China: Industrial production rose 2.4% y/y ytd in February, up from 1.3% y/y in December. Consensus was 2.6%.

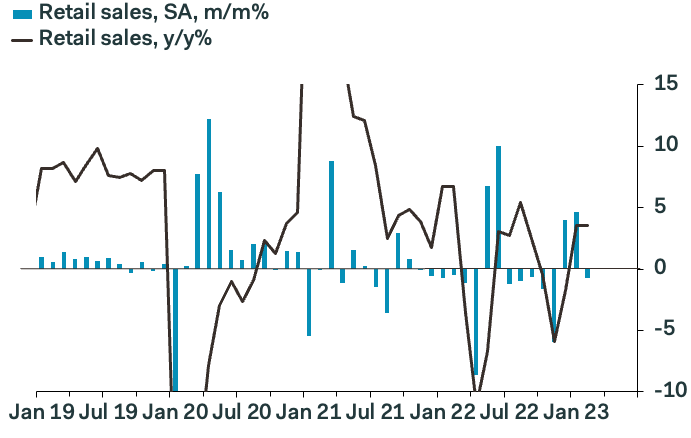

China: Retail sales climbed 3.5% y/y ytd in February, up from -1.8% y/y in December. Consensus was 3.5%.

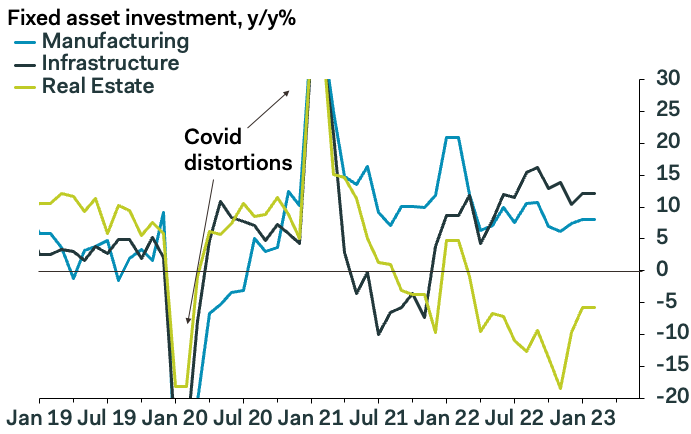

China: Fixed asset investment grew 5.5% y/y ytd in February, up from 3.2% y/y in December. Consensus was 4.5%.

China: 1 year MLF rate was unchanged at 2.75%. Consensus was 2.75%.

China enjoys a moderate rebound in the first two months, led by consumer services and infrastructure/manufacturing investment

China’s economy began to revive in the first two months of the year, after the removal of zero-Covid policy and the cresting of Covid exit waves in big cities in December. Consumer services led the reopening rebound, while

Consumer services staged a dramatic bounce-back, in line with the experience of other countries, after the withdrawal of Covid restrictions. Catering retail sales soared 9.2% y/y ytd in February, after plunging 14.1% y/y in December. The release of pent-up demand was particularly pronounced during the Lunar New Year holiday, when domestic tourism revenue surged 30% y/y.

Overall retail sales of goods showed a more measured come-back, rising 2.9% y/y ytd in February, after inching down 0.1% y/y in December, and falling 5.6% in November. Medicine sales were the fastest-growth category, owing to the Covid outbreaks. Sales of oil products, tobacco, beverages and furniture also performed well. By contrast, car sales fell 6.5% y/y ytd in February, after 9.7% growth in December. This is a result of the expiry of the preferential auto purchase tax policy at year-end as well as reduced subsidies for electric vehicle purchases. Some carmakers like Dongfeng Motors have slashed prices this month to shift high inventories, following poor sales this year.

The fixed asset investment data confirm earlier signs that local governments are front-loading policy support, after the December Central Economic Work Conference placed domestic demand expansion as the top policy priority for 2023. Infrastructure investment growth rose to 12.2% y/y ytd in February, from 10.4% in December, while manufacturing investment growth rose to 8.1%, from 7.4% in December. Local governments plan to issue over RMB2T in special bonds in the first quarter, out of the RMB3.8T annual quota. This investment project fund-raising activity showed up in strong government bond issuance and long-term corporate loan figures in the February credit data. We expect these policy-sensitive FAI sectors to remain strong in H1, then slow slightly in H2, providing the private sector recovery in consumption, business investment and property is sustained.

Real estate investment extended its decline, falling 5.7% y/y ytd in February, a tentative improvement from the 10% plunge for 2022 as a whole. The government has stepped up developer liquidity support for high-quality developers since November. The emphasis is on completing existing projects and delivering housing to buyers. Home sales are picking up in upper-tier cities since the Lunar New Year holiday. Our contact in Shanghai reported selling out batches of high-end housing in days. But many lower-tier cities are still under severe pressure, owing to high unsold housing inventories and much weaker underlying property demand. We expect a gradual recovery in the national property data over this year.

Industrial production grew 2.4% y/y ytd in February, up from 1.3% growth in December, as factory operations were less disrupted by worker sicknesses from the Covid exit waves. Manufacturing output is likely to gain momentum as domestic demand picks up, especially heavy industries, on the back of fixed asset investment-related demand. This will be partly offset by falling exports in sectors such as consumer electronics as global consumers curb purchases of work-at-home devices.

