I am loving the work of TSLombard’s Steven Blitz.

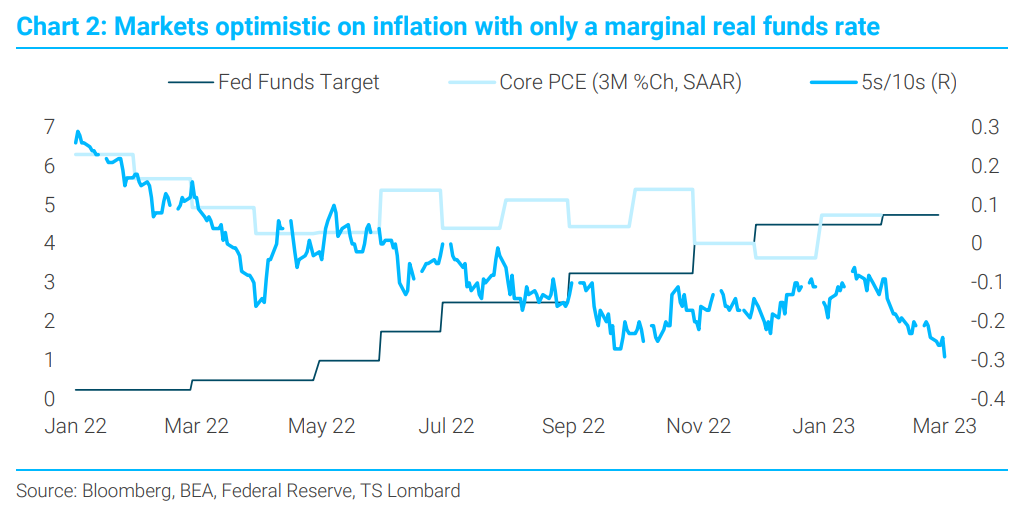

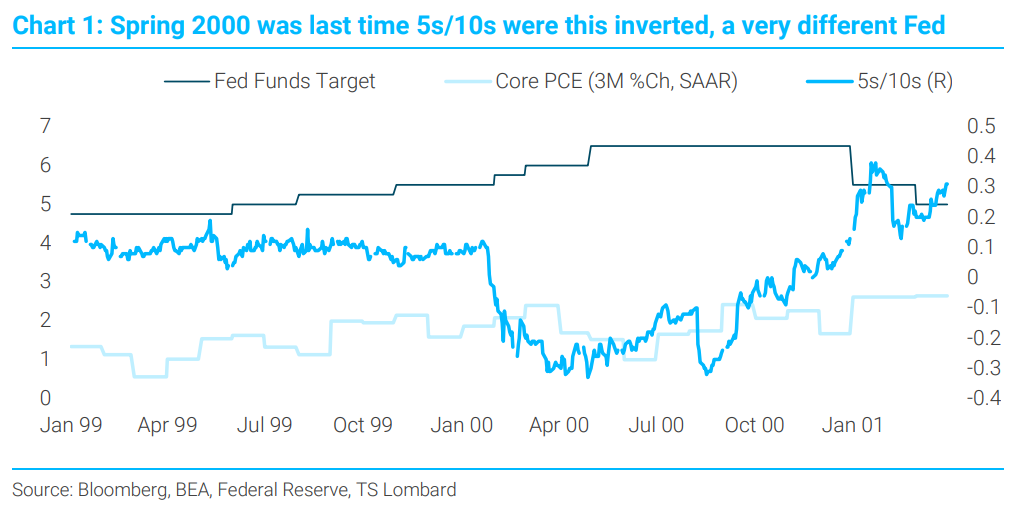

There is an unwavering belief among many traders, investors, economists, policymakers and the like that inflation returns to 2% by matter of divine right. No recession needed or even probable. How else to explain why the 5s/10s curve, the market’s bet on the course of future inflation, is about to invert past its recent -32BP mark and is threatening to take out the previous max inversion reached in Spring 2000 (-33BP to -42BP, depending on your source). The 2000 inversion was set against a funds rate topping out at 6.5% with inflation running at around at 2.4% (Core PCE, 3M annualized %Ch) (Chart 1). The present inversion comes with the real funds rate just now reaching zero (Chart 2). The Fed is not signalling any 2000-style upward shift in policy rates – real or nominal – and the market believes the same. Disinflation and no recession, all from the magic of a marginally positive funds rate, itself a signal that markets believe the preCovid dynamics are destined to return.

The 1970s was the last time such misguided optimism on inflation’s course and Fed policy was being priced into the 5s-10s yield curve over a long stretch of time. Then, like now, the market disbelieved that what it was experiencing was anything other than a passing event. The market was taking solace in comparisons such as yields having not been this high since the Civil War (they hadn’t been, but subsequently went much, much higher). As for inflation, it always reverted. In the recent memory of that time, there was the post-WWII surge, but there was a recession in 1948-49 that raised the unemployment rate from 3.7% to 7.9%, one year after CPI peaked at 14.5% on a 3M %Ch SAAR basis. Recession eventually followed the Korean War inflation as well (1953-54, unemployment rose to 6.1% from 2.5%). Recessions end inflation.