The excellent Steven Blitz at TSLombard.

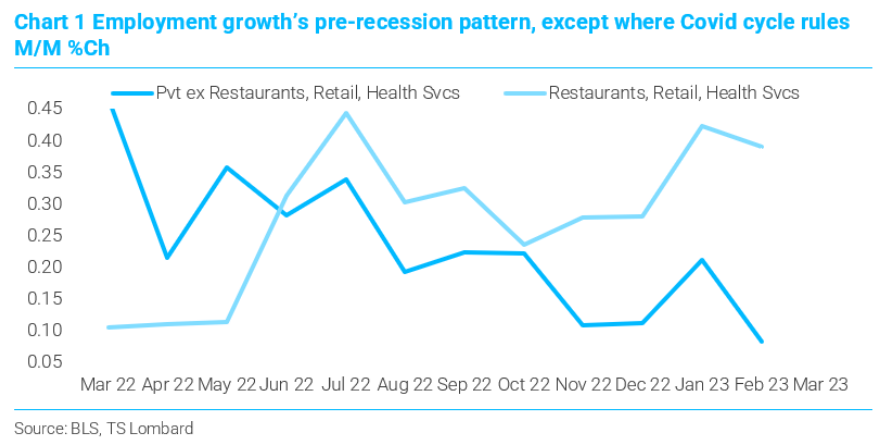

SVB’s failure means that the slow-motion slowdown rooted in an “asset-crunch” morphs into a credit crunch that accelerates the economy’s deceleration. Getting from crunch to employment reversal will prove difficult. The Covidcycle and the “regular” business cycle are, once again, out of sync. The larger Covid-cycle is still returning jobs in large scale because activity is still reverting to pre-Covid patterns, while employment in the broader economy is slowing in a typical pre-recession pattern (Chart 1).

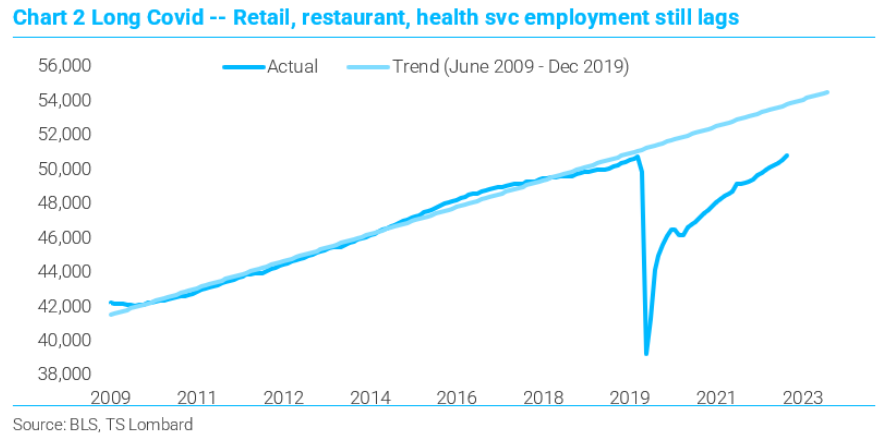

Some 82% of February’s strong 245,000 increase in private sector jobs data came from restaurants, health and social services, and retail — back-and-fill hiring in sectors where employment remains well below its combined 2009-19 trend (Chart 2) and lags the real economy generally – real GDP is 5% above 2019 and back in line with its 2010-19 trend. Still, jobs are jobs and people spend more when they are employed.

