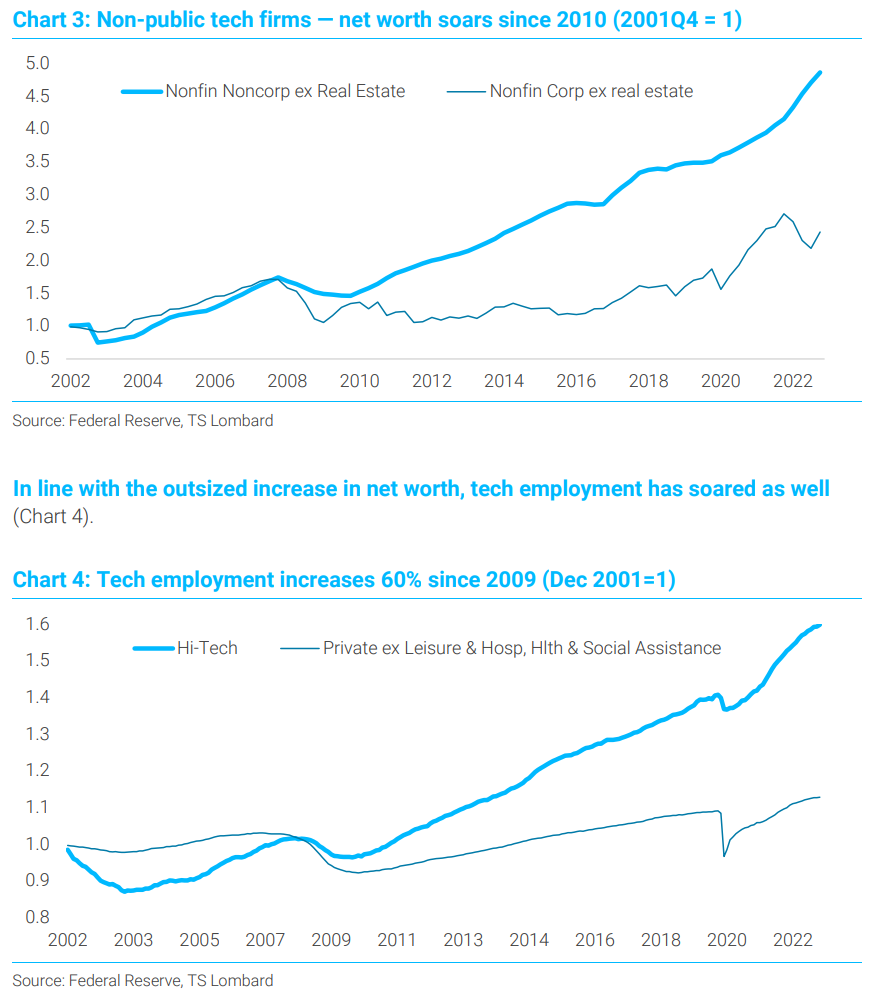

Steven Blitz at Lombard has a good take.

Any relationship between ADP and Friday’s employment number is accidental, but the ADP data along with other indicators do sync to suggest the economy’s momentum is towards recession. Every downcycle has its poster child for what got overbuilt, distorted, during the preceding expansion, and this is tech’s turn. Happens every cycle, an industry convincing themselves and investors they are a growth industry immune to economic cycles and then discovering they are a cyclical business, after all. Commercial real estate (CRE) is an obvious problem, and a coming issue for banks, they hold 50% of commercial mortgages, but CRE is not close to the relatively larger sized problem it was in 1990. As for inflation, high price levels, as opposed to rate of change, need to reverse for some items for consumers to regain lost spending power. If not, wage pressures will continue and feed on itself. This is behinds the Fed’s drive to raise unemployment, but how high to lower prices and reduce bargaining power is a matter of conjecture (I am still thinking 5.5%-6.0%, the Fed is at a politically acceptable 4.5%) The coming reversal in credit extensions will also help to lower inflation by pulling down service price inflation ex shelter — and the dollar’s downward impact on goods price is also not yet done. In the end, see the coming downturn as a recession correcting the excesses of 2010-19, such as they were (tech and asset values), not simply a correction to the post-Covid boom, and this means a smaller downturn than 2008-09, but a downturn, nevertheless.

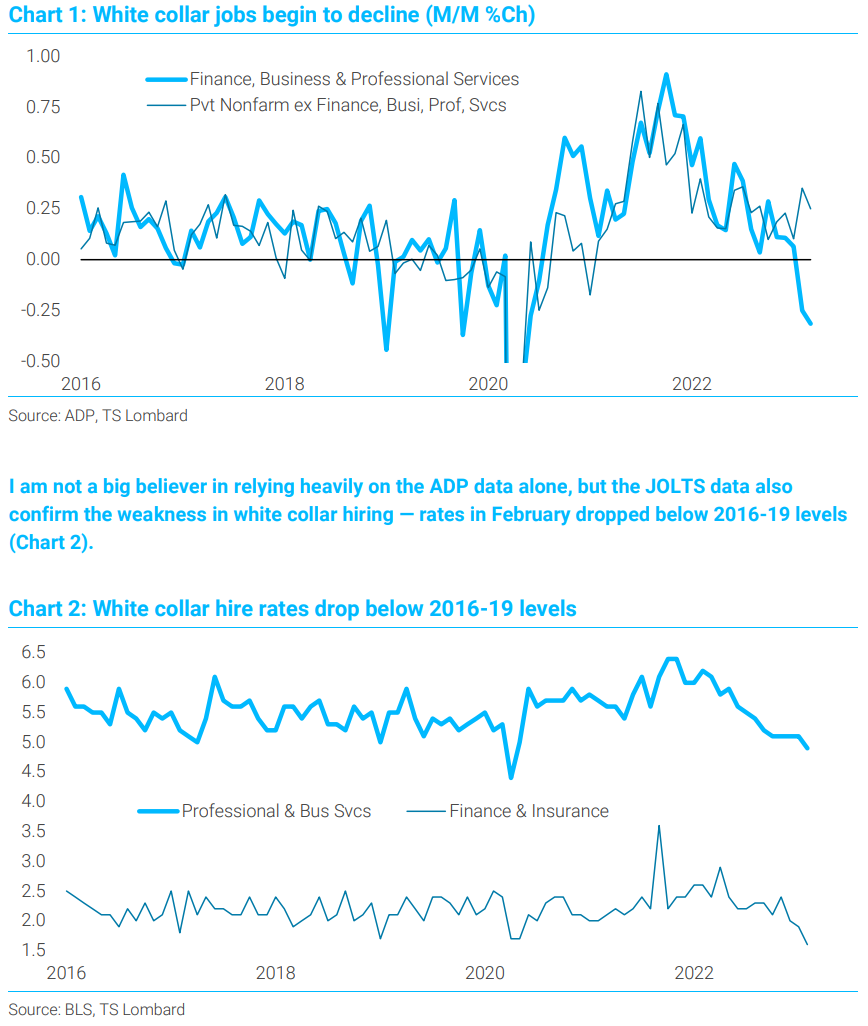

We will see Friday whether March adds onto February’s employment data that indicated an ongoing slowdown in the pace of hiring ex restaurants, retail, and health services — a typical pre-recession pattern. March ISM data on employment are indicating the same (services are barely above 50, manufacturing below). More to the point, today we got from ADP a decline in white-collar employment like what we saw heading into 2019 (Chart 1). Then the Fed reversed to avoid recession, the opposite policy tack is at play today.