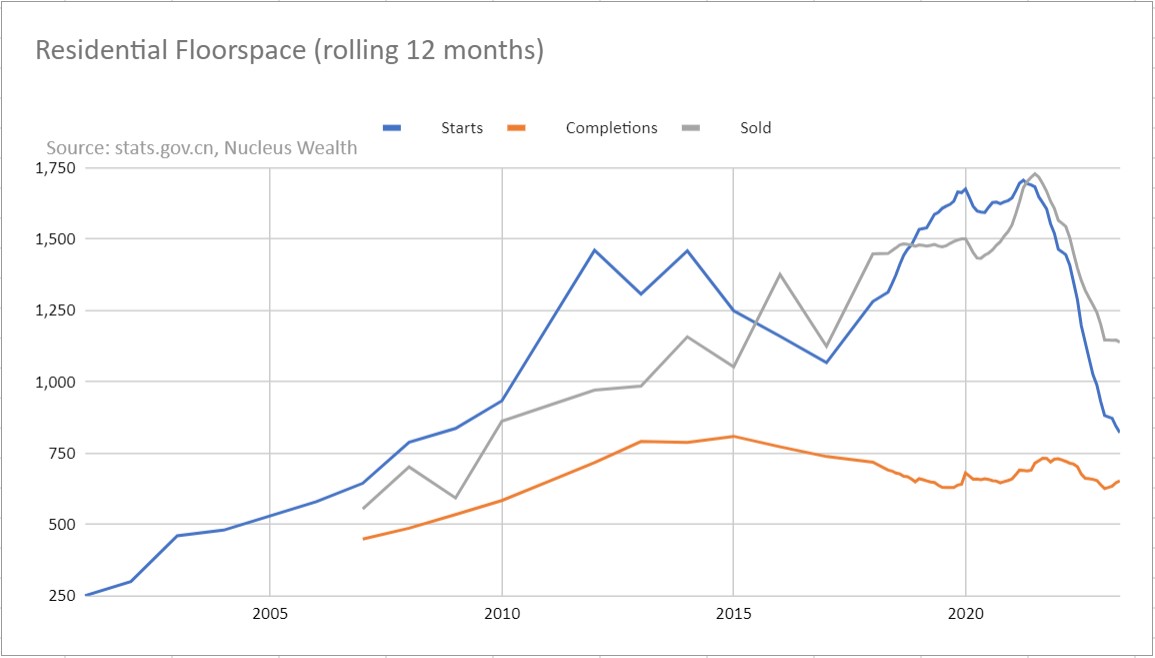

The greatest commodity consumption bubble in history has burst. The Chinese urbanisation boom is over. The chart is millions of square meters:

Don’t ask me to explain the enormous disparities in the data. I can only assume the answer is that China’s enormous developer sector has held equally enormous inventories (ghost cities basically) at various times so there are vast swathes of incomplete apartment buildings.

Starts are down 52% from the peak. At a rough guess, this represents 150mt of annualised steel consumption or 300mt of iron ore.