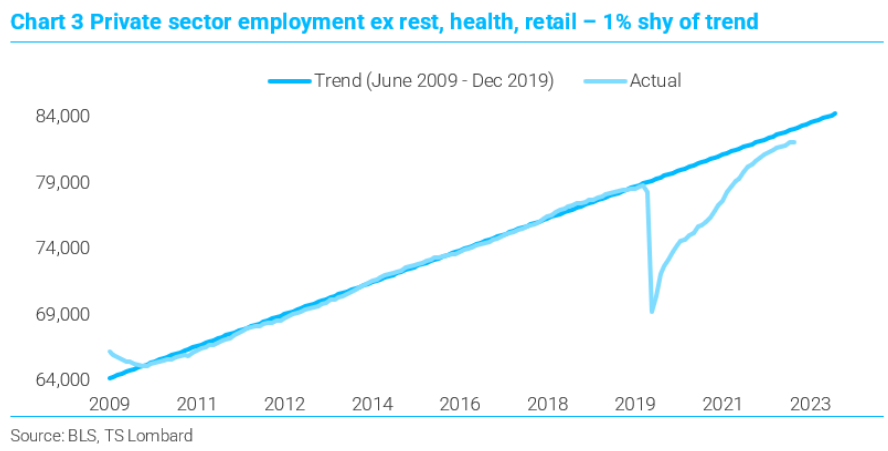

The remaining 18% of the net change in February employment included a 25,000 drop in information employment (tech), and a 10,500 drop in finance and insurance employment. Employment in this group ex retail, restaurants, and health, is only 1% below trend (Chart 3) and m/m hiring is slowing in typical pre-recession fashion (Chart 1). Info (tech) employment is 6% above trend, down from 8% higher in November.

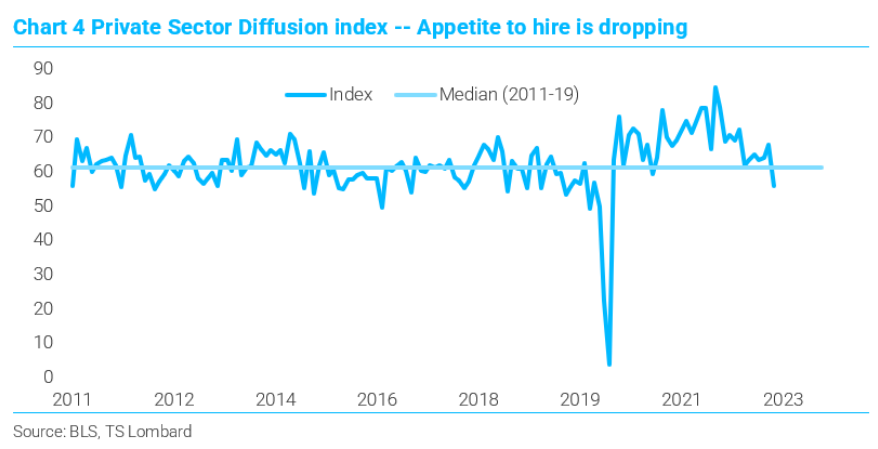

The diffusion index for private hiring (% of firms adding payroll minus ½ of % holding payroll stead) dropped to 56 in February, below the 2011-19 median (Chart 4) – indicative of an economy lowering its appetite for hiring but not yet firing.

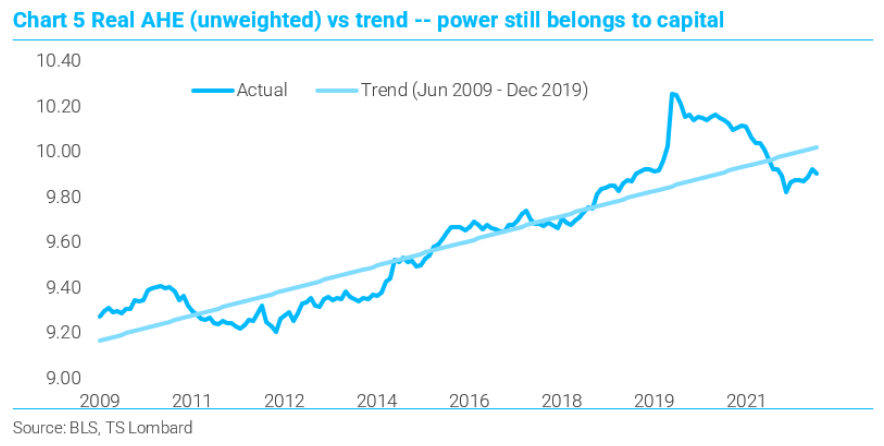

The Fed sees low unemployment as the barrier to bringing inflation back to 2%. Inherent in this view is the notion that wages are driving prices because labor is scarce. Many stats prove this view wrong (wages/profits are lower than pre-Covid) and we see this as well in real average hourly earnings (unweighted so mix/shift in hiring does not skew the results) versus its pre-Covid trend line (Chart 5). This gets updated with CPI next week, but the nominal m/m increase in the unweighted AHE was 0.3%in February, down from 0.32% in January and 0.45% in December.

