The Reserve Bank of Australia’s (RBA) latest Financial Stability Review (FSR) provides some concerning statistics around the vulnerability of Australian mortgage holders.

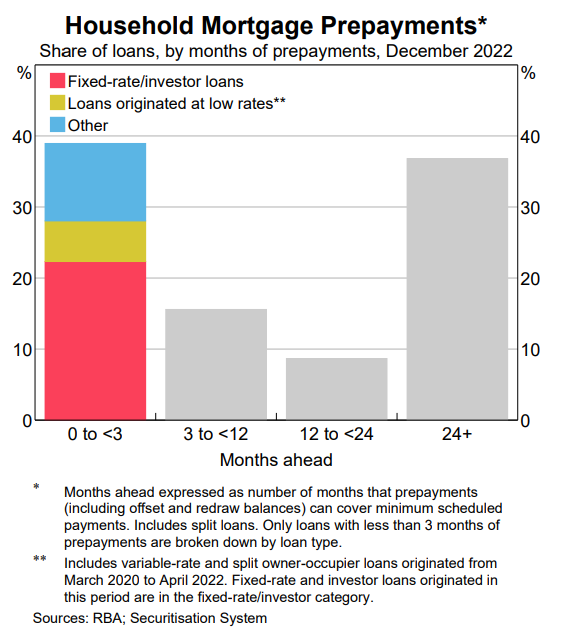

The FSR notes that around 40% of loans have less than 3 months of prepayment buffers, with more than half of these fixed rate borrowers:

The FSR also notes that “borrowers on fixed rates tend to have larger balances relative to borrower incomes and higher loan-to-valuation ratios (LVRs) than variable-rate loans”.

This “partly reflect[s] that fixed-rate loans are newer than variable-rate loans and so borrowers have had less time to accumulate equity or liquidity buffers”.

Therefore, “some borrowers on fixed rates could be at higher risk of entering financial stress when their mortgage payments increase”.

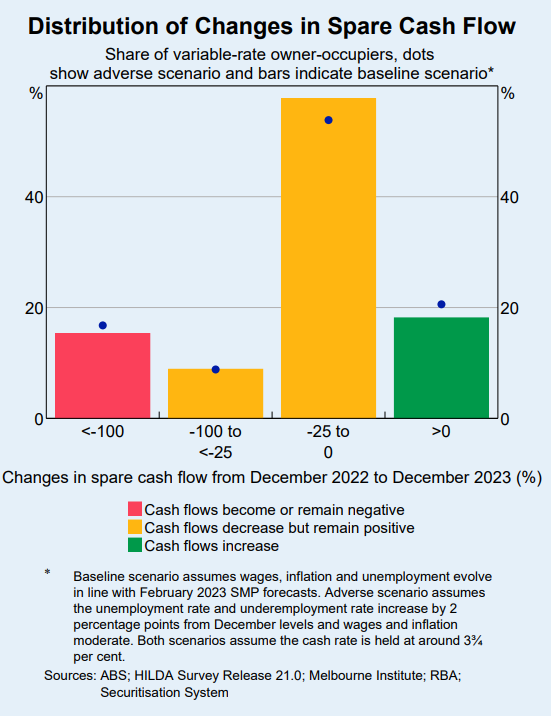

The RBA’s scenario analysis indicates that, based on its baseline forecasts, 15% of variable rate owner occupier borrowers would have negative cash flow (i.e. disposable income less than mortgage payments and essential spending) by year end if the cash rate rises to 3.75% (i.e. 0.15% above the current level):

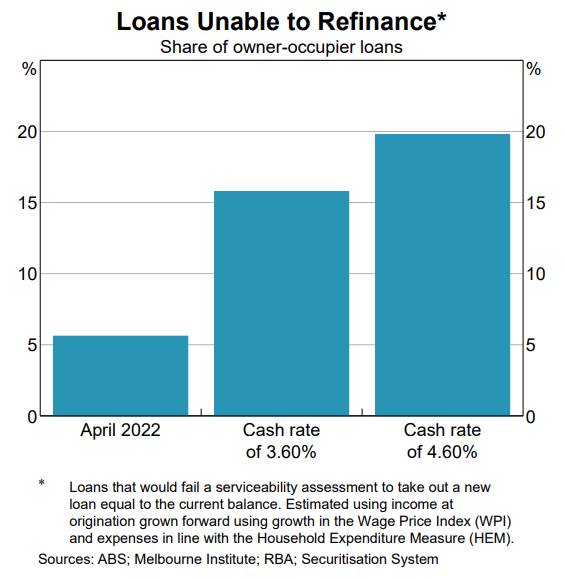

Finally, the FSR estimates that around 16% of owner occupier housing loans would not meet serviceability assessments at current interest rates and would be unable to refinance:

“Newer borrowers are over-represented in this cohort, especially the small share who borrowed close to their maximum capacity when interest rates were very low”, the FSR notes.

The RBA’s cumulative rate hikes have slashed borrowing capacity by 30% and lifted variable mortgage repayments by around 50%, according to Canstar.

APRA’s 3% mortgage serviceability buffer also means that borrowers are being assessed at an average variable rate approaching 9%, which has trapped many in their existing loans.

The head of the Finance Brokers Association of Australia (FBAA), Peter White, recently warned that “borrowers are becoming ‘mortgage prisoners’, locked into a situation where they can’t access a better deal because they don’t meet the inflated assessment rate”.

“Others may be forced into selling their homes because the excessive buffer rate holds them prisoner to their current lender as rates rise”, White said.

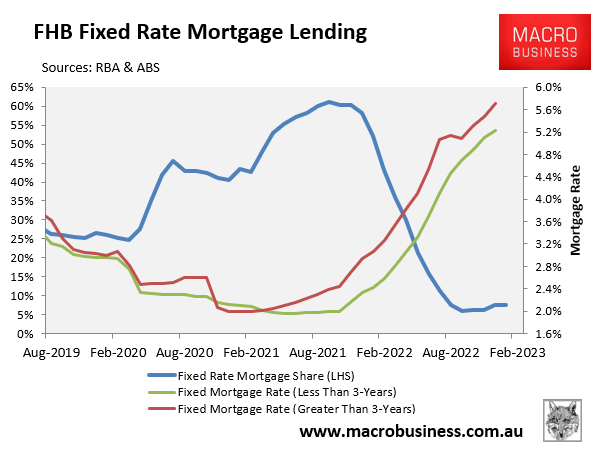

The situation is most concerning for the tens-of-thousands of first home buyers that purchased near the peak at ultra-low fixed rates of around 2%:

A significant share of these first-time borrowers face resetting to mortgage rates that are around triple current levels and being captive with their lender existing lender, unable to refinance to a better deal.