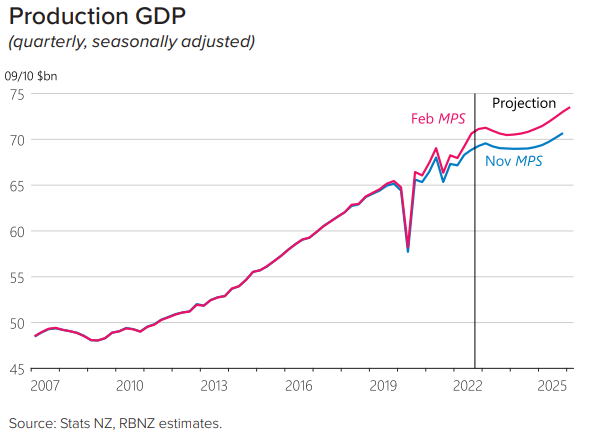

The Reserve Bank of New Zealand’s latest Monetary Policy Statement, released late last month, explicitly forecast that the economy would go into recession, registering a “peak-to-trough decline in the level of GDP over 2023… [of] about 1 percent”:

However, the Reserve Bank noted “there is considerable uncertainty about the timing”.

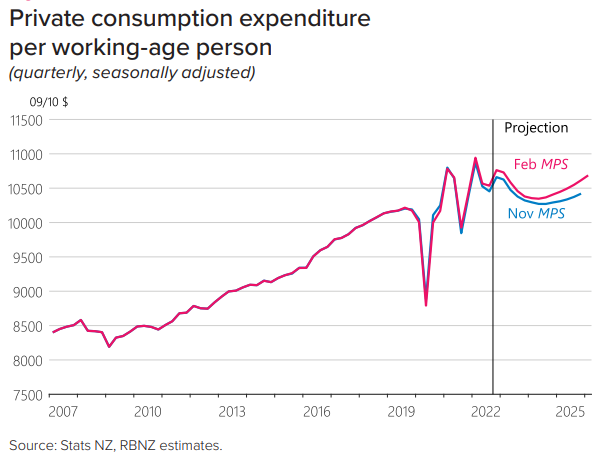

The Reserve Bank based its recession forecast on a contraction in household consumption via “higher interest rates, lower house prices and a weaker labour market”:

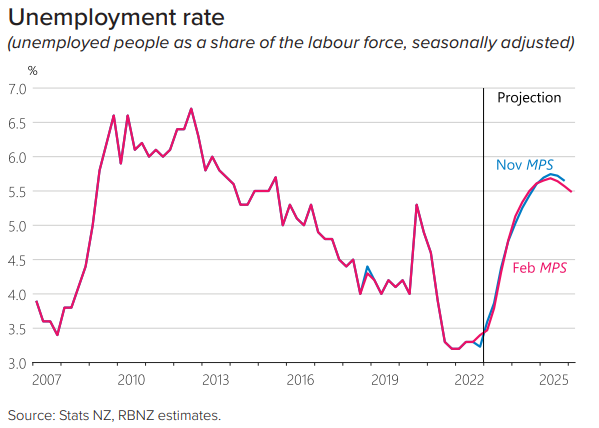

New Zealand’s unemployment rate was also projected by the Reserve Bank to soar by 2% over the forecast period:

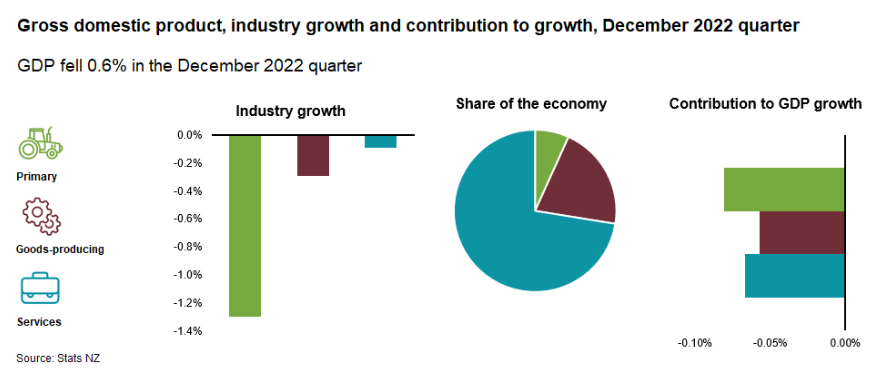

With this background in mind, the Reserve Bank is getting its wish with gross domestic product (GDP) falling 0.6% in the December quarter – a result that was worse than predicted by most bank economists and dramatically lower than the 0.7% increase in GDP forecast by the Reserve Bank.

GDP per capita fell 0.9% and real gross national disposable income, which measures the countries purchasing power, dropped 1.7%.

For New Zealand to be in technical recession, aggregate GDP growth needs to decline for two consecutive quarters.

Therefore, New Zealand is already halfway there, much sooner than the Reserve Bank anticipated.