The AFR published an article this week explaining how 2370 people a day on average have refinanced their mortgage over the past six months.

70% of those refinancing have switched to another lender, while 30% have refinanced with their existing lender.

The intense competition has forced some banks to write mortgages at below their cost of capital, which has squeezed their net interest margins, according to article.

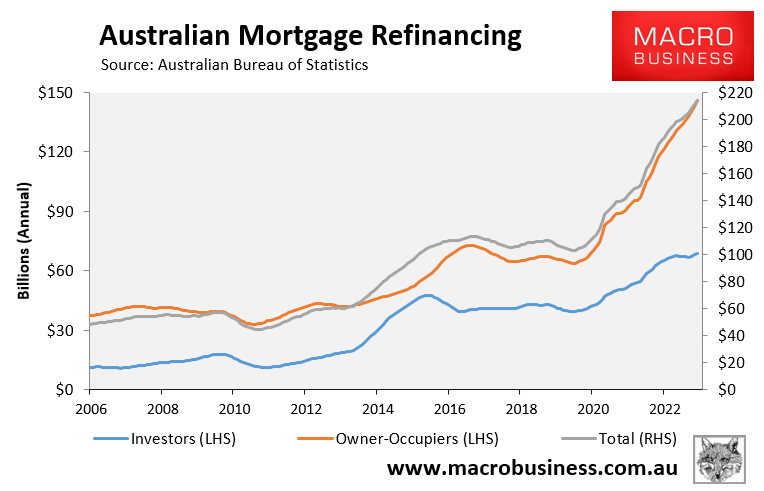

Mortgage refinancing is currently experiencing a record boom, with $214 billion dollars worth of loans written in the year to January – roughly double pre-pandemic levels:

