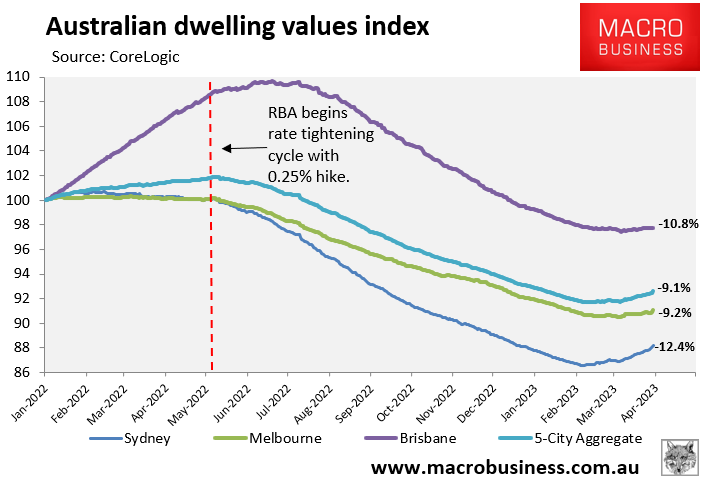

Dwelling values across Australia’s five major capital city markets have rebounded by 1.0% since 7 February, driven by a strong 1.9% rise across Sydney:

In an interview this week with Equity Mates Investing Podcast, Coolabah Capital’s Chris Joye explained why he believes the rebound is a seasonal bounce that will reverse when one in four Australian home loans convert from their current 2% fixed rates to 6% variable rates over 2023.

Joye argues this could deliver the “mother of all shocks” for household balance sheets and is sticking to his call that Australian home values will fall 15% to 25% peak-to-trough.

Below are key extracts of Joye’s interview.

“All our modelling implies house prices should fall 15% to 25%”.

“There has been a curious and somewhat surprising mini-bounce since February”.

“There is a lot of seasonality in housing. What that means is that prices statistically tend to rise over February, March, April, May. That’s because there is a strong seasonal rise in demand”.

“The little bounce hasn’t been at all sharp. It looks like a ‘dead cat bounce’. So we are sticking to our 15% to 25% expected drawdown”.

“We’re kind of 10 percentage points there”.

“We have seen the hottest migration in 20 years. And unambiguously that’s fuelling a bit of a bid in housing”.

“Anecdotally, we’re hearing lots of reports in Sydney and Melbourne of the return of the Chinese bid”.

“How that plays out in terms of the price discovery process is an open question”.

“But the flipside of the coin is that we know that the RBA has no interest in cutting rates”.

“The RBA has one or two hikes left in the system… But even if they don’t materialise, we do know that one in four Aussie home loans in 2023 switch from their 2% fixed rates to 6% variable rates”.

“This is going to be the mother of all shocks for household balance sheets according to the RBA’s own analysis”.

“What they found was that at a 3.6% cash rate, 15% of all Aussie borrowers had negative cash flow”.

“I think that’s pretty sobering that we are seeing 15% of borrowers at risk of default”.

“How that plays out in terms of the price discovery process with housing is interesting”.

“My own view is that prices will really struggle to appreciate in the next year or two”.

“If the RBA maintains its current path, we will experience peak-to-trough drawdowns of 15% to 25%”.

Whether the house price correction is genuinely over remains to be seen.

Regardless, my own view is that 2024 is shaping up to be a boom for house prices, given:

- The RBA is likely to cut rates, which would lift borrowing capacity.

- The Australian Prudential Regulatory Authority is likely to follow suit by reducing the 3% mortgage buffer, which would further boost borrowing capacity.

- Australia will continue to experience rapid immigration.

- The rental market will tighten further.

- Housing construction will be depressed, given high construction costs and widespread builder insolvencies.

There is genuine demand in the market. The only thing holding prices back is high mortgage rates and their impact on borrowing capacity.

Once that constraint is loosened, you have the ingredients for the next price boom.