CMBS and CRE loans are in the gun in the US. JPM has more.

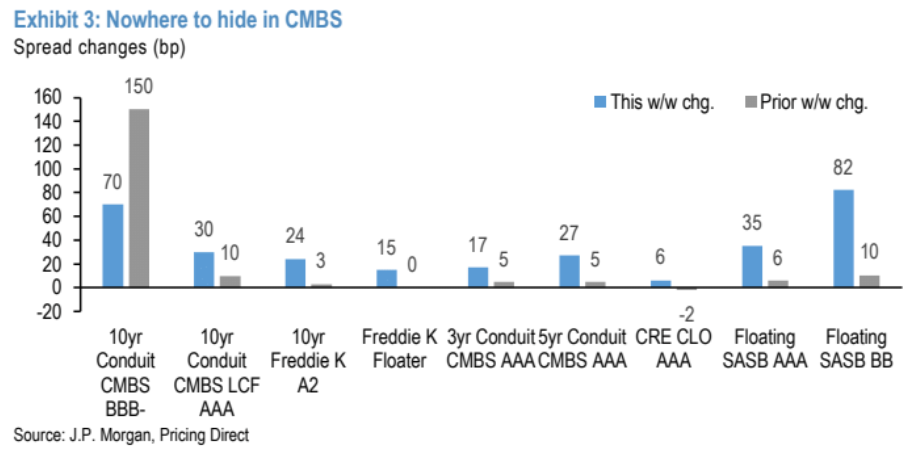

What started as a spread widening episode in IG mezz in the week leading up to SVB’s collapse has infected AAA CMBS this past week regardless of format(Exhibit 3). 10yr conduit LCF AAAs were 30bp wider on the week as of Thursday’sclose at T+168, just shy of the late October 2022 wide of T+171, which was also the widest mark post-GFC outside of the 2020 pandemic shock. Shorter duration AAAswere not spared either. There has simply been nowhere to hide in CMBS as broader risky markets sold off.

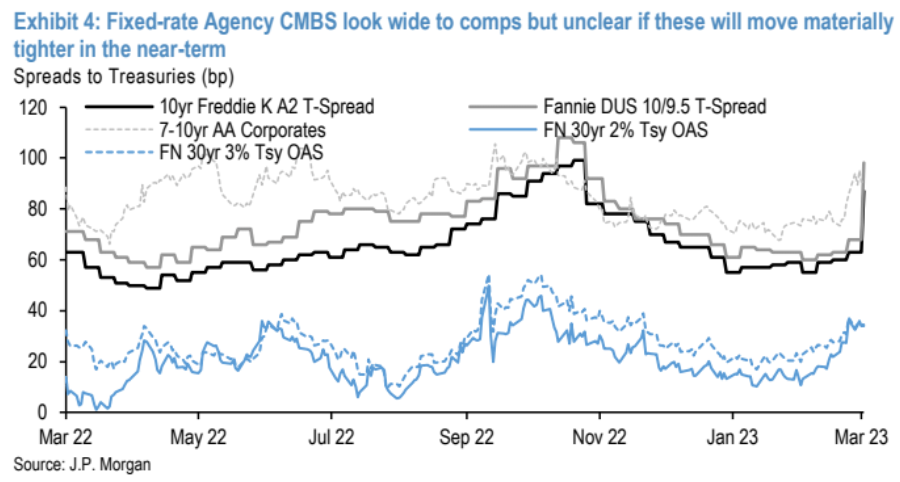

Where we go from here is uncertain, but spreads can remain wide. As our Agency MBS colleagues note(seeAgency MBS), mortgages can remain wide as money managers will remain the marginal buyer. Large banks that are gaining deposits may wait until they better understand duration needs against their new deposits before deploying cash. Recall that our Agency MBS colleagues expected banks to return to being net buyers of MBS securities this year but after recent events, this could take a while longer. If mortgage spreads are expected to remain wide, CMBS spreads will remain wide as well. Agency CMBS looks wide relative to lower coupon mortgages and similar duration AAcorporates (Exhibit 4) but it’s unclear that these will move much tighter in the near-term. IG mezz remains susceptible to further widening as fundamental concerns weigh heavy, and liquidity has been sucked out of the market. At some point IG mezz bonds will be good buys, but a lot of uncertainty remains.