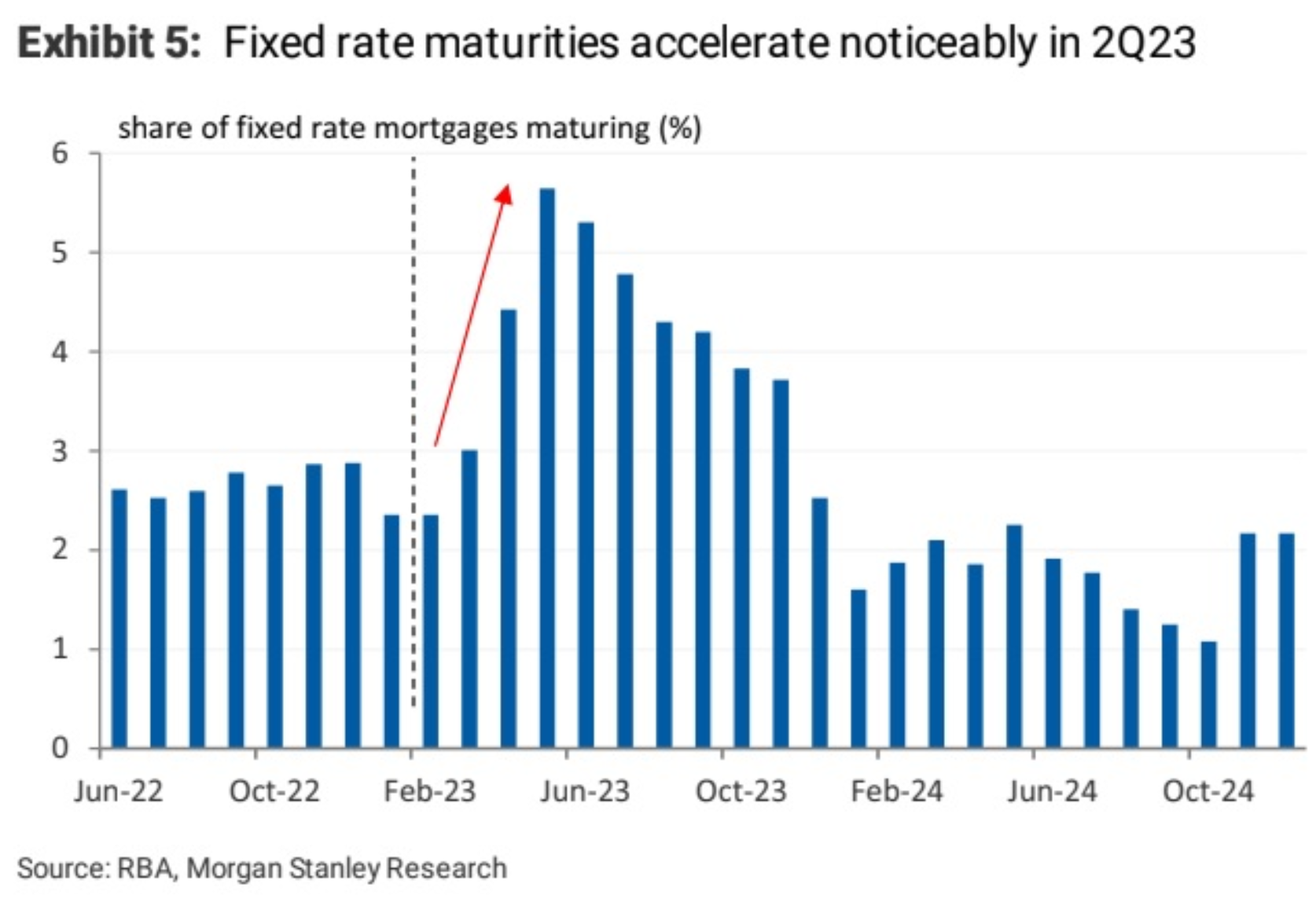

The rate of refinancing is certain to reach new heights in the months ahead, given a record number of fixed rate mortgages are scheduled to refinance over the next three months.

The next chart from Morgan Stanley illustrates the state of play, with the volume of fixed rate mortgages expiring jumping in April, peaking in May, and then remaining at high levels throughout the remainder of this year:

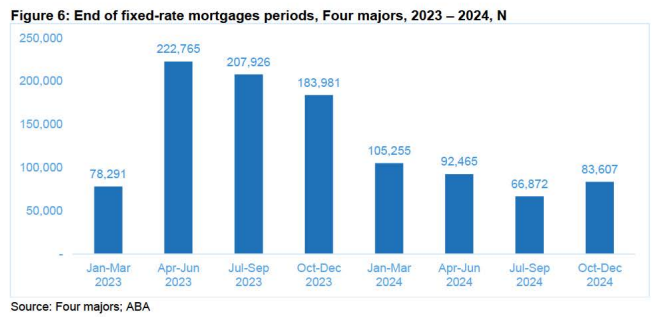

The next chart from the Australian Bankers Association, which illustrates quarterly fixed rate mortgage maturities across the Big Four banks, shows that around triple the number of mortgages will expire over the June quarter (222,800) than expired over the March quarter (78,300):

The September (208,000) and December (184,000) quarters will also see heavy volumes of fixed rate mortgage expiries.

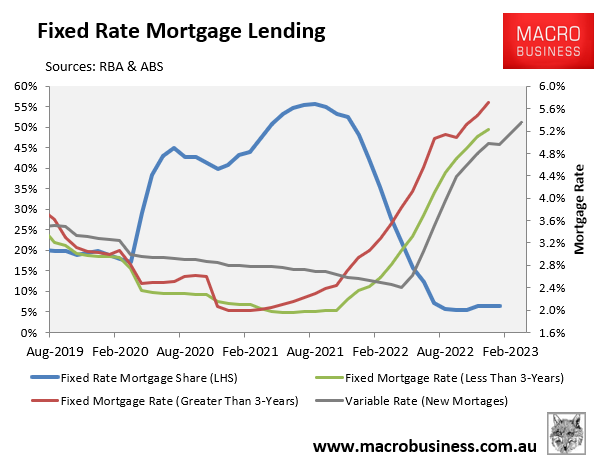

Many of these fixed rate mortgages were originated over the pandemic at rates of around 2%. This means that borrowers are facing a doubling or tripling of their mortgage rates when their loan terms expire and they switch to variable rates:

While the jump in mortgage rates is unavoidable, borrowers can at least lessen the pain by ensuring they pay the lowest possible mortgage rate on the market.

