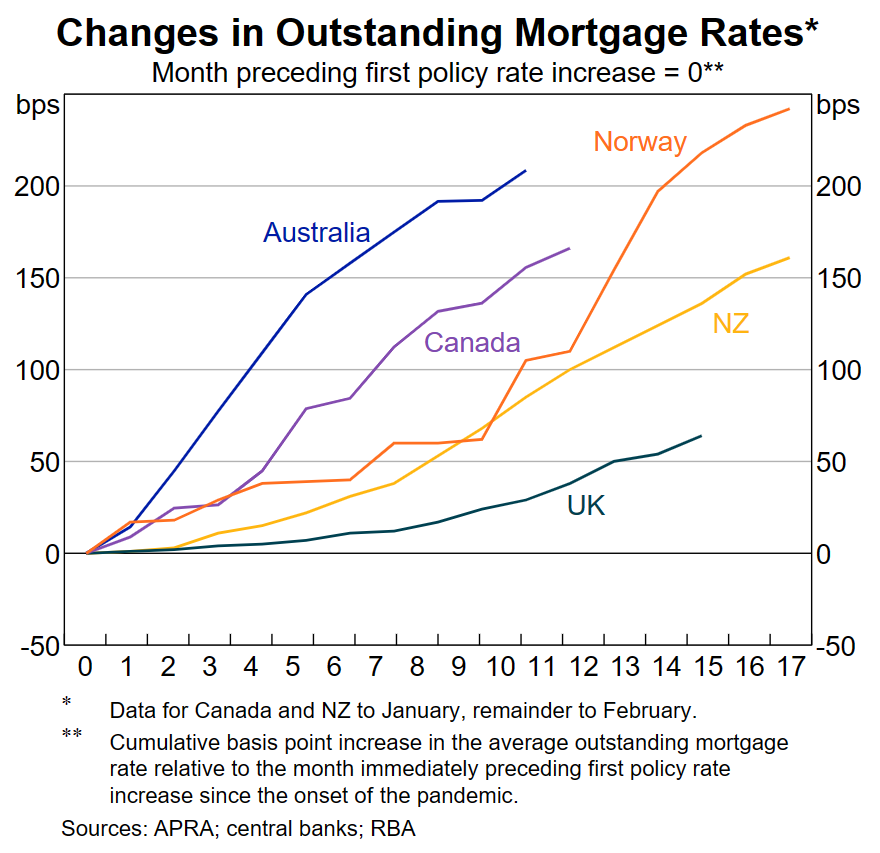

Last week’s National Press Club speech by Reserve Bank of Australia (RBA) governor Phil Lowe included the below chart showing that the rise in mortgage rates in Australia has been more severe than most other developed nations:

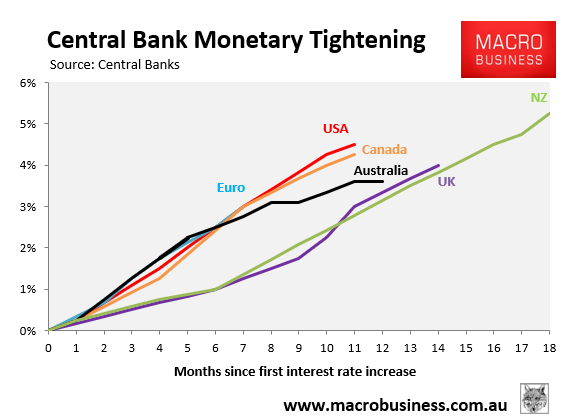

This is despite the RBA lifting rates by less than these nations, as illustrated in the chart below:

Phil Lowe explained the oversized rate increase in Australia is due to “the predominance of variable-rate mortgages”, which “means this is a more powerful transmission mechanism of monetary policy than in many other countries”.

Most economists believe the RBA is either at or close to the peak of the interest rate tightening cycle – a view I agree with.

However, this does not mean that average mortgage rates will stop rising. To the contrary.

