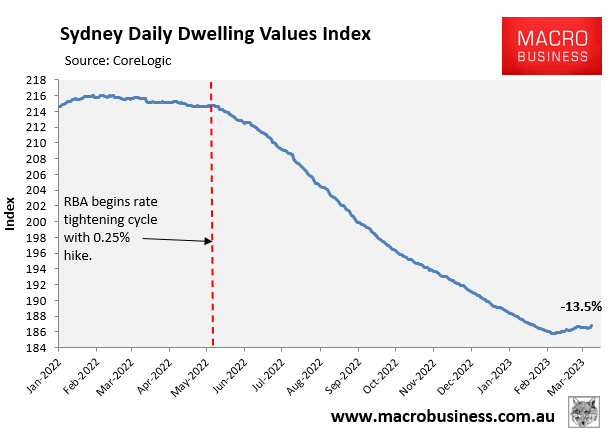

Sydney house prices continue to shrug of the Reserve Bank of Australia’s (RBA) interest rate hikes, with values up 0.13% so far in March, which follows February’s 0.3% increase.

This is according to CoreLogic’s Daily Dwelling Values Index.

In fact, since bottoming on 7 February, values across Sydney have rebounded 0.6%, as illustrated below:

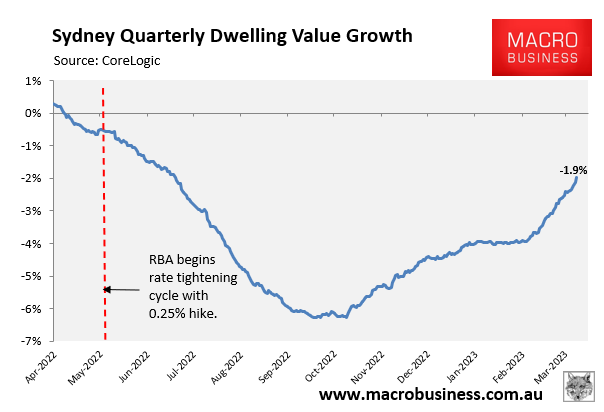

In turn, the quarterly rate of decline has decelerated sharply, from -4% at the beginning of February, to only -1.9% currently:

CoreLogic’s head of research, Tim Laswless, believes the price correction should resume on the back of rising mortgage rates and a softening economy.

“There is a good chance housing values will continue to trend lower from here as the economy weakens and sentiment remains low”, Lawless said.

“Although mortgage arrears have held around record lows, it’s reasonable to expect delinquencies will trend higher through the year, as more households find they can’t continue to service their debt under such a high interest rate environment as well as keep up with the high cost of living”.

It is a view shared AMP Capital’s chief economist, Shane Oliver, who believes the sharp reduction in borrowing capacity would drag prices lower.

“Interest rates are still a lot higher than they were a year ago and people’s borrowing capacity is substantially lower than last year, so it still points to more downside in prices”, Oliver said.

Rich Harvey, chief executive of buyer’s agency Propertybuyer, also warned that the number of forced sales is likely to rise as mortgage rates rise.

“There’s a lot of people in mortgage distress at the moment. While most are still managing somehow, we could see some motivated sellers in the coming months as the impact of rate rises filter through”, he said.

The above dwelling value data obviously does not capture Tuesday’s interest rate hike from the RBA, which is expected to be followed up with additional increases over coming months.

These rate hikes will lower borrowing capacity further, which should logically translate into lower house prices.

