The Reserve Bank of Australia’s (RBA) February Monetary Policy Statement showed that Aussie mortgage holders have been hit especially hard by the global rise in interest rates.

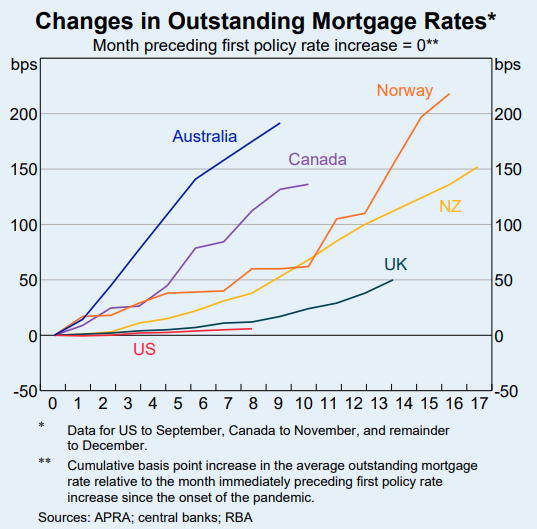

As illustrated in the next chart, Australian mortgage holders on average have experienced around a 200 basis point increase in mortgage repayments over this tightening cycle:

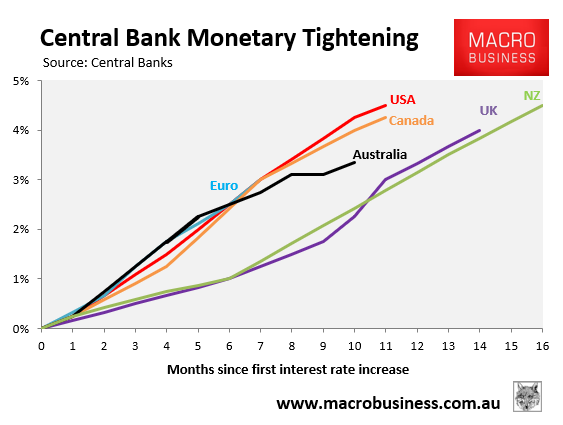

This far exceeds the experience of mortgage holders in other advanced English-Speaking nations, despite the RBA lifting official interest rates by less:

The primary reason why Australian mortgage holders have been hit harder is because a far higher proportion of borrowers here are on variable rate mortgages.

This means that increases in official interest rates are more quickly passed through to mortgage holders in Australia than elsewhere.

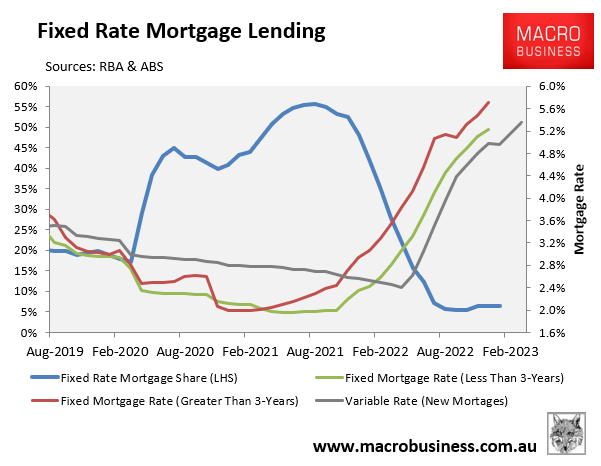

Even so, Australian households took out a record share of cheap fixed rate mortgages over the pandemic at interest rates of around 2%:

This has made monetary policy in Australia less responsive than it usually is, as noted in the RBA’s latest Bulletin. Accordingly, average outstanding mortgage rates are around 70 basis points lower than if all borrowers were paying variable rates:

In 2022, scheduled loan payments in aggregate increased a little slower than in the past because of the higher share of fixed-rate credit and because borrowers fixed their rates for longer than is typically the case…

If all fixed-rate loans instead paid the variable rate on new loans, the average outstanding mortgage rate would be 70 basis points (bps) higher than it was in December 2022.

