The media is full of righteous indignation over the Albanese Government’s announcement that it will increase the concessional tax rate for superannuation balances of more than $3 million from 15% to 30% after the next federal election.

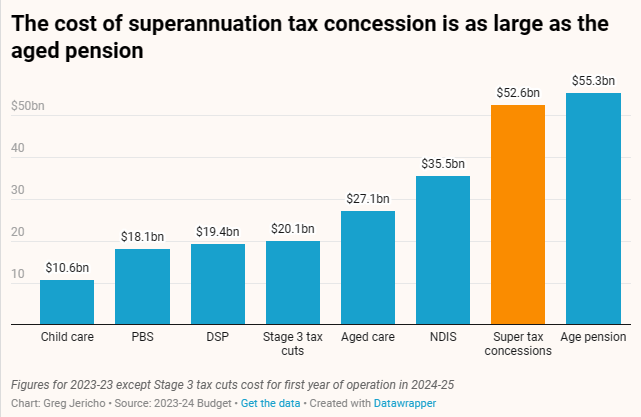

The super changes are expected to hit about 80,000 wealthy individuals, or less than 0.5% of all super accounts, and are expected to shave around $2 billion off the gargantuan ~$50 billion annual cost of superannuation concessions:

Specifically, the tax change will impact 33,500 Australians with $3m-$4m in superannuation, 16,500 who have $4m-$5m in savings, 23,000 with nest eggs between $5m and $10m and 7000 who have more than $10m, according to The Australian.

Nine out of 10 people affected will be baby boomers over the age of 60.

Clime Asset Management chair John Abernethy has labelled Labor’s policy an “attack on large funds” and a “pathetic response, picking on tall poppies”.

Liberal leader Peter Dutton is doing what all oppositions do: committing to reversing Labor’s proposed changes to superannuation tax concessions if the Coalition wins the next election.

Dutton contends that many more Australians will become subject to this $3 million threshold over the next decade or so because it is not indexed to inflation.

We shouldn’t be surprised. The Labor opposition opposed the Turnbull Government’s $1.6 million cap on superannuation contributions in 2016. That’s Australian politics for you.

The fact remains that Labor’s changes are modest and don’t go nearly far enough.

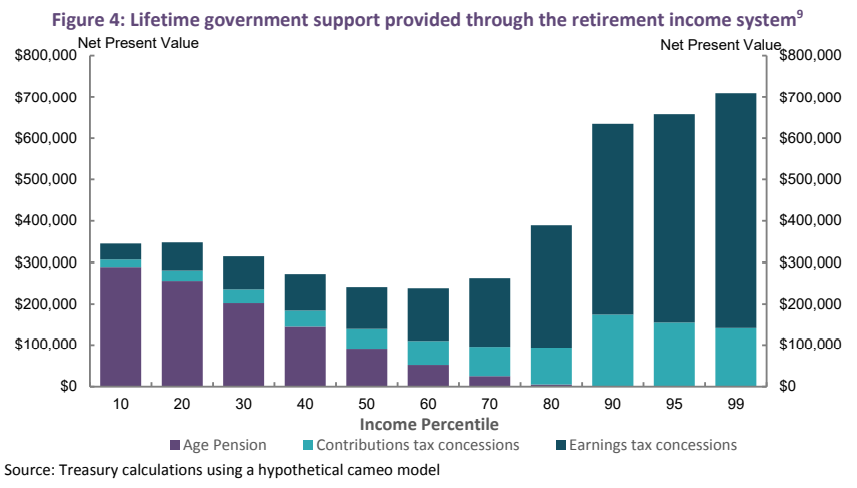

According to the Australian Treasury’s own modelling, superannuation concessions are grossly unfair and flow to where they are not needed: the highest income Australians:

Just look at the above chart. The top 1% of income earners receives around 14-times the superannuation concessions of the bottom 10% of income earners.

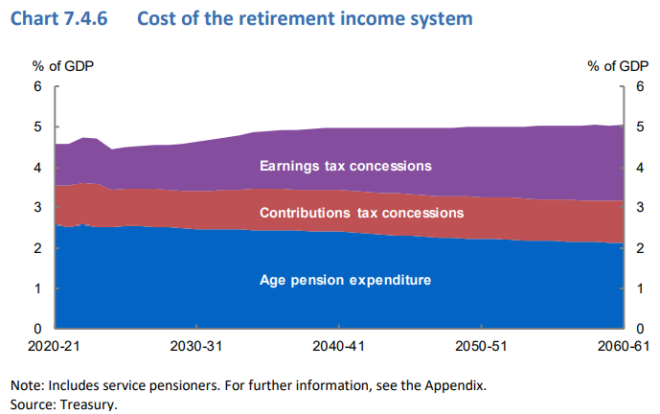

The cost of superannuation concessions must be reined-in, otherwise they will end up costing more than the aged pension, according to the Australian Treasury:

And the more tax revenue that is lost via superannuation concessions, the more taxes will need to rise elsewhere, or the more government services will need to be cut.