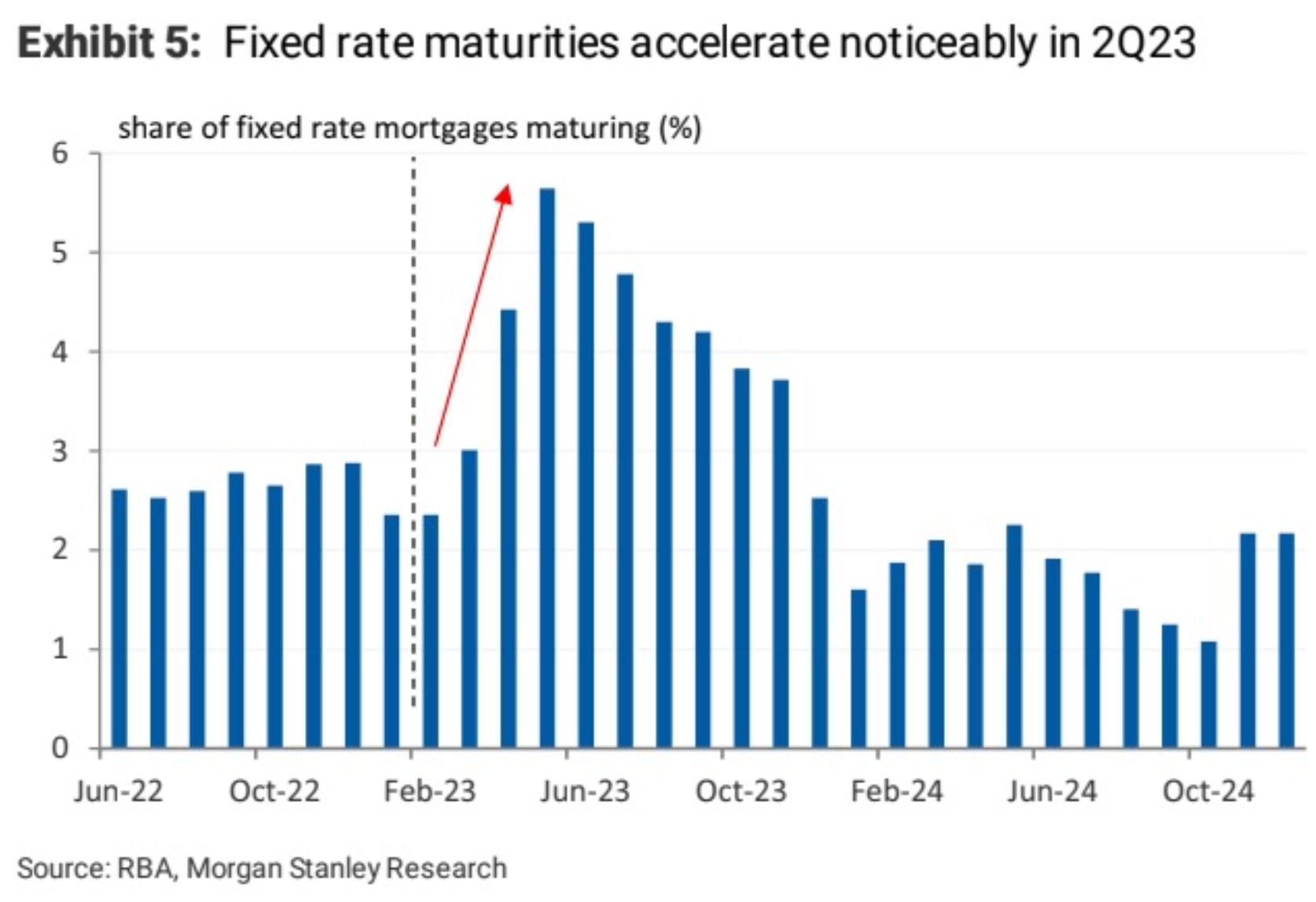

To add further insult to injury, nearly 900,000 borrowers, or 23% of Australia’s total mortgage book by value, will this year switch from cheap pandemic fixed rates to variable mortgages with rates that are more than double current levels.

The below chart from Morgan Stanley highlights the extent of this fixed rate “mortgage cliff”, with the volume of fixed rate mortgages expiring rising precipitously from April, peaking in May, and then remaining at high levels through the remainder of this year:

Many thousands of borrowers risk being pulled underwater as their fixed rate terms expire over coming months.

Accordingly, Australia’s housing market is likely to see a significant increase in forced sales, which will also pull house prices lower.