Regardless, the Fed’s prescription to cut inflation is to raise unemployment by getting the real funds rate to create a “credit crunch” – much more difficult in this cycle. Bank lending is, however, already slowing – the annualized 4- week pace was over 18% in summer and is now 5%. The pace will slow further and possibly reverse – SVB, a rising cost-of-funding, and inverted real yield curve ensure that. The difference between 25BP in March versus 50BP is belief, hope, that a data cliff signaling recession is very close. SVB breathed life into the “cumulative impact” argument to slow down, and then there is politics. They likely keep to 25BP one more time – though they know better. Odds of a mid-year recession are now under 50%, but, in turn, odds of the funds rate going to 6.5% are now above 50%. Recession is still the call.

We can probably surmise that the Fed will now go 25bps in March. Wall Street will love this. Probably rally like mad and guarantee rates need to go to 6%+.

So far we have marched through crises in Arkegos, Credit Suisse, Gilts and regional US banks. Yet we still haven’t broken anything of sufficient size and vulnerability (that is, beyond regulatory rescue) to end the cycle.

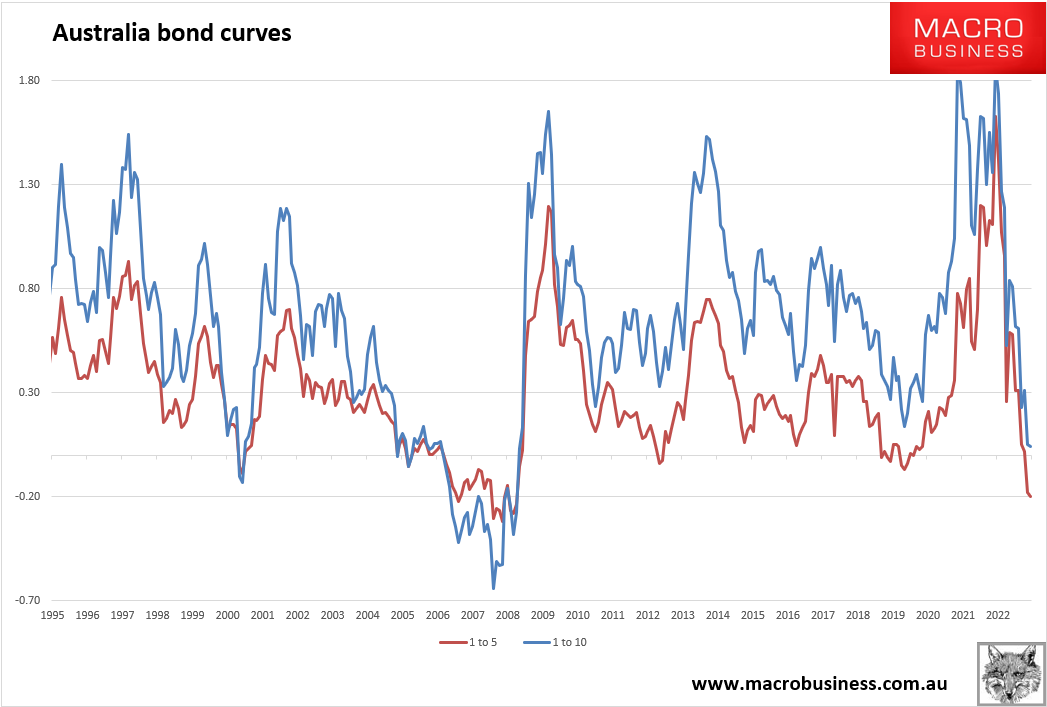

Meanwhile, in Australia, the rate hike cycle is effectively done. Three year bonds are now pricing the better part of two rate cuts so fixed mortgage rates are about to come down.

The 1-5 and 1-10 curves are both very bearish as well:

If the RBA goes one more in April, it will be the last.