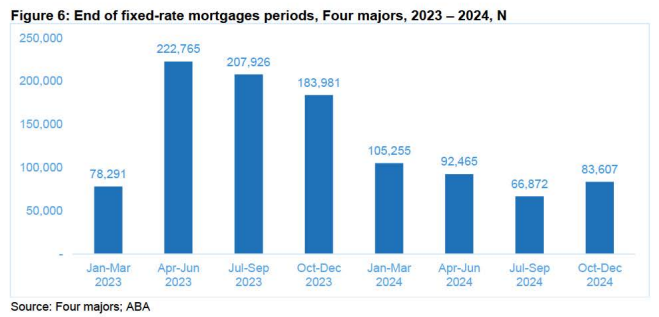

There are more than 600,000 fixed rate mortgages across the big four banks alone that will expire over the June, September and December quarters:

These borrowers will exit ultra cheap fixed rate mortgages of around 2% and transition to variable rate mortgages of around 6%.

In turn, monetary conditions will continue to tighten across Australia, even without further rate hikes from the RBA.

Indeed, Betashares chief economist David Bassanese told The Australian that the fixed-rate “mortgage cliff” would be the equivalent of five 0.25% interest rate hikes.

“The higher than usual expiry of fixed-rate mortgages over the coming two years will result in de facto policy tightening (at least on the mortgage sector) equivalent to around one third of the policy tightening already seen over the past year”, Bassanese said.

“Given this lagged policy impact, it’s little wonder the RBA this week announced a pause in hiking rates”.

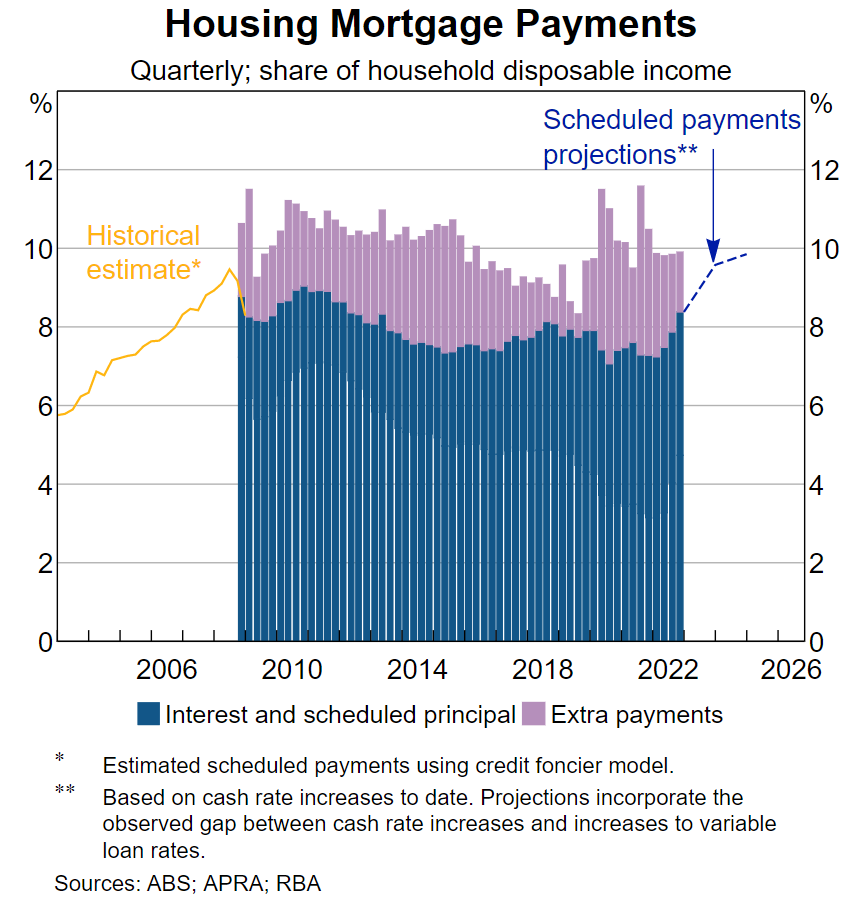

Last month’s speech by RBA assistant governor, Chris Kent, showed that scheduled mortgage repayments will lift to an all-time high share of household income once the fixed rate mortgage reset runs its course:

Viewed in this light, the RBA was justified in pausing rates at this month’s monetary policy meeting.

There is already substantial tightening ‘built-in’ owing to the fixed rate “mortgage cliff”.