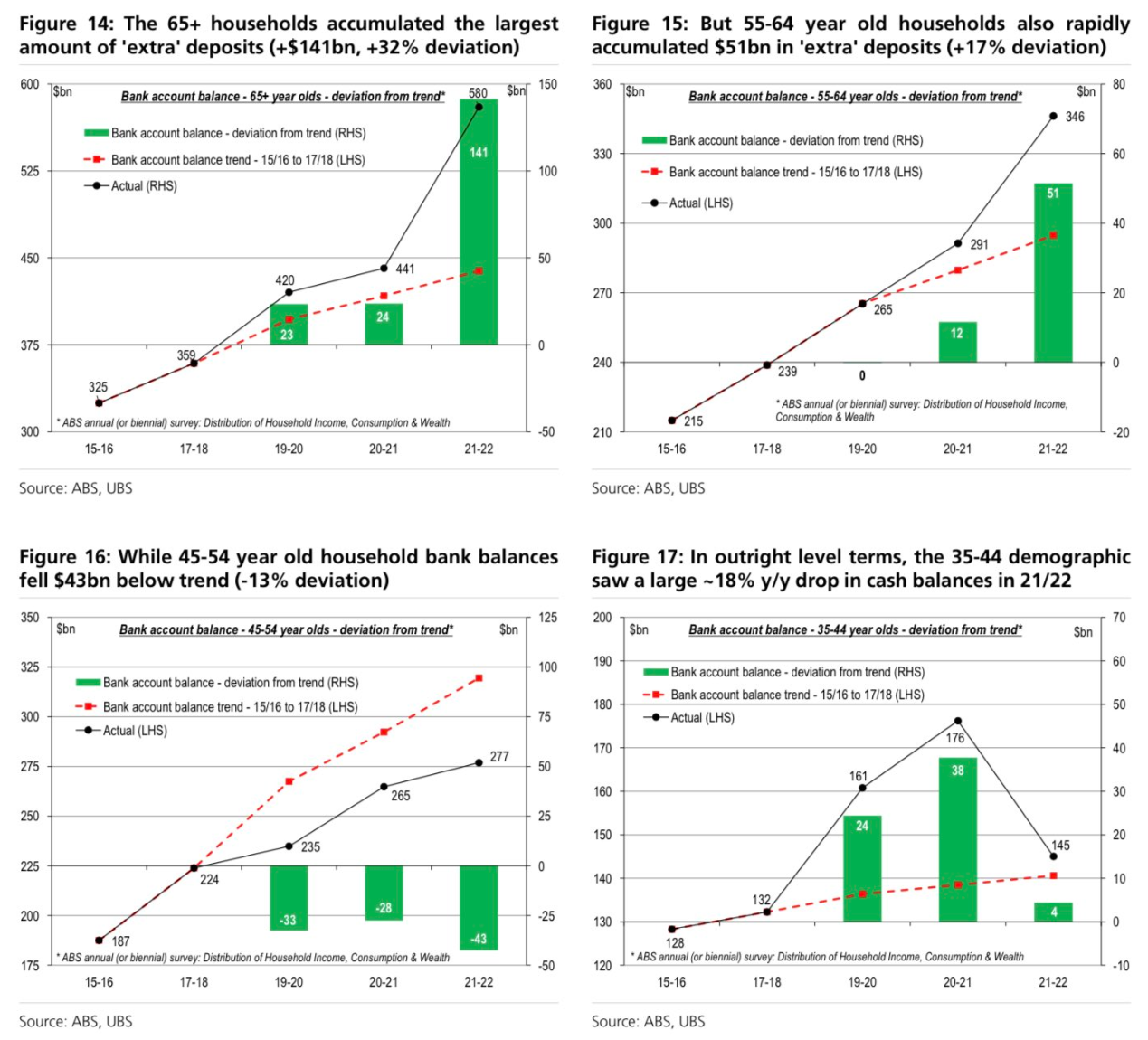

Finally, let’s not forget that baby boomers are by far Australia’s wealthiest generation and have made out like bandits over the pandemic.