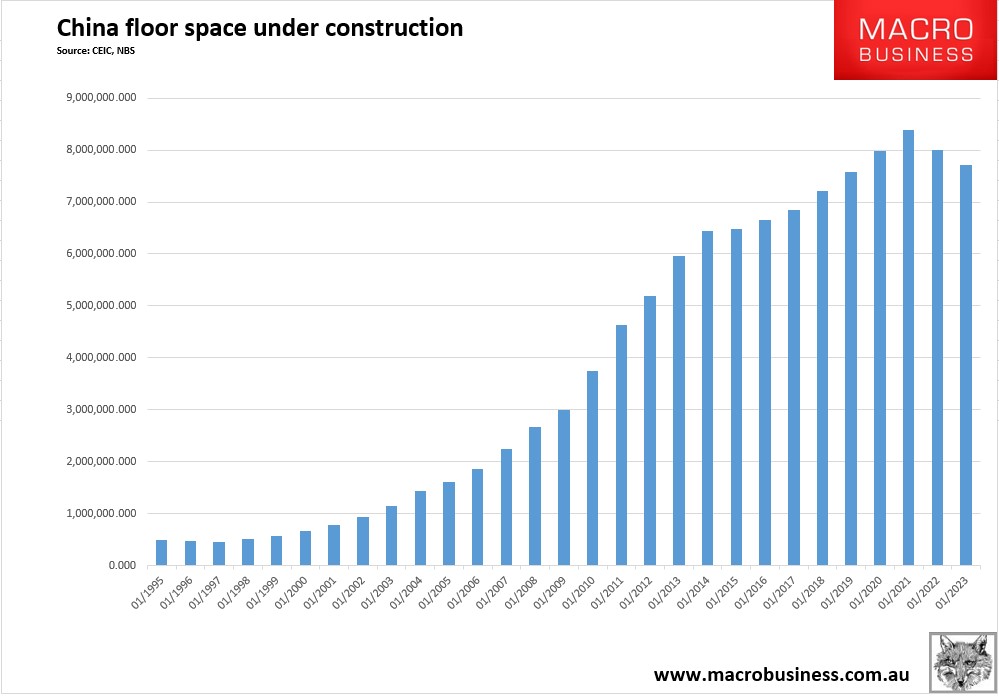

But, if we look at total floor space under construction (which is a year-to-date measure and includes commercial construction) it shows that actual activity has fallen only 8% so far:

But it is falling away at an accelerating rate as stock catches down to flow. It is going to get much worse.

There are some offsets. Infrastructure construction has surged and is now thought to be consuming more than 220mt of steel.

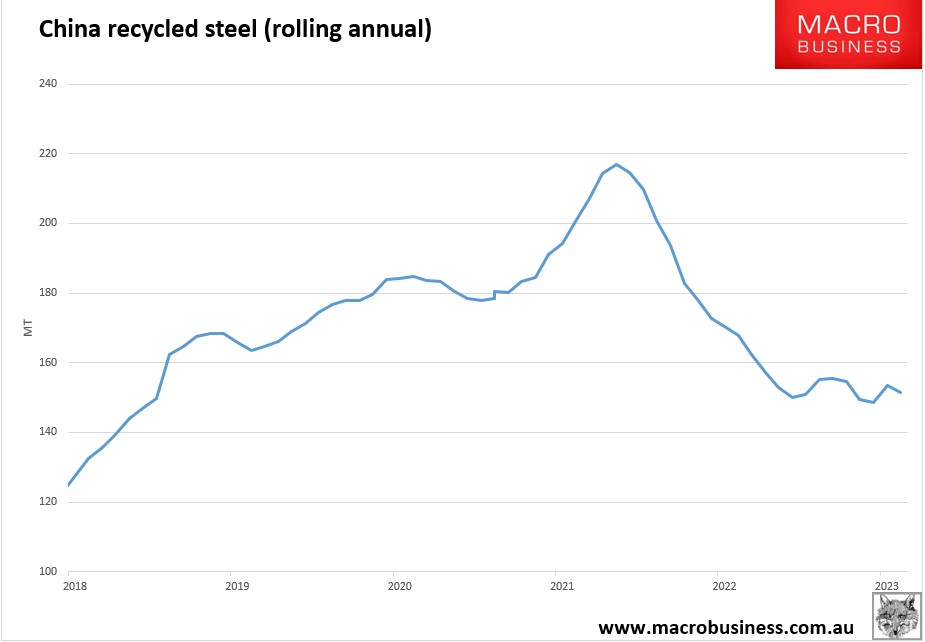

There is also the collapse of steel recycling, contrary to stated policy objectives. Steel recycling is down 68mt since 2021:

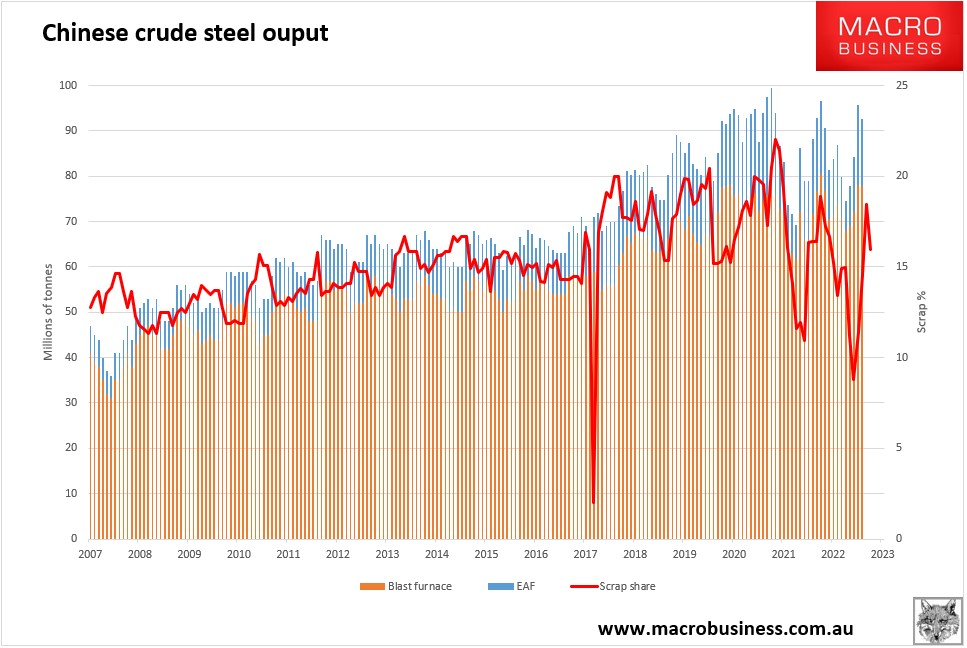

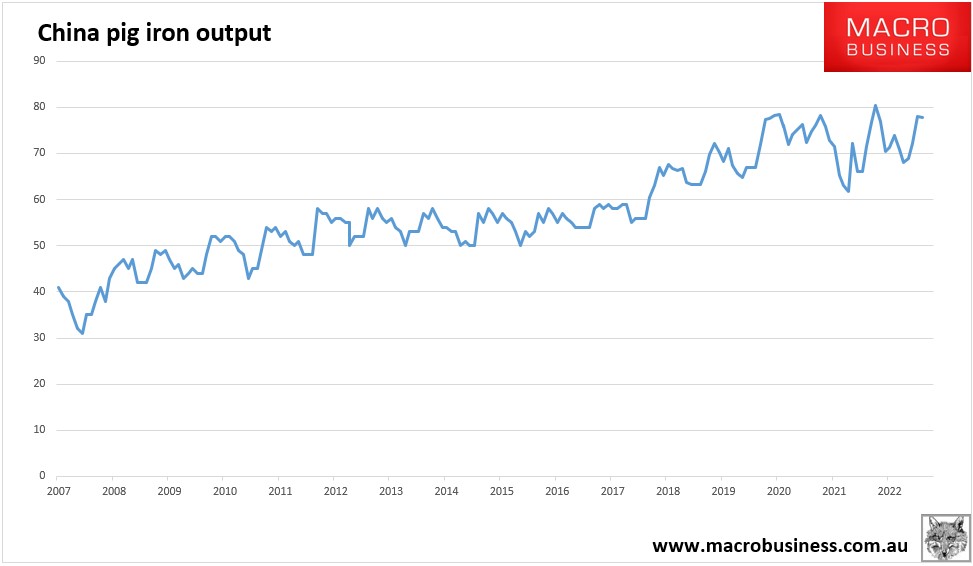

This is why pig iron production and iron ore demand have so far been relatively immune:

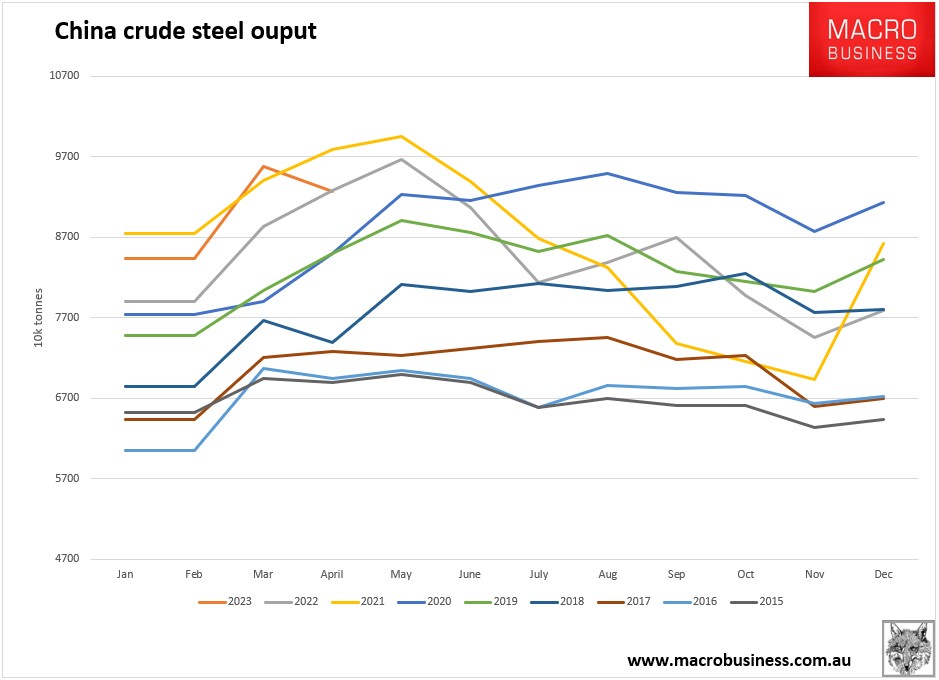

Raw steel output has held up too so far but did roll unusually hard in April as mills realised the property market was not coming to the rescue and inventories were too high:

Unless something changes drastically, another year like 2021 is in the offing as 100mt of steel output is in jeopardy while floor area under construction catches down to starts at the same time that infrastructure eases.

Either China will have to shut its entire EAF fleet or iron ore is going crash as pig iron production adjusts lower.

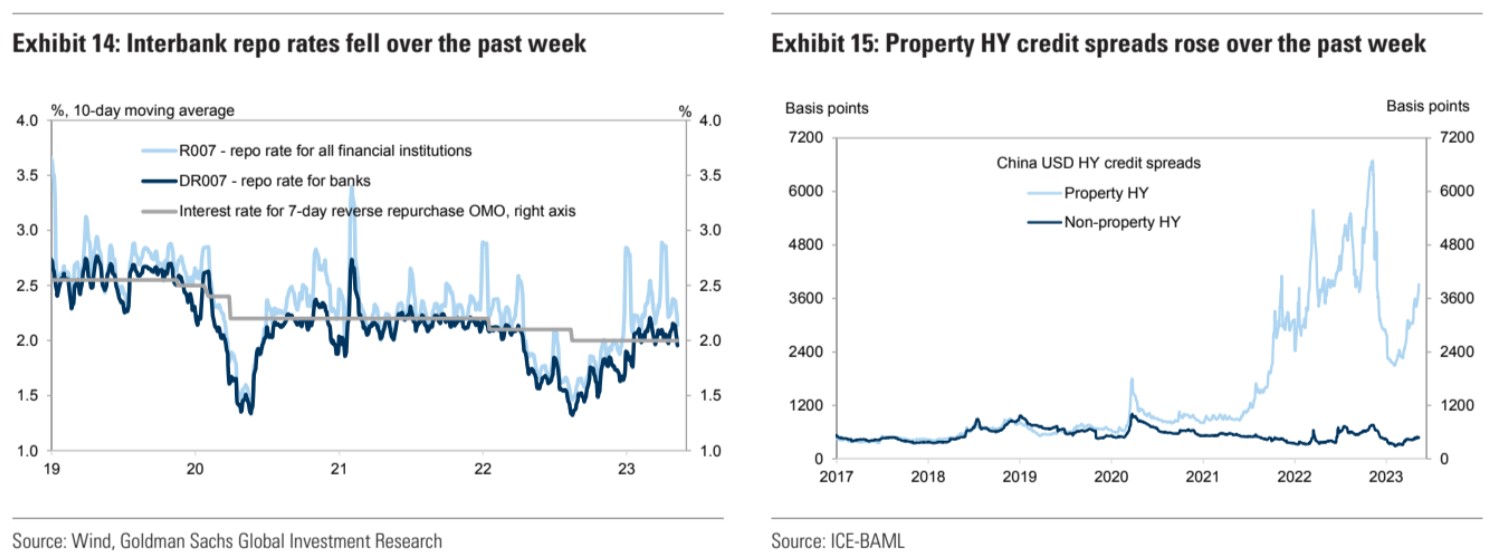

Can China turn this around with stimulus? Perhaps but it is not like previous cycles. Beijing has just spent two years killing the development sector’s capacity to leverage and its credit spreads are getting worse, blocking funding:

If China threw everything at reviving Evergrande and friends, including full public guarantees, it could probably achieve another round of pointless building but the damage to reform credibility would be immense.

More likely is what we have seen so far, with targeted measures in infrastructure. Though debt is an issue in that segment as well.

This bust looks like the end of the road for China’s growth era and iron ore plus coking coal are yet to adjust.