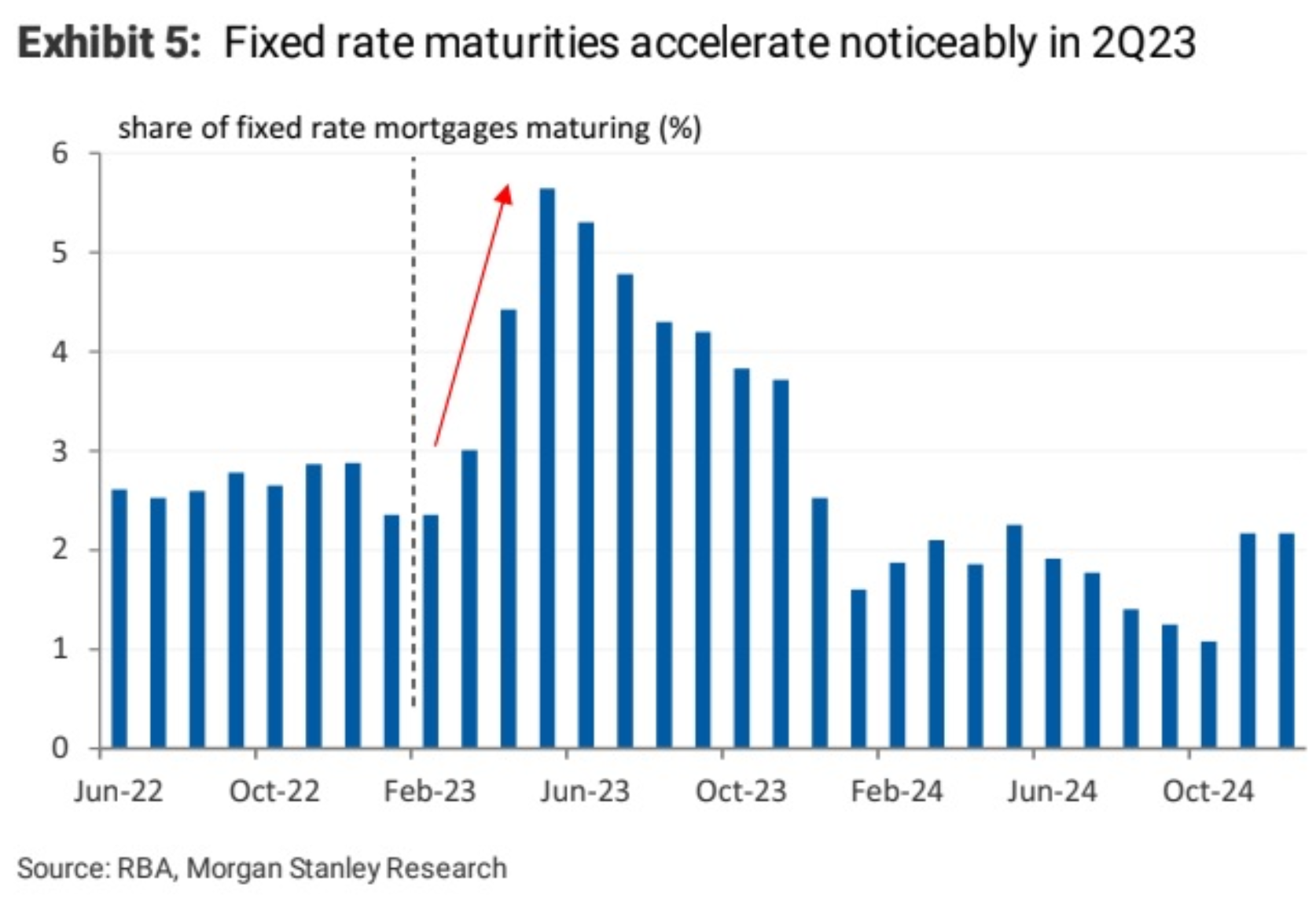

This situation will soon change with the RBA estimating that 880,000 fixed rate mortgages will expire in 2023, which means they “will face large, discrete increases in their loan payments when their fixed-rate terms expire”.

The next chart from Morgan Stanley summarises the situation with the volume of fixed rate mortgages expiring rising precipitously from April, peaking in May, and then remaining at high levels through the remainder of this year:

In his testimony to last month’s House Economics Committee, RBA governor Phil Lowe urged Australians struggling to meet their mortgage repayments to refinance.

“There are some good deals out there and people should hunt them down and take them”, Lowe said.

“There is competition for new borrowers and there is this discounting and again, people switching. I encourage people to do it”.

