A new report from the Grattan Institute says the federal government could save the budget billions of dollars by cutting generous superannuation tax breaks.

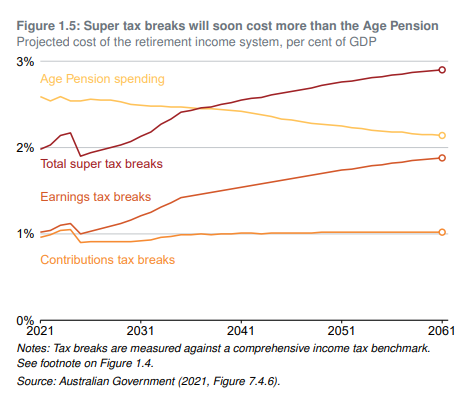

The report claims that the tax breaks currently cost $45 billion a year (2% of GDP) and will soon exceed the cost of the aged pension – a claim also made recently by The Australia Institute.

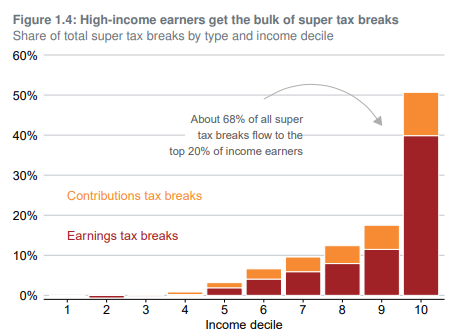

More than two-thirds of these super tax breaks also flow to the top 20% of income earners:

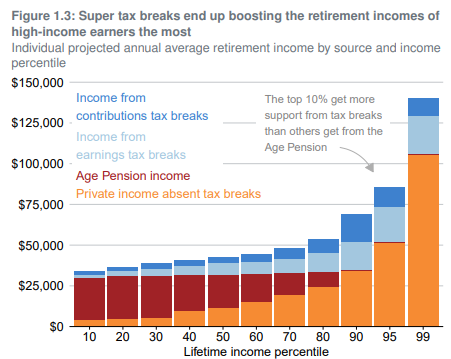

In turn, superannuation boosts the retirement incomes of high-income earners the most:

Grattan claims that these excessive super tax breaks result in “taxpayer-funded inheritance schemes” for the rich because “much of the boost to super balances from tax breaks is never spent”.

As a result, “by 2060, one-third of all withdrawals from super will be via bequests – up from one-fifth today”.

Grattan’s 10 recommendations include cutting the pre-tax contributions cap from $27,500 a year to $20,000 and taxing super earnings in retirement at 15%, as they are before people retire.

These changes would raise billions in revenue every year.

The Australian Treasury’s Retirement Income Review similarly bemoaned that superannuation has morphed into a wealth accumulation and transfer scheme that is increasing inequality.

“Inheritances are significant, representing the transfer of wealth from one generation to another. They are not distributed equally and increase inequity within the generation that receives the bequests”, the review noted.

“Most people die with the majority of wealth they had when they retired. If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances”, the review warned.

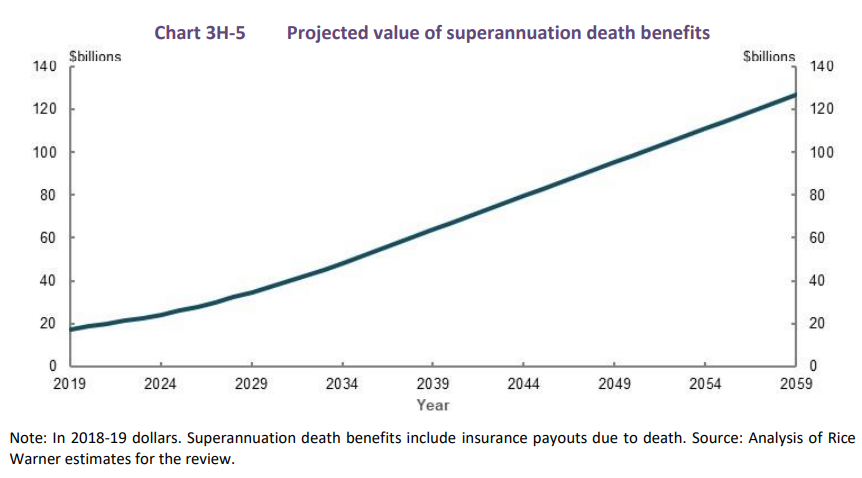

The below Treasury chart tells the tale, showing that “superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059”:

These inheritances are unequally distributed, with “wealthier people tending to receive larger inheritances than those with lower wealth”.

Therefore, superannuation inheritances “increase intragenerational inequity”, according Treasury.

Recent research from Morningstar likewise showed that “hundreds of thousands of Australians have no intention of running down their super to $1 on the day they die”.

Rather, Australians are using their superannuation “as more of a tax-advantaged savings vehicle than a source of retirement income” so they can accumulate wealth to pass onto heirs.

In summary, Australia’s superannuation system fails on practically all policy objectives:

- It is wrongly targeted at the wealthy.

- It costs the budget far more than it saves in aged pension expenses.

- By encouraging tax avoidance and wealth accumulation, it perpetuates inequality.

In light of the enormous fiscal cost and the detrimental effects on equity, the federal government must make a concerted effort to rein in the superannuation system.

It should start by abandoning further scheduled increases in the compulsory superannuation guarantee, alongside implementing strict accumulation caps and making superannuants draw-down their nest eggs.

Because continuing as is will only make the federal budget’s long-term sustainability worse and widen inequality.