The Australian Prudential Regulatory Authority (APRA) eased mortgage assessment regulations in 2019 by replacing the requirement for lenders to assess borrowers at a 7% mortgage rate with a 2.5% buffer above the loan’s interest rate.

In response to “growing financial stability risks from ADIs’ residential mortgage lending” and fast rising property values, APRA increased the mortgage repayment buffer to 3.0% in October 2021.

Ten consecutive interest rate rises from the Reserve Bank of Australia (RBA) has seen the official cash rate – and by extension variable mortgage rates – rise by 3.5%.

This means that mortgage rates have now risen 1% above the serviceability buffers that many borrowers were assessed at over the pandemic.

In turn, many pandemic borrowers would not pass today’s lending requirements in the face of declining home values, preventing them from obtaining a better offer from a competing lender.

Executive director and head of research at K2 Asset Management, George Boubouras, warns that thousands of Australians have become trapped in expensive mortgages, unable to refinance because they no longer meet lenders’ standards.

“There is without a doubt a big challenge for new mortgage holders over the past three years”, Boubouras said.

“Many are mortgage prisoners and a mortgage prisoner is unable to refinance because of the serviceability buffers”.

Research released last month by Canstar showed that nearly one-quarter of owner-occupiers are making mortgage repayments on rates in excess of 6.5%, which is around 1.5% above the lowest rate on the market.

“For borrowers still in sound enough financial shape to refinance, an interest rate above 6.5% should be blaring alarm bells and sending them off to a bank for a better deal”, said Canstar group executive, Steve Mickenbecker.

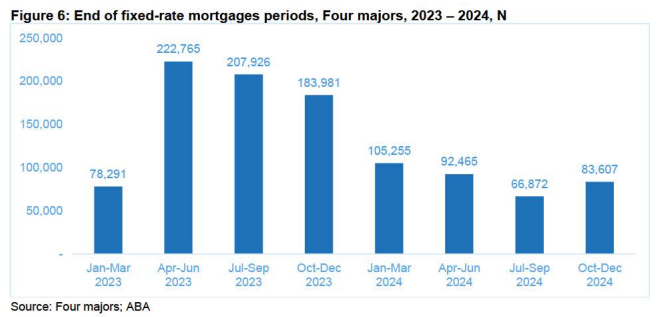

The situation is likely to worsen over the remainder of this year as more than 600,000 borrowers switch from cheap ~2% fixed rate loans originated over the pandemic to variable mortgages with rates above 6%:

In response, Boubouras has called for APRA to reduce the mortgage buffer on existing mortgage holders to enable “mortgage prisoners” on uncompetitive rates to switch lenders.

This idea has merit in my view as it would ease financial pressures on “mortgage prisoners” without adding to housing demand.

It would also boost competition in the home loan market and lessen the severity of mortgage defaults and forced property sales.