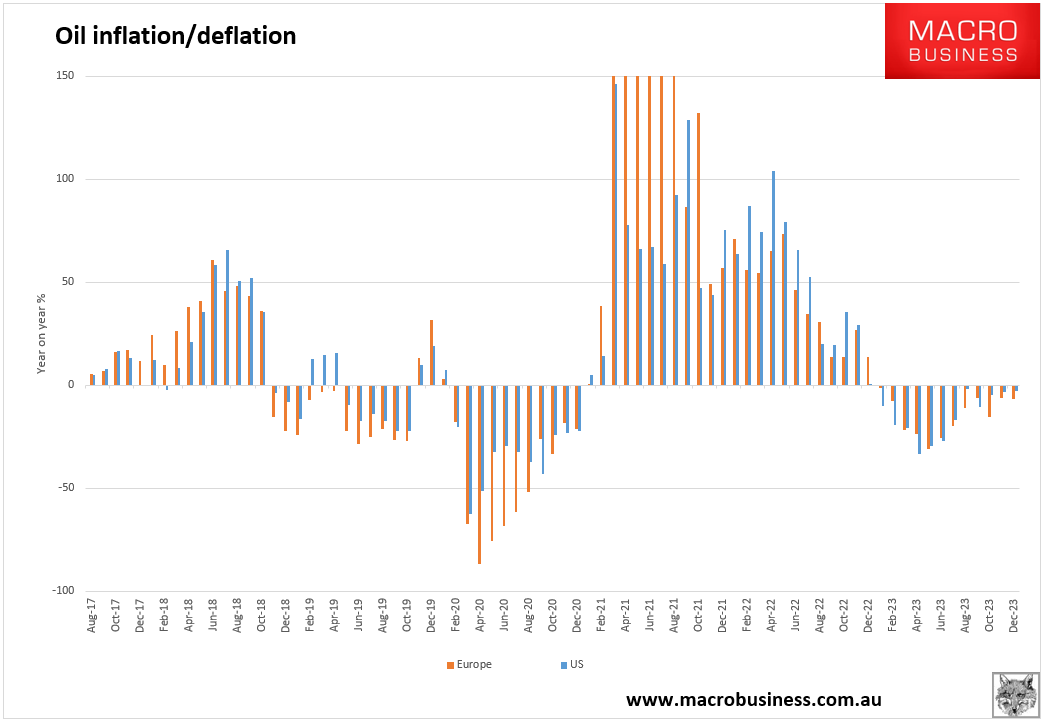

As I said earlier this week, the OPEC cut does not look like an oil shock to me:

Now, others are climbing aboard. BofA has more.

On Sunday, five OPEC oil producers and two non members announced 1.15 million barrels per day (bpd) in production cuts. This follows announced cuts of 2 million bpd fromOPEC+ in October and 500 thousand bpd by Russia in February. The latest announcement pushed the Brent price of oil up from $75.7/bbl(barrels) on Friday to$81.0/bbl as this note publishes. Here we argue that the economic and monetary policy implications are likely to be quite small. Press reports have jumped on this story, arguing that it adds to an already complicated outlook, creating upside risks to inflation and Fed policy. We seethis story differently. Inour view, the headlines should read: “OPEC production cuts create small upside risks to inflation and small downside risks to growth” and “The Fed is watching to see which effect dominates: is the main impact a real-income shock to consumption or a bump up in inflation expectations?