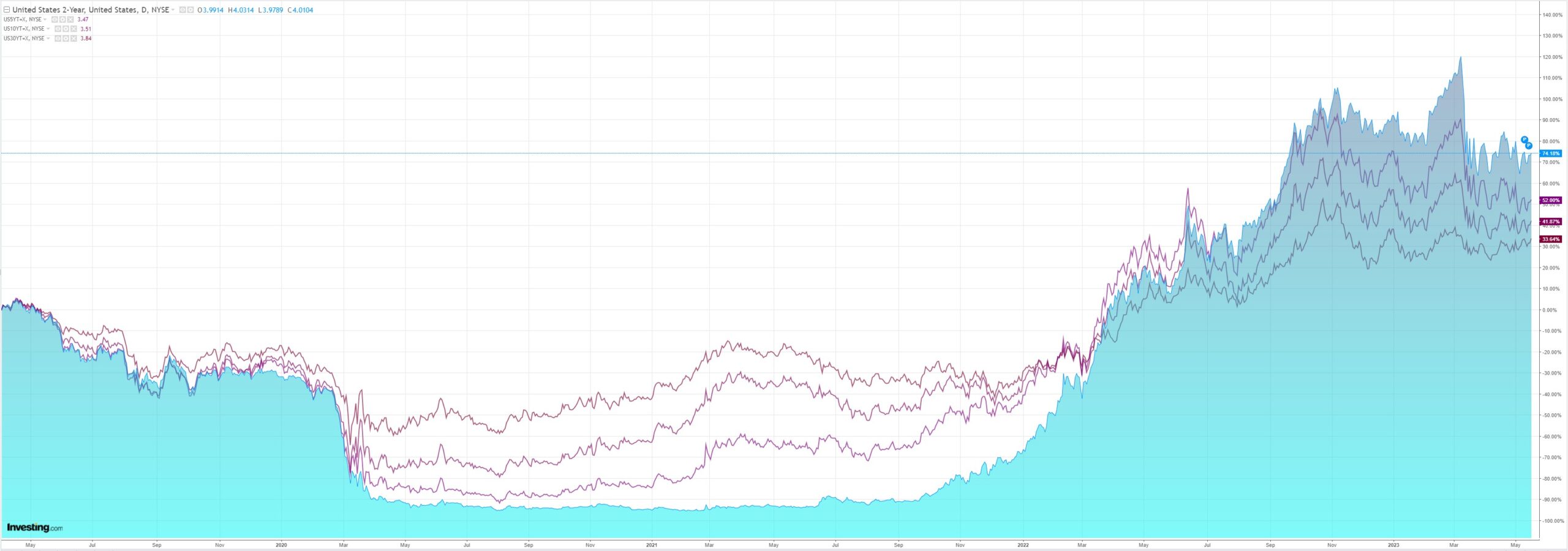

Yields are stuck:

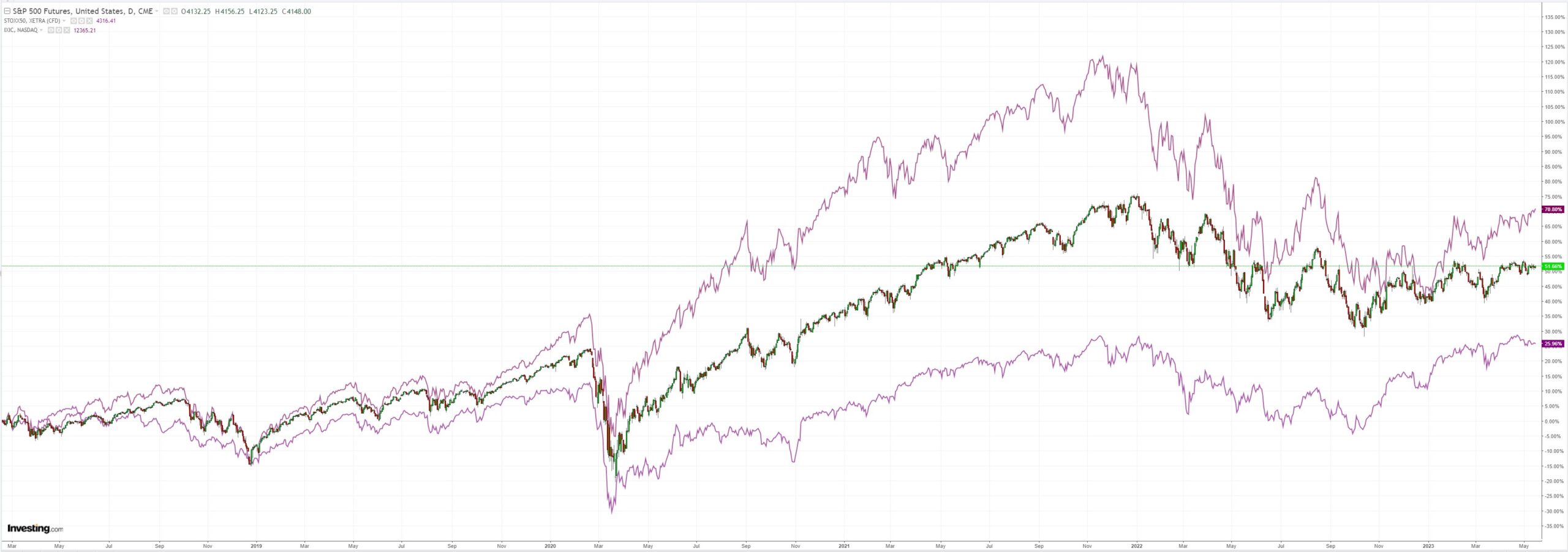

And stocks:

