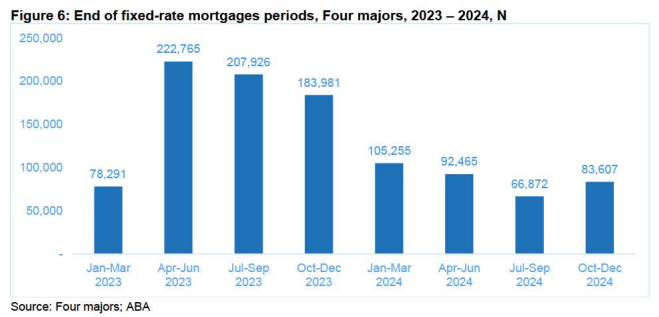

The Australian Bankers Association (ABA) released the below chart showing that more than 600,000 fixed rate mortgages would expire over the final three quarters of this year across the Big Four banks alone:

These borrowers will, in turn, reset from fixed rates of around 2% to variable rates of 6% or more, which will place many (especially first home buyers) in severe financial stress.

There is growing concern that a large share of these resetting borrowers will be unable to refinance to more competitive rates because of the Australian Prudential Regulatory Authority’s (APRA) 3% mortgage serviceability buffer.

This buffer requires prospective borrowers to be able to meet mortgage repayments at 3% above the prospective loan’s interest rate, meaning borrowers will be assessed at around 9%.

Accordingly, a large share of borrowers do not qualify for refinancing, trapping them in ‘mortgage prison’ with their existing lender paying an exorbitant interest rate.

Mortgage professionals like Rate Money’s CEO Ryan Gair are now calling for APRA to remove the serviceability buffer for borrowers seeking to refinance an existing mortgage.

“Home loan buffers made sense during the last few years when we had record-low interest rates. They acted as a contingency for lenders to ensure borrowers could repay their loan”, Gair said.

“However, it’s now become an unfair trap for those looking to refinance the exact same amount – dollar-for-dollar – with a new lender and they’re left paying hundreds or thousands more on the same loan”

“APRA should have separate recommendations to regulate existing borrowers: they should allow those looking to refinance to simply show that they can meet the repayments along the same lines as applying for a new loan, and that your current income can still service the repayments”.

Gair’s proposal makes sense logically as it would ease financial pressures on “mortgage prisoners” (typically recent first home buyers) without adding to new housing demand.

It would also boost competition in the home loan market and lessen the severity of mortgage defaults and forced property sales.

APRA says that its mortgage serviceability buffer is “designed to reinforce the stability of the financial system… ensuring the financial system remains safe, and that banks are lending to borrowers who can afford the level of debt they are taking on – both today and into the future”.

Thus, it is centred around ensuring that new mortgage lending is ‘safe’.

Existing mortgages were already subject to the serviceability buffer when the loan was originated.

They should be free to refinance without meeting the 3% buffer all over again.