This is where the MacroBusiness Compare n Save home loan comparison service can help, which enables borrowers to compare hundreds of loans to potentially save thousands of dollars in annual repayments.

If you choose to proceed with an application, the team at Compare n Save will manage the entire process for you.

Try the Compare n Save comparison service for yourself. It is quick and easy to use.

Compare 100s of loans in seconds, hassle free…..

and when you’re ready to apply, we’ll manage the process for you.

I Want To Refinance

I Need A Loan

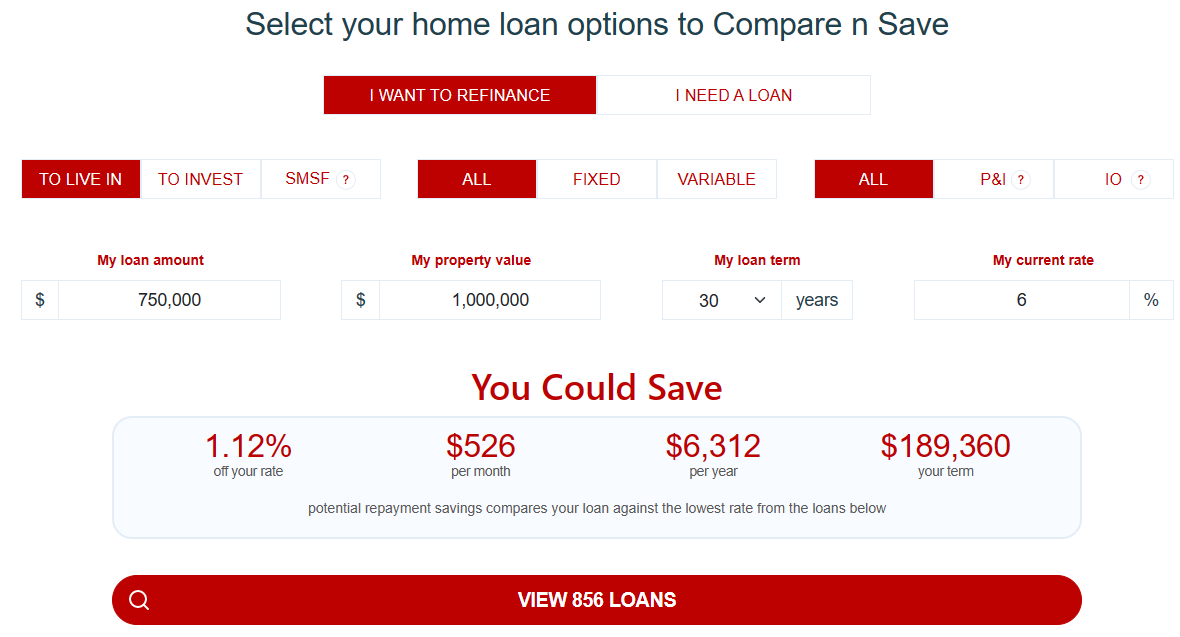

For example, if you are seeking a better rate on an existing mortgage, choose the “I Want To Refinance” option, enter the amount you wish to borrow and the interest rate you are currently paying.

Compare n Save will then show how much you could save by refinancing.

View the loans on offer and should you choose to proceed with an application, simply hit the Enquire button, fill out your contact details and the team at Compare n Save will contact you to get the process going.

As an example, consider someone seeking to refinance a $750,000 loan on a house valued at $1 million and paying a mortgage rate of 6%.

This borrower could save $526 per month ($6,312 a year) by refinancing to the lowest rate on offer:

The Compare n Save comparison tool lists hundreds of loans to compare, from cheapest to more expensive.

Should you obtain a loan via Compare n Save, MacroBusiness receives a share of the commission, which will help fund the site.

The next few months will be challenging for hundreds of thousands of borrowers coming off cheap fixed rate mortgages.

But at least you can lessen the impact by ensuring you pay the lowest possible rate.

Make the banks compete for your business.