The Government Work Report set out a relatively conservative GDP growth target of “about 5%” for 2023. We think policymakers will be encouraged by the economic data showing a reopening rebound, but they are uncertain about the strength of the consumption revival. Households have accumulated excess savings at around RMB5T, but these are likely concentrated among relatively well-off households, who also have secure job prospects. We think that spending by these households is driving the initial consumption rebound, for example, in tourism spending. For the consumption rebound to have legs, the benefits of recovery must spread to lower-income households such as the 300M migrant workers. Many migrant workers are forced to take lower-paid service jobs, instead of working in factories making exports.

China has ample policy room to provide more fiscal, quasi fiscal or monetary stimulus later in the year, if the private sector recovery falters—and policymakers will be poised to act if necessary. For this reason, we see the growth target as attainable. It is just a question of the quality of growth, as a larger contribution from private consumption rather than debt-funded investment would be healthier.

The PBoC left the one-year MLF unchanged at 2.75%, in line with expectations, after the Bank said that current rates are relatively appropriate in a meeting before the just-concluded National People’s Congress. The Bank will be ready to add policy support if the domestic demand-led growth loses steam later in the year. For now, the PBoC is likely to focus on targeted credit support for weaker areas, like smaller firms and the private sector, by using structural tools like refinancing.

It is early days and the COVID stimulus via infrastructure is still running off while the private sector reopens. But I am having my doubts that Xi’s declared consumer-led recovery is underway or even possible.

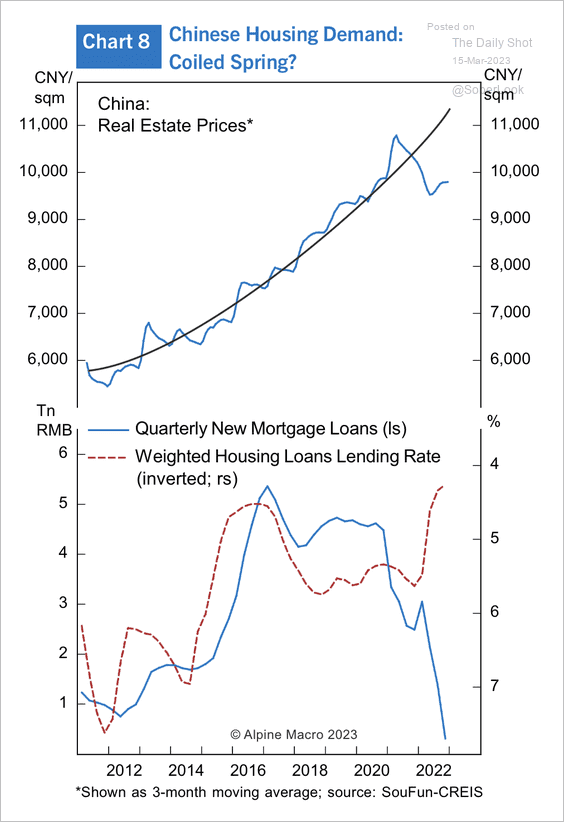

Chinese stimulus is nearly always directed at the supply side and the consumer hangs on real estate prices as well, which comes with overbuilding more supply-side.

Credit expansions also have a nasty habit of ending up in property:

Advertisement

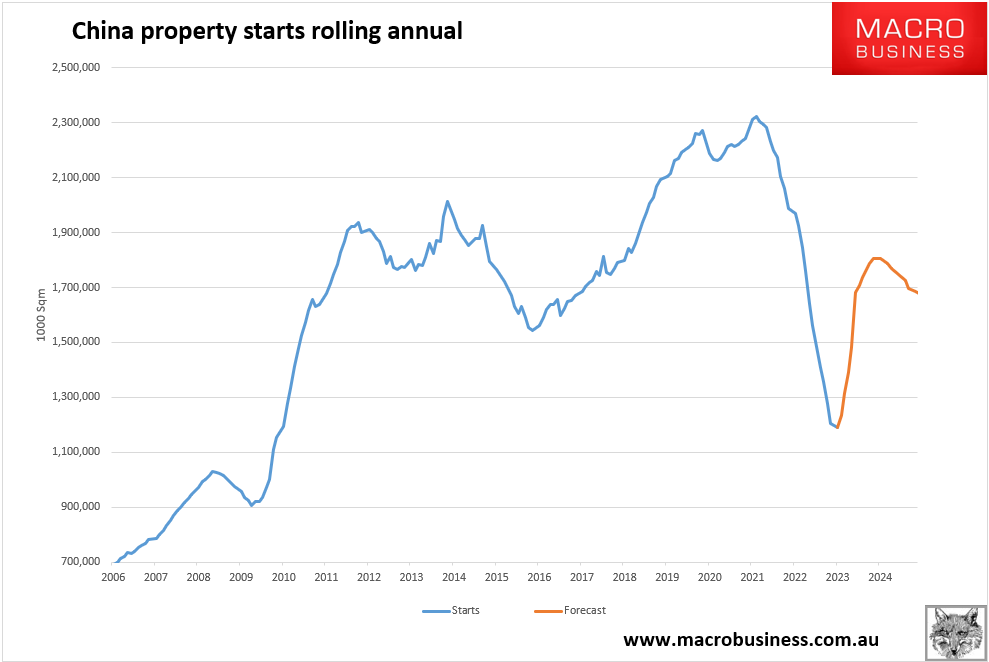

So far, this rebound looks exactly the same as previous iterations.