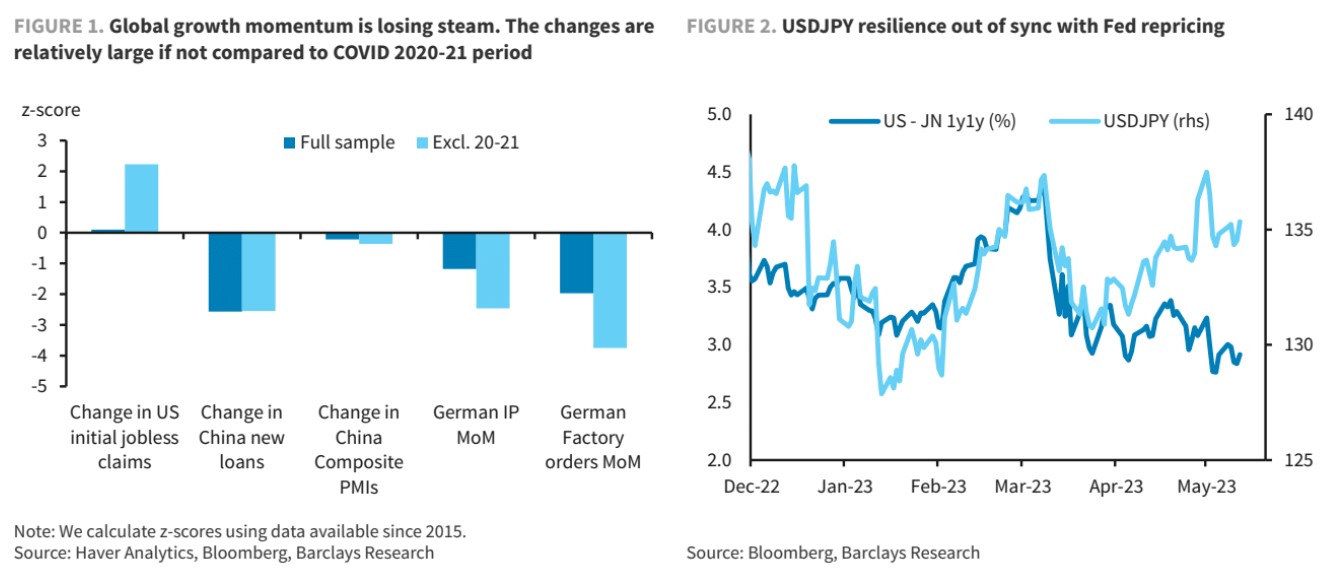

Barclays neatly observed what’s happened:

A slew of data from around the world appears to be signaling a sudden loss of momentum in global activity (Figure 1). Most conspicuously in China, trade, new loans and PMIs all lost substantial momentum over the past few weeks. In Europe, we had a large dip in German factory orders, a tightening credit impulse and soft German IP numbers. In the US, initial claims seem to be breaking out higher, super-core inflation is easing and the Atlanta Fed wage tracker fell.

These are risks to our views. First, without a strong impulse for growth outside the US, there is less active reason for investors to buy currencies against the dollar (due to growth or policy).

Second, even if the slowdown spreads in the US, there is still the worry of tail dollar strength via the operation of the well-known dollar smile. To be sure, EUR/$ is still hovering above our near-term forecast (1.08). Still, more than two weeks ago, we worried our forecasts were too conservative – today that view looks dated.

The choppy FX environment of the past few months has shown that it is important not to act too quickly. After decent growth prints in Q1, some of the growth slowdown may be part of the natural volatility in the data. There is also an inventory cycle evident across global manufacturing surveys that may eventually conclude. Lastly, there is space for some policy easing in China. What is more, typically dollar smile properties become more acute amid more extreme shifts in growth than what we are currently experiencing.

Still, our thesis should increasingly now focus on US growth developments and hinge on dynamics of benign moderation in the coming retail sales, home sales, claims and US regional bank surveys. Price action and deposit data across US regional banks, as well as the dynamics of the debt ceiling episode, should also play a role – although none of that points to comfortable risk-taking versus the dollar.

But not uncomfortable. Long DXY at least offers the benefit of being uncrowded versus EUR and CNY stampedes. And both economies look very shaky from the profits standpoint.

Even as the risk of financial shocks rises.

I am still bearish AUD.