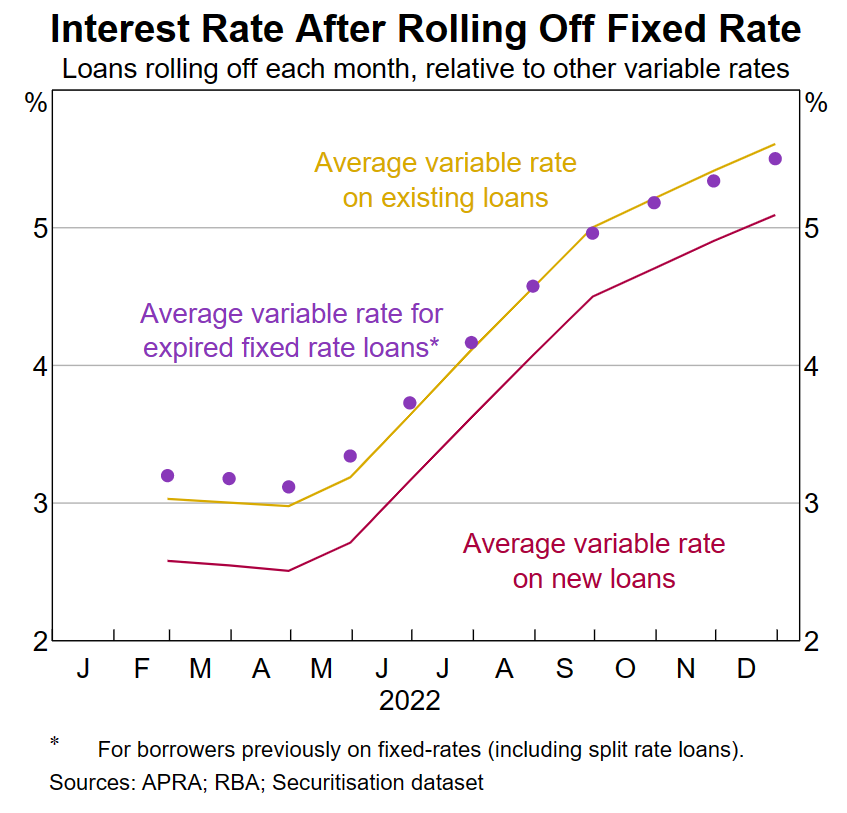

The next chart from the RBA Bulletin shows that the average variable interest rate on expiry of a fixed rate loan is around 50 basis points higher than the average variable rate on a new mortgage:

This suggests that borrowers could save significant sums on their mortgage repayments simply by refinancing.

This is where the MacroBusiness Compare n Save home loan comparison service can help.

With this service, borrowers can compare hundreds of loans to potentially save thousands of dollars in annual mortgage repayments.

Should you wish to proceed with an application, the team at Compare n Save will manage the entire process for you.

Try the Compare n Save comparison service for yourself. It is quick and easy.

Compare 100s of loans in seconds, hassle free…..

and when you’re ready to apply, we’ll manage the process for you.

I Want To Refinance

I Need A Loan

For example, if you are looking for a better deal on your existing loan, simply hit the “I Want To Refinance” button, enter the amount you wish to borrow and the interest rate you are currently paying.

The Compare n Save comparison tool will then show in simple terms how much you could save by refinancing, alongside loan options.

View the available loans on offer and if you wish to proceed with an application, simply hit the Enquire button, fill out your contact details and the team at Compare n Save will contact you to get the process moving.

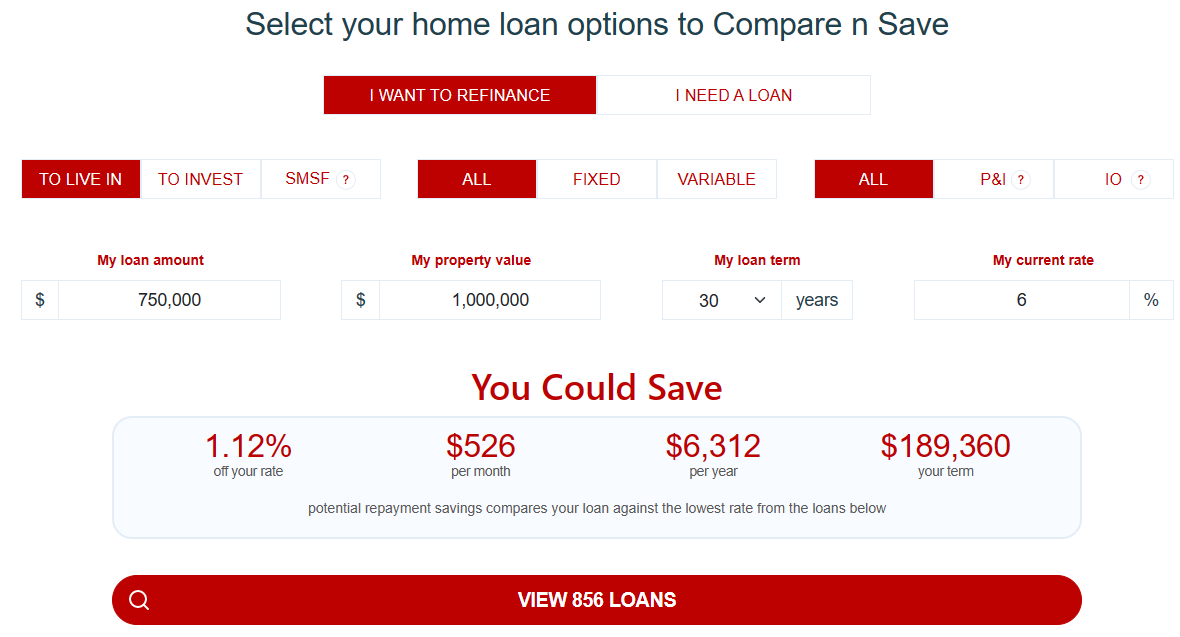

As an example, consider a household wishing to refinance a $750,000 mortgage on a home valued at $1,000,000 and currently paying a variable mortgage rate of 6%. They could save $526 per month ($6,312 a year) by refinancing to the lowest rate on offer:

The Compare n Save tool lists hundreds of loans to compare, from cheapest to more expensive.

If you proceed with a loan through Compare n Save, MacroBusiness receives a share of the commission, so you will help fund the site.

The record increase in interest rates is unfortunate. But at least you can lessen the pain by paying the lowest possible rate on your mortgage.