Property starts have begun to rebound in the second derivative and sales are forecasting a bounce of perhaps one-third from the bottom:

Advertisement

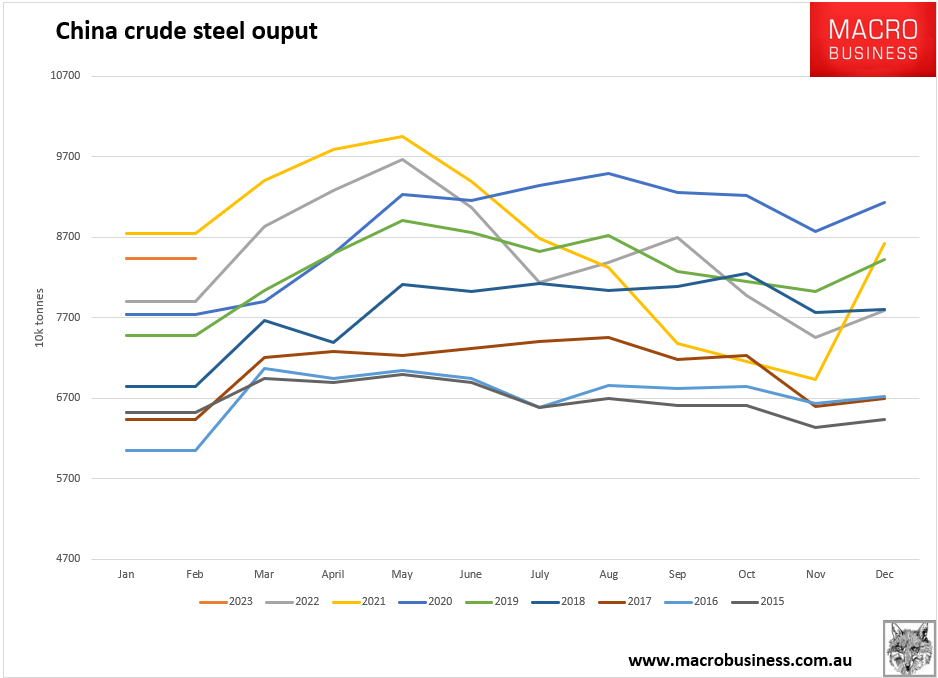

Steel output is strong on the infrastructure pump:

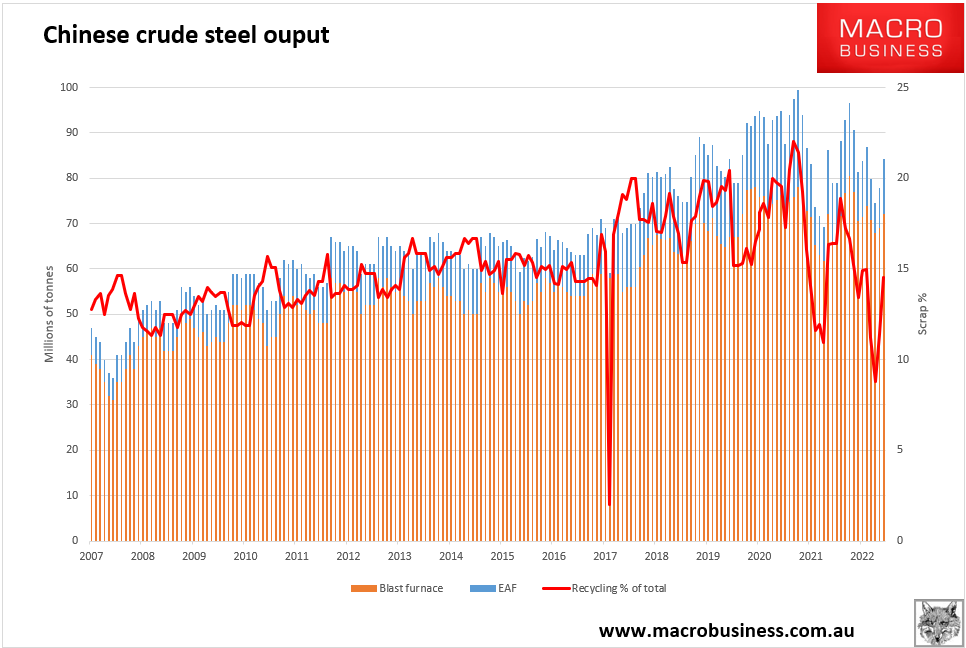

So much so that scrap output is climbing again:

Advertisement

Infrastructure is going to fade as property rises but the real question is can the Chinese consumer lift without a sustainable rise in property prices, and will that result in more overbuilding?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.