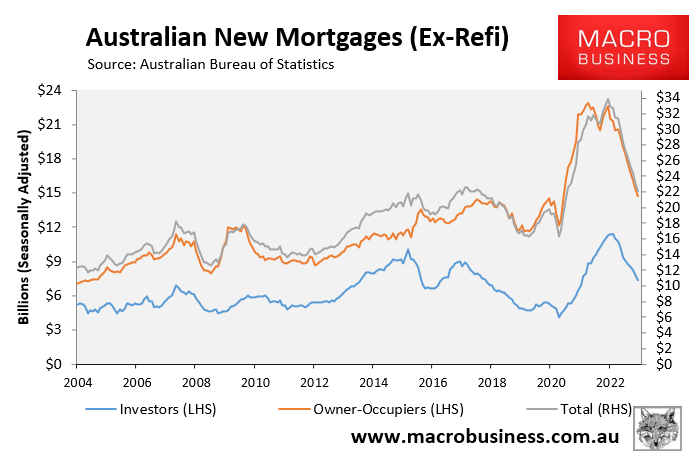

The Australian Bureau of Statistics (ABS) on Friday released mortgage commitments data for the month of January.

This showed that the value of mortgages originations fell to their lowest level since August 2020:

From its peak level a year earlier, annual mortgage originations were down a whopping 35%, with owner-occupiers and investors falling by equal amounts.

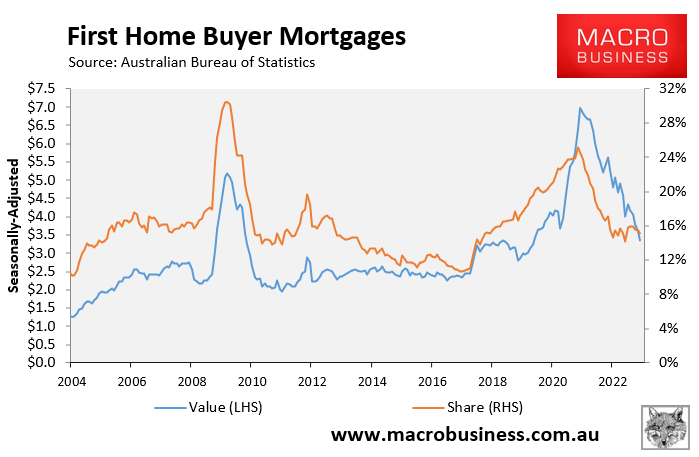

Australian first home buyers have well and truly fled the market, with mortgage commitments down 37% year-on-year to their lowest level since February 2017:

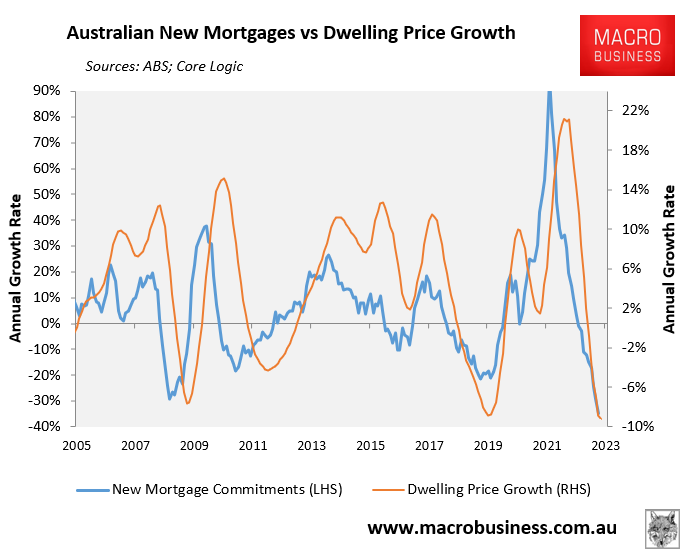

The collapse in mortgage originations augers badly for house prices, given mortgages typically lead prices by around a quarter, as illustrated clearly below:

Mortgage borrowing capacity has contracted by one-third in response to the Reserve Bank of Australia’s (RBA) 3.25% of interest rate hikes since April last year.

Given the RBA is expected to hike another 0.25% on Tuesday, with additional rate increases expected over following months, borrowing capacity will shrink further, which will pull both mortgage demand and house prices lower.

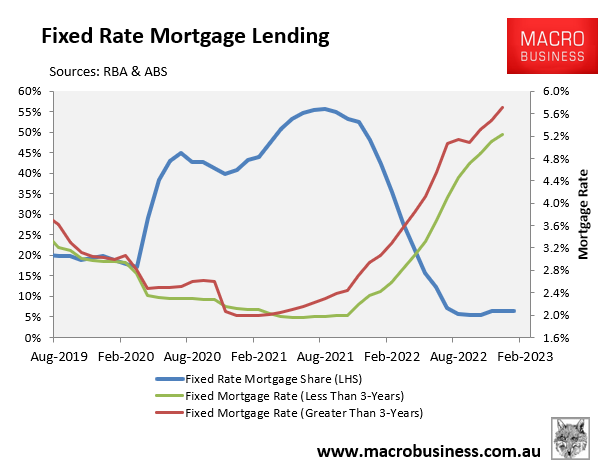

To add insult to injury, only a fraction of the RBA’s 3.25% of rate hikes have been felt by Australian mortgage borrowers.

The share of mortgage originations on fixed rates peaked at 56% in the second half of 2021, up from a historical average of only 20%:

This boom in faxed rate mortgage lending over the pandemic lifted the share of all home loan borrowers on fixed rates to one-third, according to the RBA, many of which were originated at rates of around 2%.

This year, nearly 900,000 borrowers, or nearly one quarter of Australia’s total mortgage book, will switch from cheap fixed rate mortgages taken out over the pandemic to variable mortgages with rates more than double those levels.

In turn, monetary conditions will continue to tighten in Australia even without further increases in the cash rate from the RBA.

Conditions are, therefore, primed for further house prices falls as mortgage demand continues to shrink alongside borrowing capacity.