Deloitte’s Weekly Economics Briefing reports that “renters are increasingly being squeezed by higher rents, with little respite in sight”.

Deloitte says it is “an issue of supply and demand, but private dwelling investment is forecast to fall rather than increase through 2023, before recovering modestly in 2024”.

“Construction is expected to commence on only just more than 160,000 dwellings in 2023 and on fewer than 170,000 dwellings in 2024”.

“That result in 2023 would be some 21,000 dwellings below the number that commenced in 2022, and almost 70,000 fewer than the 230,000 dwellings that started construction in 2021”, Deloitte says.

The upshot is that “Australia is building far too few dwellings and, with a myriad of supply side challenges unresolved, that is unlikely to change in the near term”.

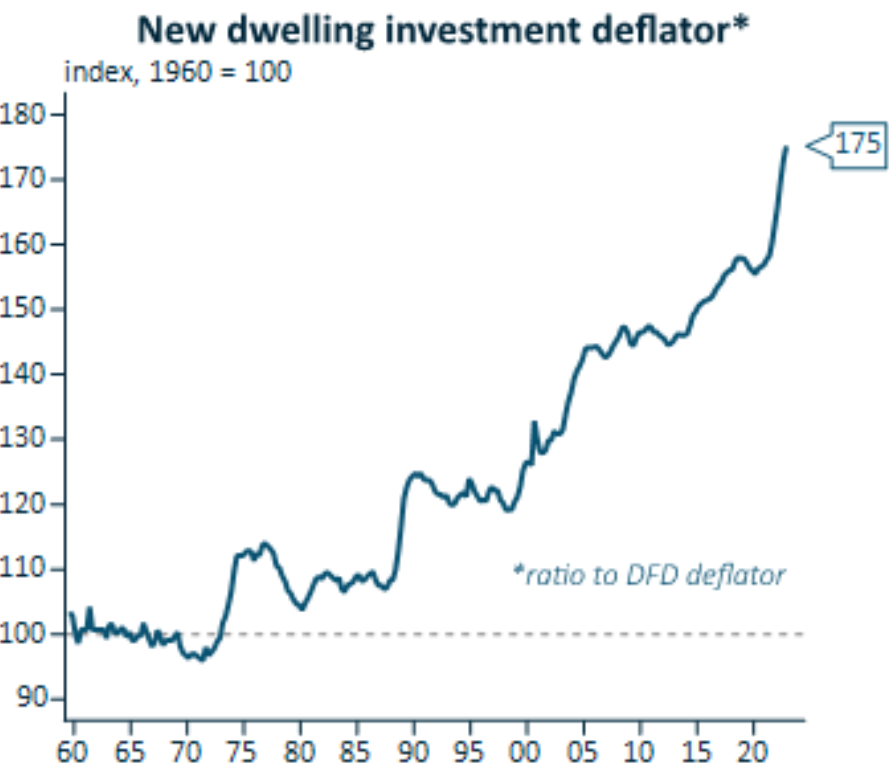

Deloitte’s concerns are justified. Dwelling construction volumes will fall over coming years amid soaring construction costs and tighter financing conditions.

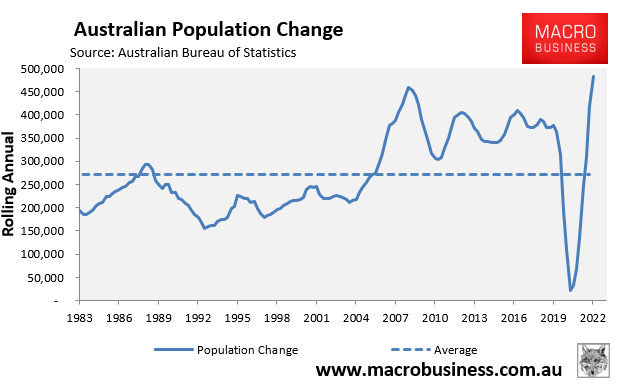

At the same time, population growth soared by a record high 482,000 in the 2022 calendar year on the back of unprecedented net overseas migration:

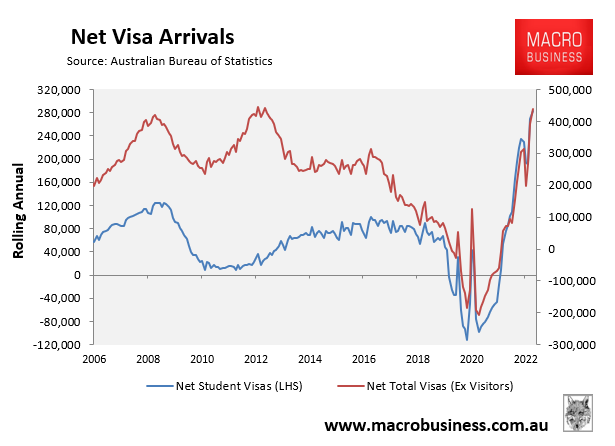

Monthly visa data to March also suggests that net overseas migration will reach new heights in 2023 on the back of soaring international student arrivals:

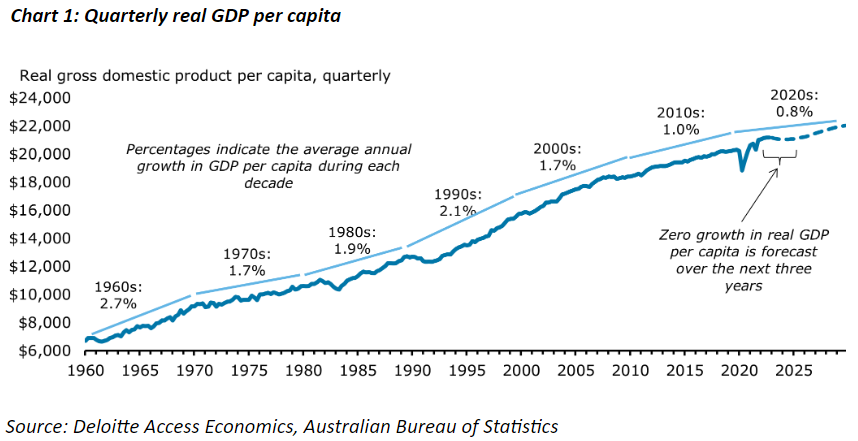

The surge in population growth also means that per capita GDP growth will plunge to levels not experienced since the early-1990s recession, according to Deloitte:

“Deloitte Access Economics has revised down expectations for Australian economic growth in calendar 2023 and 2024 to just 1.5% and 1.2% respectively”.

“If realised, Australia’s growth will be the slowest outside the COVID-19 pandemic since the recession of the early 1990s and see economic activity per capita flatline”.

If anything, Deloitte is being optimistic here.

Australia’s population growth rate will likely be around 2% this calendar year and at least 1.5% next year given the Albanese Government’s extreme immigration settings.

Therefore, Australians will likely experience a deep per capita recession as aggregate GDP growth falls well behind population growth.

The overall economic pie will continue to grow slowly, but everybody’s share of the pie will shrink.