As shown in the below charts from UBS, Australian households aged over 65 accumulated the overwhelming majority of the nation’s savings over the pandemic, followed by 55-64 aged households:

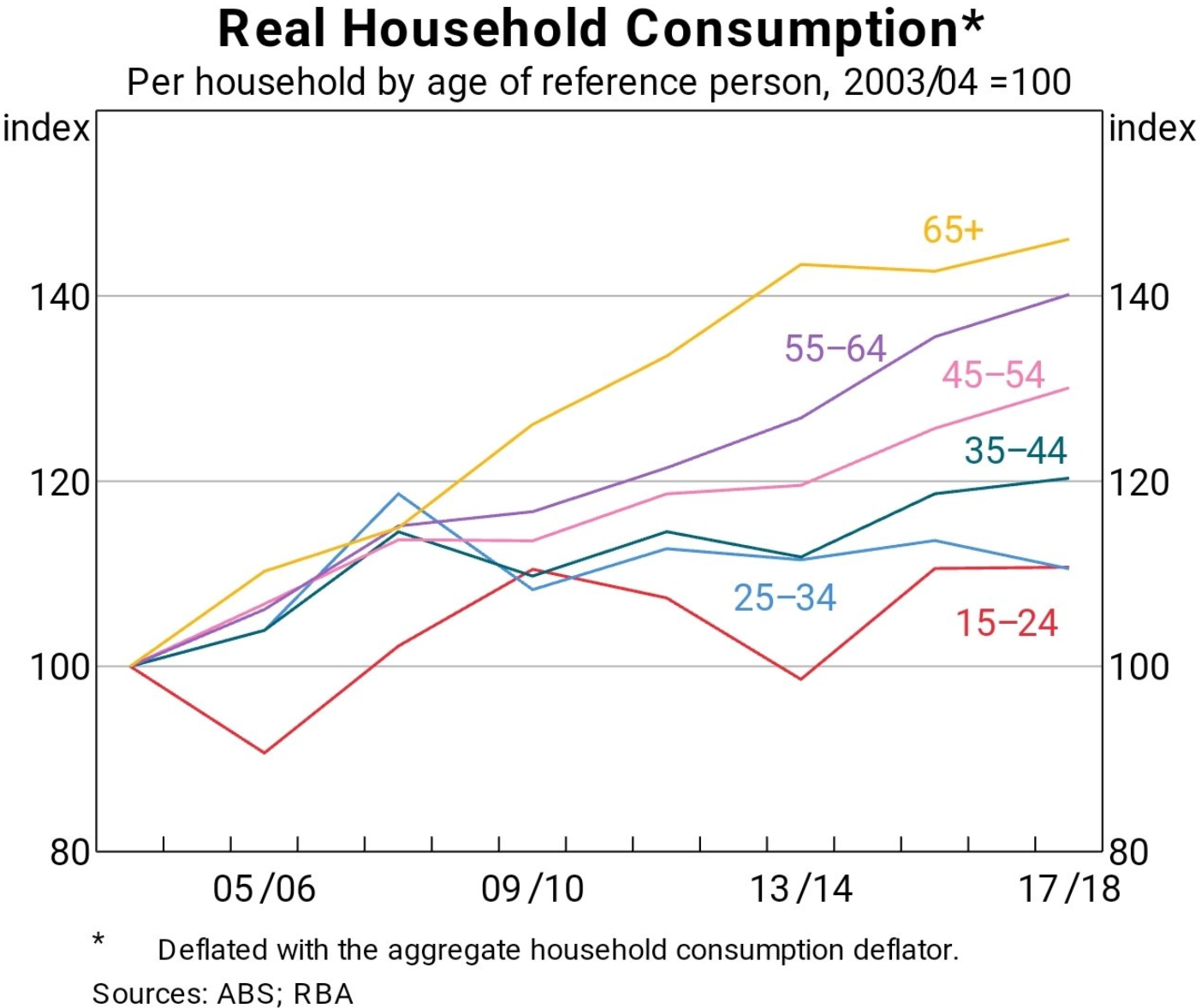

They have also enjoyed the strongest consumption growth over recent decades:

The baby boomer generation is also least impacted by soaring interest rates and rents.

So, spare me your crocodile tears.

Labor’s modest $3 million superannuation cap is entirely justifiable on equity and budget sustainability grounds.