The excellent Steven Blitz at TSLombard.

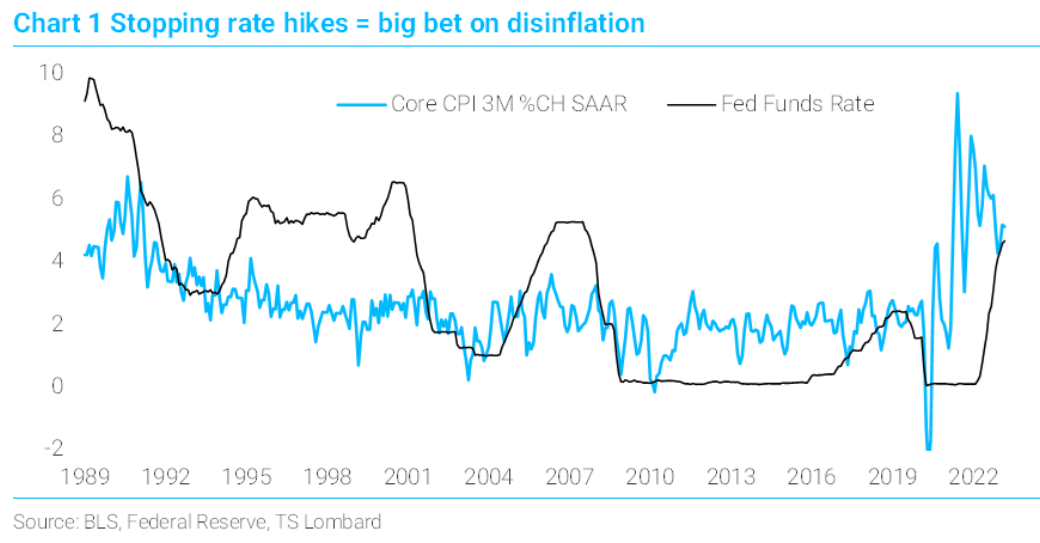

March CPI did not deliver the Fed an excuse to skip a 25BP tightening in May, nor did March employment. The reversal in credit extensions will, if sustained, help flip the economy into recession – but not tomorrow. Finding any excuse to stop tightening has been the Fed’s objective all along, rooted in a transitory view of inflation that is not tethered to employment. They are consequently fearful of creating a recession in real time, even though their own forecast sees unemployment rising to 4.5%, by year’s end – only recession creates that result. Several FOMC members want to stop hiking now, with the funds rate not even at their real long-term neutral of 50BP (Chart 1). Stopping means they are back betting on disinflation itself to get to a near 200BP real funds rate (their forecast, not mine). Problem is, in the past five months, core CPI on a rolling 3-month basis is centered around 5% — a long way from 2%. Fed hikes 25BP in May.

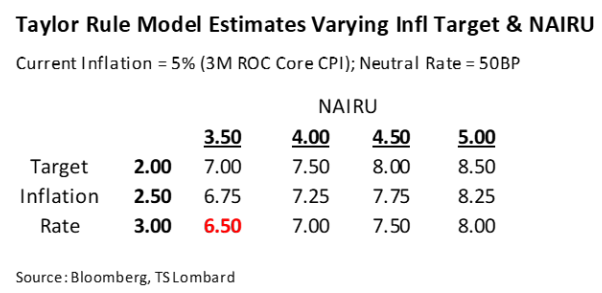

Looking at the Taylor Rule, even an expansive set of inputs (50BP neutral, 3.5% NAIRU and 3% inflation target) puts the funds rate at 6.5%. Which is where it is going IF, somehow, recession is avoided in the near term (table below).